PDF 原檔:260608_citi_GCE_original.pdf

原始內容

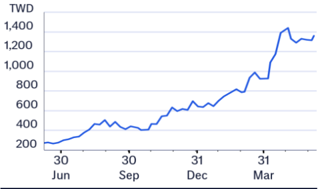

(RIC: 2300.1W, BB: 2560 11)

TWD

1,400

1,200

1,000

800

600

400

200

08 Jun 2026 14:04:50 ET │ 14 pages

Jun

Sep

Dec

Mar

Gold Circuit Electronics (2368.TW)

Record monthly sales backed by robust demand; Buy

CITI'S TAKE

Gold Circuit saw strong April-May sales driven by a better product mix (i.e., networking), higher ASP, and likely some new capacity ramp, in our view. We expect stronger sales momentum in the coming months given the start of production ramp for its existing ASIC customer. Given its market share gain in 2026, we expect GCE's plants to be fully utilized in the coming quarters. Further, the company sees a high likelihood of supplying a new ASIC customer, which we view as an important growth driver for 2027. We believe GCE's aggressive capacity expansion will help it capture more AI demand. Reiterate Buy with higher TP of NT$1,740 (26x 2027E EPS).

Strong sales uptick -GCE reported NT$8.8bn sales in May (+88% YoY, +20% MoM), driven in our view by ASP hike, enhanced product mix, and some sales delayed from April. Combined April and May sales account for c.70% of our 2Q26 Citi/consensus forecasts. Going forward, we believe the company could fully reflect the CCL price hike on end-customers given its leading PCB player position and tight capacity.

ASIC demand ramping up; potential new customer from 4Q26 -We expect existing ASIC demand to start ramping up in late 2Q26, with more meaningful contribution from 3Q26. GCE will likely leverage its Thailand plant to support the ASIC demand. We expect the company to gain market share at its existing ASIC customer. Management also sees a high likelihood of securing a new AI ASIC customer starting 4Q26. The company could supply its AI ASIC mainboard with >30L layer count design.

Continued capacity ramp to catch up with demand -This year, GCE is taking measures to debottleneck and ramp up additional capacity in Taiwan and Thailand. We also see it aiming to ramp up with one greenfield plant each year in 2027/28/29E across Thailand, China, and Taiwan. Despite the three plants currently planned, management thinks overall capacity is still not able to fulfill customer demand.

Earnings/TP upward revisions; higher TP NT$1,740 -We raise our 2026/27/28E earnings by 4%/4%/6% to reflect strong sales and enhanced product mix. We raise our TP to NT$1,740 (26x 2027E EPS) from NT$1,650 (26x 2027E EPS). We believe the high PE multiple of 26x is justified by GCE's market share gain with its existing ASIC customer and potential to secure a new ASIC customer. Reiterate Buy.

Earnings Summary

| Year to 31Dec | Net Profit (NT$M) | DilutedEPS (NT$) | EPSgrowth (%) | P/E (x) | P/B (x) | ROE (%) | Yield (%) |

|---|---|---|---|---|---|---|---|

| 2024A | 5,616 | 11.11 | 53.6 | 122.4 | 32.2 | 29.4 | 0.3 |

| 2025A | 9,607 | 18.98 | 70.9 | 71.6 | 20.6 | 35.1 | 0.4 |

| 2026E | 19,840 | 39.21 | 106.6 | 34.7 | 12.9 | 45.7 | 0.7 |

| 2027E | 33,399 | 66 | 68.3 | 20.6 | 7.9 | 47.7 | 1.4 |

| 2028E | 45,623 | 90.16 | 36.6 | 15.1 | 5.2 | 41.7 | 2.4 |

Source: Powered by dataCentral

See Appendix A-1 for Analyst Certification, Important Disclosures and Research Analyst Affiliations.

n Buy

Price (08 Jun 26 13:30)

NT$1,360.00

Target price

NT$1,740.00↑

from NT$1,650.00

Expected share price return

27.9%

Expected dividend yield

0.7%

Expected total return

28.7%

Market Cap

NT$703,184M US$22,349M

Price Performance (RIC: 2368.TW, BB: 2368 TT)

Jack Chen AC

+886-2-8726-9091 jack1.chen@citi.com

Laura (Chia Yi) Chen +886-2-8726-9090 laura.cy.chen@citi.com

Nicholas Lai +886-2-8726-9093 nicholas.lai@citi.com

| 2368.TW: Fiscalyearend31-Dec | 2368.TW: Fiscalyearend31-Dec | 2368.TW: Fiscalyearend31-Dec | 2368.TW: Fiscalyearend31-Dec | 2368.TW: Fiscalyearend31-Dec | 2368.TW: Fiscalyearend31-Dec | Price: NT$1,360.00; TP: NT$1,740.00; Market Cap:NT$703,184m; Recomm:Buy | Price: NT$1,360.00; TP: NT$1,740.00; Market Cap:NT$703,184m; Recomm:Buy | Price: NT$1,360.00; TP: NT$1,740.00; Market Cap:NT$703,184m; Recomm:Buy | Price: NT$1,360.00; TP: NT$1,740.00; Market Cap:NT$703,184m; Recomm:Buy | Price: NT$1,360.00; TP: NT$1,740.00; Market Cap:NT$703,184m; Recomm:Buy | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Profit&Loss(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E | Valuation ratios | 2024 | 2025 | 2026E | 2027E | 2028E |

| Sales revenue | 38,952 | 60,004 | 99,046 | 146,911 | 192,448 | PE(x) | na | 71.6 | 34.7 | 20.6 | 15.1 |

| Cost of sales | -27,556 | -40,321 | -62,234 | -87,491 | -112,470 | PB(x) | 32.2 | 20.6 | 12.9 | 7.9 | 5.2 |

| Gross profit | 11,396 | 19,683 | 36,812 | 59,420 | 79,978 | EV/EBITDA(x) | 76.9 | 45.8 | 22.2 | 12.9 | 9.1 |

| Gross Margin (%) | 29.3 | 32.8 | 37.2 | 40.4 | 41.6 | FCFyield (%) | 0.1 | -0.6 | -0.7 | 2.9 | 4.7 |

| EBITDA(Adj) | 9,118 | 15,327 | 31,792 | 53,816 | 72,977 | Dividend yield (%) | 0.3 | 0.4 | 0.7 | 1.4 | 2.4 |

| EBITDAMargin(Adj) (%) | 23.4 | 25.5 | 32.1 | 36.6 | 37.9 | Payout ratio (%) | 31 | 30 | 26 | 29 | 36 |

| Depreciation | -1,051 | -1,284 | -2,932 | -5,492 | -6,825 | ROE(%) | 29.4 | 35.1 | 45.7 | 47.7 | 41.7 |

| Amortisation | 0 | 0 | 0 | 0 | 0 | Cashflow(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E |

| EBIT (Adj) | 8,067 | 14,043 | 28,860 | 48,324 | 66,152 | EBITDA | 9,118 | 15,327 | 31,792 | 53,816 | 72,977 |

| EBIT Margin (Adj) (%) | 20.7 | 23.4 | 29.1 | 32.9 | 34.4 | Working capital | -1,129 | -8,564 | -10,184 | -6,770 | -8,358 |

| Net interest | 78 | 55 | 122 | 272 | 272 | Other | -2,451 | -4,437 | -9,020 | -14,925 | -20,529 |

| Associates | -340 | -79 | 0 | 0 | 0 | Operating cashflow | 5,538 | 2,327 | 12,588 | 32,121 | 44,091 |

| Non-Op/Except/Other Adj | 685 | 154 | -88 | 50 | 50 | Capex | -5,131 | -6,733 | -17,500 | -12,000 | -12,000 |

| Pre-tax profit | 8,490 | 14,173 | 28,894 | 48,646 | 66,474 | Net acq/disposals | -263 | -66 | 1,281 | 0 | 0 |

| Tax | -2,875 | -4,567 | -9,054 | -15,247 | -20,851 | Other | 0 | 0 | 0 | 0 | 0 |

| Extraord./Min.Int./Pref.div. | 0 | 0 | 0 | 0 | 0 Investing cashflow | -5,394 | -6,799 | -16,219 | -12,000 | -12,000 | |

| Reported net profit | 5,616 | 9,607 | 19,840 | 33,399 | 45,623 | Dividends paid | -1,703 | -2,920 | -5,105 | -9,920 | -16,700 |

| Net Margin (%) | 14.4 | 16.0 | 20.0 | 22.7 | 23.7 | Financing cashflow | 1,879 | 14,186 | 7,739 | 4,378 | 2,576 |

| CoreNPAT | 5,616 | 9,607 | 19,840 | 33,399 | 45,623 | Net change in cash | 2,023 | 9,714 | 4,107 | 24,499 | 34,667 |

| Per share data | 2024 | 2025 | 2026E | 2027E | 2028E | Free cashflow to s/holders | 407 | -4,407 | -4,912 | 20,121 | 32,091 |

| Reported EPS($) | 11.11 | 18.98 | 39.21 | 66.00 | 90.16 | ||||||

| Core EPS($) | 11.11 | 18.98 | 39.21 | 66.00 | 90.16 | ||||||

| DPS($) | 3.46 | 5.72 | 10.00 | 19.43 | 32.71 | ||||||

| CFPS($) | 10.96 | 4.60 | 24.88 | 63.48 | 87.13 | ||||||

| FCFPS($) | 0.81 | -8.71 | -9.71 | 39.76 | 63.42 | ||||||

| BVPS($) | 42.17 | 66.16 | 105.37 | 171.37 | 261.53 | ||||||

| Wtdavgordshares(m) | 487 | 491 | 493 | 493 | 493 | ||||||

| Wtdavgdiluted shares (m) | 505 | 506 | 506 | 506 | 506 | ||||||

| Growthrates | 2024 | 2025 | 2026E | 2027E | 2028E | ||||||

| Sales revenue (%) | 29.6 | 54.0 | 65.1 | 48.3 | 31.0 | ||||||

| EBIT (Adj) (%) | 57.1 | 74.1 | 105.5 | 67.4 | 36.9 | ||||||

| CoreNPAT(%) | 59.1 | 71.1 | 106.5 | 68.3 | 36.6 | ||||||

| CoreEPS(%) | 53.6 | 70.9 | 106.6 | 68.3 | 36.6 | ||||||

| BalanceSheet(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E | ||||||

| Cash&cashequiv. | 9,185 | 18,114 | 22,222 | 46,721 | 87,107 | ||||||

| Accounts receivables | 13,401 | 27,001 | 42,165 | 52,667 | 65,420 | ||||||

| Inventory | 7,900 | 9,747 | 14,365 | 17,787 | 21,835 | ||||||

| Net fixed &other tangibles | 12,779 | 19,121 | 32,408 | 38,917 | 38,372 | ||||||

| assets | |||||||||||

| Financial &other | 1,062 | 1,478 | 2,329 | 2,917 | 3,632 | ||||||

| Total assets | 44,584 8,268 | 75,746 | 113,774 | 159,294 | 216,651 | ||||||

| Accounts payable | 11,029 | 16,690 | 20,886 | 25,848 | |||||||

| Short-term debt | 2,722 | 5,937 11,875 | 5,937 | 5,937 | 5,937 | ||||||

| Long-term debt | 4,531 | 19,614 | 23,992 | 26,568 | |||||||

| Provisions &other liab | 7,751 | 13,425 | 18,212 | 21,759 | 25,955 | ||||||

| Total liabilities | 23,272 | 42,265 | 60,453 | 72,574 | 84,308 | ||||||

| Shareholders' equity Minority interests | 21,312 0 | 33,481 0 | 53,321 0 | 86,720 0 | 132,343 0 | ||||||

| Total equity | 21,312 | 33,481 | 53,321 | 86,720 | |||||||

| -303 | 3,329 | 132,343 | |||||||||

| Net debt (Adj) | -1,931 | -16,792 | -54,602 | ||||||||

| Net debt to equity (Adj) (%) | -9.1 | ||||||||||

| For definitions of the items in this table, | please click here. | -0.9 | 6.2 | -19.4 | -41.3 |

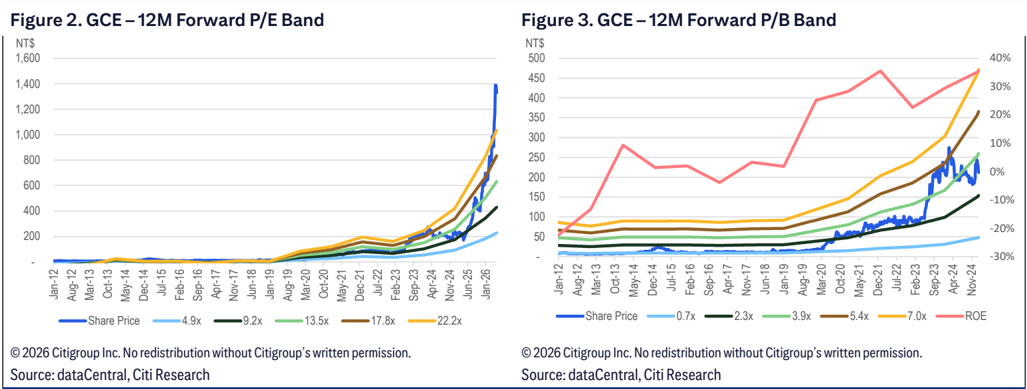

Figure 1. GCE - Earnings Revisions

| 2Q26E | 2Q26E | 2Q26E | 3Q26E | 3Q26E | 3Q26E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | New | Old | Chg. | New | Old | Chg. | New | Old | Chg. | New | Old | Chg. | New | Old | Chg. |

| Sales | 24,427 | 22,804 | 7% | 27,807 | 26,838 | 4% | 99,046 | 95,067 | 4% | 146,911 | 142,815 | 3% | 192,448 | 185,148 | 4% |

| Sequential growth (%) | 26% | 18% | 14% | 18% | 65% | 58% | 48% | 50% | 31% | 30% | |||||

| Gross profit | 8,943 | 8,320 | 7% | 10,592 | 10,205 | 4% | 36,812 | 35,247 | 4% | 59,420 | 57,335 | 4% | 79,978 | 75,817 | 5% |

| Opex | 1,946 | 1,814 | 7% | 2,220 | 2,141 | 4% | 7,953 | 7,628 | 4% | 11,096 | 10,783 | 3% | 13,826 | 13,298 | 4% |

| Operating profit | 6,997 | 6,505 | 8% | 8,373 | 8,063 | 4% | 28,860 | 27,619 | 4% | 48,324 | 46,552 | 4% | 66,152 | 62,519 | 6% |

| Pre-tax profit | 7,035 | 6,543 | 8% | 8,420 | 8,110 | 4% | 28,894 | 27,653 | 4% | 48,646 | 46,874 | 4% | 66,474 | 62,841 | 6% |

| Net income | 4,784 | 4,450 | 8% | 5,810 | 5,596 | 4% | 19,840 | 18,988 | 4% | 33,399 | 32,190 | 4% | 45,623 | 43,133 | 6% |

| EPS(NT$) | 9.45 | 8.79 | 8% | 11.48 | 11.06 | 4% | 39.21 | 37.52 | 4% | 66.00 | 63.61 | 4% | 90.16 | 85.24 | 6% |

| Gross margin (%) | 36.6% | 36.5% | +0.1 ppt | 38.1% | 38.0% | +0.1 ppt | 37.2% | 37.1% | +0.1 ppt | 40.4% | 40.1% | +0.3 ppt | 41.6% | 40.9% | +0.6 ppt |

| Opexratio (%) | 8.0% | 8.0% | +0.0ppt | 8.0% | 8.0% | +0.0ppt | 8.0% | 8.0% | +0.0ppt | 7.6% | 7.6% | +0.0ppt | 7.2% | 7.2% | +0.0ppt |

| Operating margin (%) | 28.6% | 28.5% | +0.1 ppt | 30.1% | 30.0% | +0.1 ppt | 29.1% | 29.1% | +0.1 ppt | 32.9% | 32.6% | +0.3 ppt | 34.4% | 33.8% | +0.6 ppt |

| Net margin (%) | 19.6% | 19.5% | +0.1 ppt | 20.9% | 20.9% | +0.0ppt | 20.0% | 20.0% | +0.1 ppt | 22.7% | 22.5% | +0.2 ppt | 23.7% | 23.3% | +0.4 ppt |

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

Source: Citi Research Estimates

Figure 4. GCE - Forecast Summary

| GCE (NT$inMn, year-end Dec) | 1Q | 2QE 3QE 2026 | 2QE 3QE 2026 | 4QE | 4QE | 1QE 2QE | 3QE 2027 | 4QE | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 19,313 | 24,427 | 27,807 | 27,499 | 32,684 | 36,210 | 39,108 | 38,909 | 19,166 | 20,596 | 18,991 | 23,398 | 26,607 | 32,785 | 30,044 | 38,952 | 60,004 | 99,046 | 146,911 | 192,448 |

| COGS | -12,590 | -15,484 | -17,215 | -16,944 | -19,579 | -21,663 | -23,195 | -23,054 | -17,283 | -17,596 | -16,500 | -18,108 | -20,236 | -24,057 | -22,320 | -27,556 | -40,321 | -62,234 | -87,491 | -112,470 |

| Depreciation costs | -469 | -599 | -752 | -906 | -1,080 | -1,230 | -1,341 | -1,453 | -942 | -887 | -754 | -615 | -653 | -743 | -821 | -960 | -1,195 | -2,725 | -5,104 | -6,343 |

| Gross Profit | 6,722 | 8,943 | 10,592 | 10,555 | 13,105 | 14,547 | 15,913 | 15,855 | 1,883 | 3,000 | 2,491 | 5,291 | 6,371 | 8,728 | 7,724 | 11,396 | 19,683 | 36,812 | 59,420 | 79,978 |

| OperatingExpense | -1,538 | -1,946 | -2,220 | -2,250 | -2,516 | -2,755 | -2,939 | -2,885 | -1,963 | -2,226 | -1,821 | -2,217 | -2,249 | -2,691 | -2,588 | -3,329 | -5,640 | -7,953 | -11,096 | -13,826 |

| SG&Aexpenses | -1,223 | -1,514 | -1,724 | -1,760 | -1,961 | -2,136 | -2,307 | -2,296 | -1,404 | -1,462 | -1,285 | -1,575 | -1,673 | -1,948 | -1,866 | -2,342 | -4,430 | -6,221 | -8,700 | -10,777 |

| R&Dexpenses | -348 | -464 | -528 | -522 | -588 | -652 | -665 | -623 | -420 | -474 | -471 | -533 | -623 | -718 | -803 | -974 | -1,256 | -1,863 | -2,527 | -3,180 |

| EBIT | 5,185 | 6,997 | 8,373 | 8,306 | 10,589 | 11,792 | 12,973 | 12,970 | -80 | 774 | 669 | 3,074 | 4,123 | 6,037 | 5,136 | 8,067 | 14,043 | 28,860 | 48,324 | 66,152 |

| NetInterestIncome | 28 | 26 | 34 | 34 | 58 | 66 | 74 | 74 | -219 | -258 | -213 | -147 | -51 | -27 | 78 | 78 | 55 | 122 | 272 | 272 |

| NetOther Income | -125 | 12 | 13 | 12 | 13 | 12 | 13 | 12 | 37 | -196 | -186 | -229 | -23 | 379 | 3 | 345 | 75 | -88 | 50 | 50 |

| Pre-Tax Profit | 5,088 | 7,035 | 8,420 | 8,352 | 10,660 | 11,870 | 13,060 | 13,056 | -263 | 320 | 270 | 2,698 | 4,049 | 6,388 | 5,218 | 8,490 | 14,173 | 28,894 | 48,646 | 66,474 |

| Tax | -1,604 | -2,251 | -2,610 | -2,589 | -3,614 | -3,798 | -3,918 | -3,917 | -6 | -92 | -140 | -631 | -1,122 | -1,820 | -1,689 | -2,875 | -4,567 | -9,054 | -15,247 | -20,851 |

| NetProfit | 3,484 | 4,784 | 5,810 | 5,763 | 7,046 | 8,072 | 9,142 | 9,139 | -269 | 229 | 130 | 2,067 | 2,927 | 4,568 | 3,529 | 5,616 | 9,607 | 19,840 | 33,399 | 45,623 |

| EPS(NT$) | 6.88 | 9.45 | 11.48 | 11.39 | 13.92 | 15.95 | 18.07 | 18.06 | -0.50 | 0.42 | 0.24 | 3.81 | 5.40 | 8.80 | 7.23 | 11.11 | 18.98 | 39.21 | 66.00 | 90.16 |

| Sequential Growth (%) | ||||||||||||||||||||

| Networking | 12% | -3% | 8% | -3% | 34% | -2% | 10% | 0% | -12% | 42% | -30% | 18% | 3% | 30% | -25% | 12% | 59% | 79% | 39% | 27% |

| Server | 21% | 34% | 15% | 0% | 19% | 13% | 8% | 0% | -7% | 5% | 8% | 28% | 11% | 48% | -3% | 40% | 67% | 70% | 54% | 34% |

| NB | -2% | 45% | 14% | -9% | -10% | 12% | 14% | -2% | 23% | -12% | -8% | 12% | 25% | -16% | -13% | -15% | 25% | 19% | 13% | 0% |

| Others | 18% | 10% | 1% | -12% | 1% | 12% | 1% | -12% | 14% | -6% | -8% | 41% | 28% | -32% | 3% | 83% | -29% | 11% | 0% | 0% |

| Margins (%) | ||||||||||||||||||||

| Gross Margin | 34.8% | 36.6% | 38.1% | 38.4% | 40.1% | 40.2% | 40.7% | 40.7% | 9.8% | 14.6% | 13.1% | 22.6% | 23.9% | 26.6% | 25.7% | 29.3% 32.8% | 37.2% | 40.4% | 41.6% | |

| OperatingMargin | 26.8% | 28.6% | 30.1% | 30.2% | 32.4% | 32.6% | 33.2% | 33.3% | -0.4% | 3.8% | 3.5% | 13.1% | 15.5% | 18.4% | 17.1% | 20.7% | 23.4% | 29.1% | 32.9% | 34.4% |

| NetMargin | 18.0% | 19.6% | 20.9% | 21.0% | 21.6% | 22.3% | 23.4% | 23.5% | -1.4% | 1.1% | 0.7% | 8.8% | 11.0% | 13.9% | 11.7% | 14.4% | 16.0% | 20.0% | 22.7% | 23.7% |

| Sequential Growth (%) | ||||||||||||||||||||

| Revenue | 18% | 26% | 14% | -1% | 19% | 11% | 8% | -1% | 0% | 7% | -8% | 23% | 14% | 23% | -8% | 30% | 54% | 65% | 48% | 31% |

| Gross Profit | 22% | 33% | 18% | 0% | 24% | 11% | 9% | 0% | -28% | 59% | -17% | 112% | 20% | 37% | -12% | 48% | 73% | 87% | 61% | 35% |

| EBIT | 30% | 35% | 20% | -1% | 27% | 11% | 10% | 0% | -111% | -1066% | -13% | 359% | 34% | 46% | -15% | 57% | 74% | 106% | 67% | 37% |

| NetProfit | 19% | 37% | 21% | -1% | 22% | 15% | 13% | 0% | -287% | -185% | -43% | 42% | 56% | -23% | 59% | 71% | 107% | 68% | 37% | |

| 19% | 21% | 22% | 0% | -289% | 1493% | -18% | 54% | |||||||||||||

| EPS | 37% | -1% | 15% | 13% | -185% | -43% | 1490% | 42% | 63% | 71% | 107% | 68% | 37% | 37% |

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

Source: Citi Research Estimates, Company Reports

NT$

1,800

1,500

1,200

900

600

300

Jun 25

4 32% Upside

NT$ 1,740.00

A 28% Upside

NT$ 1,100.00

• 19% Downside

Bull/Bear: Gold Circuit Electronics (2368.TW)

BASE Assumptions

• Revenue YoY growth of +65%/ + 48% in 2026/27E.

- GM at 37.2%/40.4% in 2026/27E.

BEAR Assumptions

• Share loss to its peers in switch board/UBB/OAM businesses of US CSPs.

- Poor efficiency of its Thailand plant.

Gold Circuit Electronics

Company description

Founded in 1981, Gold Circuit Electronics (GCE) is a Taiwanese company specializing in the production of printed circuit board (PCB) including doublesided PCB, multi-layer PCB, and HDI. GCE's products primarily focus on applications of servers, networking, laptops, base stations, mobile phones, and tablets. The company is known for its high-layer count design capabilities (maximum layer count: +50L) in the PCB industry, which help it to penetrate into more high-end applications such as AI servers and 400G networking. Currently, server/networking accounts for +70% of its total sales. The company has four plants, with one located in Taiwan and the other three in China, and plans to build one plant in Thailand.

Investment strategy

We rate GCE a Buy as we believe its high-tech capabilities in server/networking design will allow it to catch more AI opportunities from US CSPs or US IC designers in the AI boom cycle. We expect its rising sales exposure toward high-end applications with better margins and improving UTR to drive its margin going forward. In our view, geopolitical tensions should benefit non-China suppliers more, which would prevent GCE from fierce ASP competition from China PCB peers.

Valuation

Our TP of NT$1,740 for GCE is based on 26x our 2027E EPS estimate, which is higher than 22x or +2std level of its 1-year-forward PE over the past three years. We believe the 26x multiple is justified by GCE's high AI server/networking sales exposure, market share gain in existing ASIC customer and new AI ASIC customer wins from 4Q26, which drives its AI ASIC sales growth and margin profile. Recall that TSMC expects close to a 50%+ CAGR in the next five years for its AI-related demand, which is stronger than any other applications. Thus, we believe investors would be willing to pay for high-growth AI names (especially ASIC) with high PE multiples. Our target price is equivalent to 44x/26x our 2026/27E EPS estimates and 16.7x/10.2x our 2026/27E BVPS.

Risks

Key downside risks that could prevent the shares from reaching our target price include: 1) weaker-than-expected server recovery; 2) slower ramp-up pace of new server platform; 3) less-than-expected AI demand; 4) more PCB peers added into AI supply chain; and 5) stricter practice of China+1 by customers due to geopolitical concerns.

Analyst: Jack Chen

TWD

1,000

500

If you are visually impaired and would like to speak to a Citi representative regarding the details of the graphics in this document, please call USA 1-888-500-5008 (TTY: 711), from outside the US +1-210-677-3788 JASONDIFM AMIJASON DJ F M A M J

Date

Appendix A-1

E. 12-Mar-24 09:50:59

*280.00

242.50

@ 18-Feb-25 12:07:53

*270.00

198.50

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260608_citi_GCE_002.png |

140KB | 真資料圖 | 雙圖並列:Figure 2「GCE – 12M Forward P/E Band」與 Figure 3「GCE – 12M Forward P/B Band」,皆含 Share Price 折線與多條倍數估值線(P/E:4.9x/9.2x/13.5x/17.8x/22.2x;P/B:0.7x/2.3x/3.9x/5.4x/7.0x,另疊加 ROE 折線),X 軸 Jan-12 至 2026,含 © 2026 Citigroup Inc. 版權標示與 Source: dataCentral, Citi Research |