PDF 原檔:260606_2357_華碩_gs_asustek_original.pdf

原始內容

Asus (2357.TW): Enhanced AI-driven PC for LLM workloads and local AI tasks; TP raised to NT$1,082; Neutral

ASUS showcased the new ProArt P16/ P14 based on the NVIDIA RTX Spark Superchip (Link) during the Computex 2026, highlighting the faster AI model loading, ultra-responsive multitasking, and e ffi cient processing for creators, including the local AI tasks. Despite near-term pressures of memory cost weighing on the PC end demand, we see the company still bene fi ts from the rising AI PC adoption rate and speci fi cation upgrade for enhanced AI user experiences. Meanwhile, we expect to see company's AI server business ramp up across various platforms, supported by comprehensive o ff erings and client diversi fi cation. Maintain Neutral with TP raised to NT$1,082.

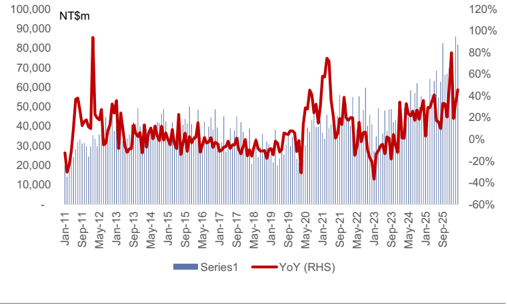

Monthly revenues preview: ASUS April revenues were +46% YoY/ -5% MoM to NT$82bn, or 36% higher than our estimates, and we attribute it to product mix upgrade with spec upgrade and customer pull-in. Looking ahead, despite memory cost pressures remaining, we expect the mix upgrade towards AI PC and rack-level AI server ramp up to support 2Q/ 3Q26E growth at 26%/ 12% YoY. We model May/ Jun revenues to grow 26%/ 9% YoY to NT$79bn/ NT$75bn, while MoM decline on the high base.

Exhibit 1: We expect ASUS May revenues growth at 26% YoY/ -3% MoM to NT$79bn ASUS monthly/ quarterly revenues

| Apr-26 | May-26E | Jun-26E | Jul-26E | Aug-26E | Sep-26E | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 81,915 | 79,458 | 74,725 | 68,747 | 74,246 | 93,105 | 236,098 | 223,645 |

| Rev YoY | 46% | 26% | 9% | 25% | 18% | 13% | 26% | 12% |

| RevMoM/QoQ | -5% | -3% | -6% | -8% | 8% | 25% | 22% | -5% |

| GS estimates (NT$m) | 60,259 | |||||||

| Act vs. GS | 36% |

Source: Company data, Goldman Sachs Global Investment Research

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng +852-2978-1681 | verena.jeng@gs.com

Goldman Sachs (Asia) L.L.C.

Ting Song +852-2978-6466 | ting.song@gs.com Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 2: ASUS monthly revenues

Source: Company data

Earnings revision: We revise up earnings by 4%/ 12%/ 14% in 2026-28E mainly on higher revenues. We revise up revenues on higher growth of (1) Notebook revenues driven by rising adoption of AI PC and speci fi cation upgrade to support on-device AI; (2) rack-level AI server ramp up with shipment growth and dollar content increase.

Exhibit 3: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NTm | Old | New | Chg | Old | New | Chg | Old | New | Chg |

| Revenue | 831,325 | 859,450 | 3% | 876,897 | 967,080 | 10% | 937,464 | 1,062,418 | 13% |

| GP | 120,935 | 125,096 | 3% | 136,440 | 149,602 | 10% | 147,031 | 165,687 | 13% |

| OP | 42,910 | 44,968 | 5% | 50,417 | 57,633 | 14% | 57,878 | 67,413 | 16% |

| Net income | 40,100 | 41,798 | 4% | 46,193 | 51,802 | 12% | 52,163 | 59,314 | 14% |

| Margins | |||||||||

| GM | 14.5% | 14.6% | 15.6% | 15.5% | 15.7% | 15.6% | |||

| OPM | 5.2% | 5.2% | 5.7% | 6.0% | 6.2% | 6.3% | |||

| NM | 4.8% | 4.9% | 5.3% | 5.4% | 5.6% | 5.6% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 4: ASUS revenues changes by segment

| Revenues (New) | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|

| Notebook | 353,080 | 333,226 | 339,767 | 344,796 |

| Desktop | 25,428 | 22,071 | 21,585 | 21,575 |

| Tablet | 1,655 | 1,663 | 1,561 | 1,483 |

| Workstation | 1,430 | 1,462 | 1,427 | 1,425 |

| Motherboard/Graphic Cards | 318,322 | 423,382 | 495,357 | 554,800 |

| General servers | 3,683 | 13,133 | 14,351 | 15,190 |

| AI servers | 16,968 | 46,389 | 70,391 | 94,862 |

| AIoT | 14,834 | 18,067 | 22,584 | 28,230 |

| Total | 738,905 | 859,450 | 967,080 | 1,062,418 |

| Revenues (Old) | 2025 | 2026E | 2027E | 2028E |

| Notebook | 356,894 | 333,926 | 305,797 | 303,812 |

| Desktop | 21,614 | 21,839 | 21,373 | 21,376 |

| Tablet | 1,655 | 1,663 | 1,561 | 1,483 |

| Workstation | 1,430 | 1,462 | 1,427 | 1,425 |

| Motherboard/Graphic Cards | 323,455 | 404,005 | 464,606 | 511,066 |

| General servers | 2,992 | 12,259 | 12,524 | 13,425 |

| AI servers | 12,525 | 38,631 | 48,572 | 59,644 |

| AIoT | 14,834 | 17,484 | 20,981 | 25,177 |

| Total | 738,905 | 831,325 | 876,897 | 937,464 |

| Revenues (Change) | 2025 | 2026E | 2027E | 2028E |

| Notebook | -1% | 0% | 11% | 13% |

| Desktop | 18% | 1% | 1% | 1% |

| Tablet | 0% | 0% | 0% | 0% |

| Workstation | 0% | 0% | 0% | 0% |

| Motherboard/Graphic Cards | -2% | 5% | 7% | 9% |

| General servers | 23% | 7% | 15% | 13% |

| AI servers | 35% | 20% | 45% | 59% |

| AIoT | 0% | 3% | 8% | 12% |

| Total | 0% | 3% | 10% | 13% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 5: ASUS GM changes by segment

| GM (New) | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|

| Notebook | 14.6% | 13.2% | 13.8% | 14.0% |

| Desktop | 14.0% | 12.5% | 13.0% | 13.2% |

| Tablet | 11.1% | 11.0% | 11.0% | 11.0% |

| Workstation | 15.8% | 16.0% | 16.0% | 16.0% |

| Motherboard/Graphic Cards | 16.2% | 16.4% | 17.8% | 18.0% |

| General servers | 11.0% | 11.0% | 11.0% | 11.0% |

| AI servers | 6.7% | 8.5% | 9.0% | 9.0% |

| AIoT | 15.4% | 15.3% | 14.6% | 14.6% |

| Total | 15.1% | 14.6% | 15.5% | 15.6% |

| GM (Old) | 2025 | 2026E | 2027E | 2028E |

| Notebook | 14.6% | 13.2% | 13.8% | 13.9% |

| Desktop | 13.8% | 12.5% | 13.0% | 13.2% |

| Tablet | 11.1% | 11.0% | 11.0% | 11.0% |

| Workstation | 16.1% | 16.0% | 16.0% | 16.0% |

| Motherboard/Graphic Cards | 16.2% | 16.4% | 17.7% | 17.8% |

| General servers | 11.0% | 11.0% | 11.0% | 11.0% |

| AI servers | 6.6% | 8.6% | 9.0% | 9.0% |

| AIoT | 14.8% | 14.6% | 14.6% | 14.6% |

| Others | 10.7% | 11.1% | 12.3% | 12.3% |

| Total | 15.1% | 14.5% | 15.6% | 15.7% |

| GM (Change) | 2025 | 2026E | 2027E | 2028E |

| Notebook | 0ppts | 0ppts | 0ppts | 0.1ppts |

| Desktop | 0ppts | 0ppts | 0ppts | 0ppts |

| Tablet | 0ppts | 0ppts | 0ppts | 0ppts |

| Workstation | 0ppts | 0ppts | 0ppts | 0ppts |

| Motherboard/Graphic Cards | 0ppts | 0ppts | 0.1ppts | 0.2ppts |

| General servers | 0ppts | 0ppts | 0ppts | 0ppts |

| AI servers | 0ppts | 0ppts | 0ppts | 0ppts |

| AIoT | 0ppts | 0.7ppts | 0ppts | 0ppts |

| Total | 0ppts | 0ppts | -0.1ppts | -0.1ppts |

Source: Company data, Goldman Sachs Global Investment Research

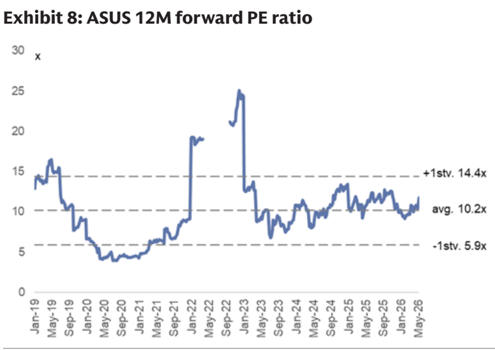

Valuation: We continue to use near term P/E to derive our 12M TP. Our target P/E is updated to 15.8x 2027E EPS, (vs. 11.3x previously), still derived from peers' avg. ratio of 2027E PE to 2028E NI YoY and OPM and supported by our higher 2028E NI growth at 15% (vs. 12% previously). With the updated earnings estimates and target P/E, our 12M TP is raised to NT$1,082.0 (vs. NT$690.1 previously). Maintain Neutral.

Exhibit 6: ASUS P&L Summary

| (NT$ m) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 147,693 | 188,006 | 200,281 | 202,924 | 194,051 | 236,098 | 223,645 | 205,656 | 537,192 | 482,314 | 587,087 | 738,905 | 859,450 | 967,080 | 1,062,418 |

| Gross profit | 24,600 | 25,963 | 28,706 | 32,346 | 26,709 | 33,886 | 33,646 | 30,855 | 74,145 | 72,405 | 103,474 | 111,614 | 125,096 | 149,602 | 165,687 |

| Operating income | 12,580 | 7,835 | 9,839 | 9,403 | 10,502 | 10,748 | 12,400 | 11,317 | 12,982 | 11,164 | 29,595 | 39,656 | 44,968 | 57,633 | 67,413 |

| Net income | 12,791 | 9,806 | 10,556 | 11,405 | 9,797 | 10,120 | 11,400 | 10,481 | 14,691 | 15,928 | 31,394 | 44,558 | 41,798 | 51,802 | 59,314 |

| EPS (NT$) | 17.22 | 13.20 | 14.21 | 15.36 | 13.19 | 13.62 | 15.35 | 14.11 | 19.78 | 21.44 | 42.27 | 59.99 | 56.27 | 69.74 | 79.13 |

| Margins / ratio | |||||||||||||||

| Gross margin | 16.7% | 13.8% | 14.3% | 15.9% | 13.8% | 14.4% | 15.0% | 15.0% | 13.8% | 15.0% | 17.6% | 15.1% | 14.6% | 15.5% | 15.6% |

| Operating margin | 8.5% | 4.2% | 4.9% | 4.6% | 5.4% | 4.6% | 5.5% | 5.5% | 2.4% | 2.3% | 5.0% | 5.4% | 5.2% | 6.0% | 6.3% |

| Net margin | 8.7% | 5.2% | 5.3% | 5.6% | 5.0% | 4.3% | 5.1% | 5.1% | 2.7% | 3.3% | 5.3% | 6.0% | 4.9% | 5.4% | 5.6% |

| QoQ | |||||||||||||||

| Revenue | -4% | 27% | 7% | 1% | -4% | 22% | -5% | -8% | |||||||

| Gross profit | -6% | 6% | 11% | 13% | -17% | 27% | -1% | -8% | |||||||

| Operating income | 699% | -38% | 26% | -4% | 12% | 2% | 15% | -9% | |||||||

| Net income | 681% | -23% | 8% | 8% | -14% | 3% | 13% | -8% | |||||||

| EPS | 681% | -23% | 8% | 8% | -14% | 3% | 13% | -8% | |||||||

| YoY | |||||||||||||||

| Revenue | 21% | 30% | 20% | 32% | 31% | 26% | 12% | 1% | 0% | -10% | 22% | 26% | 16% | 13% | 10% |

| Gross profit | 26% | -7% | -4% | 24% | 9% | 31% | 17% | -5% | -33% | -2% | 43% | 8% | 12% | 20% | 11% |

| Operating income | 160% | -32% | -16% | 497% | -17% | 37% | 26% | 20% | -74% | -14% | 165% | 34% | 13% | 28% | 17% |

| Net income | 135% | -17% | -16% | 596% | -23% | 3% | 8% | -8% | -67% | 8% | 97% | 42% | -6% | 24% | 15% |

| EPS | 135% | -17% | -16% | 596% | -23% | 3% | 8% | -8% | -67% | 8% | 97% | 42% | -6% | 24% | 13% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

30

25

20

15

10

x

70% 66%

60%

50%

Exhibit 7: Target P/E is derived from peers' avg. ratio of 2027E PE to 2028E NI YoY and OPM

42%

| Company Ticker Rating | ASUS 2357.TW Neutral | Lenovo 0992.HK Buy | Gigabyte 2376.TW Neutral | Dell DELL Buy | Quanta 2382.TW Neutral | HP HPQ Sell | Apple AAPL Buy |

|---|---|---|---|---|---|---|---|

| 2027E PE | 15.8 | 16.5 | 12.8 | 19.3 | 12.5 | 8.7 | 32.5 |

| 2028E NI YoY | 15% | 25% | 15% | 12% | 4% | 12% | 6% |

| 2028E OPM | 6.3% | 3.8% | 5.0% | 9.5% | 3.6% | 7.0% | 32.1% |

| Ratio | 0.8 | 0.6 | 0.6 | 0.9 | 1.7 | 0.5 | 0.8 |

| Avg. | 0.8 |

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 10: ASUS Balance sheet and Cash fl ow statement

| Balance Sheet (NT$m) | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|

| Cash and equivalents | 79,227 | 94,038 | 90,079 | 78,847 | 80,451 | 102,128 |

| Accounts receivable | 86,817 | 107,078 | 139,327 | 152,651 | 175,892 | 179,218 |

| Inventory | 122,790 | 152,620 | 197,642 | 265,101 | 294,815 | 294,816 |

| Other current assets | 18,342 | 25,507 | 26,786 | 26,786 | 26,786 | 26,786 |

| Current assets | 307,177 | 379,243 | 453,834 | 523,385 | 577,943 | 602,947 |

| Net PP&E/Fixed assets | 20,082 | 20,838 | 21,359 | 20,386 | 19,322 | 18,229 |

| Net intangibles | 2,687 | 2,891 | 13,283 | 9,881 | 6,873 | 4,711 |

| Other long-term assets | 150,136 | 153,552 | 143,181 | 143,181 | 143,181 | 143,181 |

| Non-current assets | 172,905 | 177,281 | 177,823 | 173,448 | 169,376 | 166,121 |

| Total assets | 480,082 | 556,524 | 631,657 | 696,833 | 747,319 | 769,068 |

| Accounts payable | 56,967 | 73,997 | 119,584 | 174,158 | 202,106 | 200,809 |

| Short-term debt | 16,273 | 25,296 | 29,755 | 29,755 | 29,755 | 29,755 |

| Other current liabilities | 124,312 | 132,574 | 158,009 | 156,076 | 163,081 | 168,340 |

| Current liabilities | 197,552 | 231,867 | 307,347 | 359,989 | 394,941 | 398,903 |

| Long-term debt | 162 | 366 | 293 | 293 | 293 | 293 |

| Other long-term liabilities | 23,386 | 27,093 | 26,453 | 26,453 | 26,453 | 26,453 |

| Non-current liabilities | 23,547 | 27,459 | 26,747 | 26,747 | 26,747 | 26,747 |

| Total liabilities | 221,100 | 259,326 | 334,094 | 386,735 | 421,687 | 425,650 |

| Common stock | 7,428 | 7,428 | 7,428 | 7,428 | 7,428 | 7,428 |

| Retained earnings | 163,411 | 182,629 | 202,004 | 214,538 | 230,072 | 247,859 |

| Other common equity | 68,977 | 79,483 | 58,865 | 58,865 | 58,865 | 58,865 |

| Total common equity | 239,816 | 269,540 | 268,297 | 280,831 | 296,365 | 314,152 |

| Minority interest | 19,166 | 27,658 | 29,266 | 29,266 | 29,266 | 29,266 |

| Total equity | 258,982 | 297,198 | 297,563 | 310,097 | 325,632 | 343,419 |

| BVPS | 321.62 | 360.10 | 354.99 | 371.27 | 391.81 | 415.32 |

| Cash conversion cycle | ||||||

| Account receivable days | 67 | 60 | 61 | 62 | 62 | 61 |

| Inventory days | 118 | 104 | 102 | 115 | 125 | 120 |

| Net payable days | 48 | 49 | 56 | 73 | 84 | 82 |

| Cash conversion cycle | 137 | 115 | 106 | 104 | 103 | 99 |

| Ratios | ||||||

| ROA | 3% | 6% | 8% | 6% | 7% | 8% |

| Net debt to total equity | -25% | -24% | -20% | -16% | -16% | -21% |

| Net cash per share (NTD) | 86.18 | 94.85 | 80.54 | 65.63 | 67.75 | 96.41 |

| Total liabilities to total assets | 46% | 47% | 53% | 55% | 56% | 55% |

| Dupont analysis | ||||||

| Asset turnover | 1.0 | 1.1 | 1.2 | 1.3 | 1.3 | 1.4 |

| Leverage (assets to equity) | 1.9 | 1.9 | 2.1 | 2.2 | 2.3 | 2.2 |

| Net margin | 3% | 5% | 6% | 5% | 5% | 6% |

| ROE (total equity) | 7% | 11% | 15% | 14% | 16% | 18% |

| CROCI (EDBITA/total equity) | 5% | 11% | 14% | 17% | 20% | 21% |

| Cash flow statement (NT$m) | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

| Net income | 15,928 | 31,394 | 44,558 | 41,798 | 51,802 | 59,314 |

| Minority interest add-back | (1,962) | (2,845) | (3,659) | - | - | - |

| Depreciation and amortization add-back | 2,771 | 2,894 | 3,117 | 6,266 | 6,007 | 5,220 |

| (Increase)/decrease in working capital | 29,775 | (33,060) | (31,685) | (26,208) | (25,008) | (4,623) |

| Other operating cash flow items | 5,574 | 9,648 | 17,999 | - | - | - |

| Cash flow from operating | 52,087 | 8,030 | 30,330 | 21,855 | 32,801 | |

| 59,911 | ||||||

| Capital expenditure Other investment cash flow items | (1,688) 3,895 | (2,068) (1,123) | (985) (7,198) | (1,891) - | (1,934) - | (1,965) - |

| Cash flow from investing | 2,206 | (3,190) | (8,183) | (1,891) | (1,934) | (1,965) |

| Dividends paid | (11,141) | (12,627) | (25,254) | (31,196) | (29,263) | (36,268) |

| Change in common stock | - | - | - | - | - | - |

| Increase/(decrease) in short-term debt | (32,635) | 9,024 | 4,458 | - | - | - |

| Increase/(decrease) in long-term debt | 17 | 204 | (73) | - | - | - |

| Other financing cash flow items | (1,481) | 8,204 | (2,352) | - | - | - |

| Cash flow from financing | (45,240) | 4,806 | (23,221) | (31,196) | (29,263) | (36,268) |

| Net change in cash | 9,904 | 14,811 | (3,959) | (11,231) | 1,603 | 21,677 |

| FCF | 50,399 | 5,963 | 29,345 | 19,965 | 30,867 | 57,945 |

| Ratio | 0.2% | |||||

| Capex to revenue | 0.4% | 0.4% | 0.1% | 0.2% | 0.2% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Price Target Risks and Methodology - Asus

We are Neutral rated on ASUS with a 12-month target price of NT$1,082. Our TP is based on 15.8x 2027E P/E, which is based on brand makers' avg. ratio of 2027E PE to 2028E NI YoY and OPM. We see EPS growth and OPM as a major factor for the stock's share performance.

Key upside / downside risks include: 1) stronger / weaker-than-expected PC market growth, 2) faster / slower-than-expected AI and gaming PC growth, and 3) faster / slower-than-expected AI servers ramp-up.

| 2357.TW | 12m Price Target: NT$1,082.00 | 12m Price Target: NT$1,082.00 | Price: NT$900.00 | Price: NT$900.00 | Upside: 20.2% | Upside: 20.2% |

|---|---|---|---|---|---|---|

| Neutral | Neutral | GS Forecast | GS Forecast | GS Forecast | GS Forecast | GS Forecast |

| Market c ap: NT$668.5b n / $ 21 . 2 b n | Market c ap: NT$668.5b n / $ 21 . 2 b n | Revenue ( NT$m n ) N e w Revenue (NT$ mn) Old EBITDA (NT$ mn) E PS ( NT$) N e w | 12/25 7 3 8 ,904. 8 | 12/26E 85 9,449. 5 | 12/27E 9 67 ,0 7 9.9 | 12/28E 1 ,0 62 ,4 17 . 7 |

| En terpr is e v a lu e: | En terpr is e v a lu e: | 738,904.8 | 831,325.3 | 876,896.8 | 937,464.3 | |

| NT$6 49 . 0 b n / $ 20 .6b n | NT$6 49 . 0 b n / $ 20 .6b n | 42,773.2 | 51,233.2 | 63,639.2 | 72,633.4 | |

| 3m AD T V : NT$ 3 .5b n / $ 109 .8 mn | 3m AD T V : NT$ 3 .5b n / $ 109 .8 mn | 5 9.99 | 56 . 27 | 6 9. 7 4 | 7 9. 1 3 | |

| Ta iw a n | Ta iw a n | EPS (NT$) Old | 59.99 | 53.99 | 62.19 | 69.22 |

| G reater Chin a Te chnology | G reater Chin a Te chnology | P/E (X) | 10.6 | 16.0 | 12.9 | 11.4 |

| M &A R a n k: 3 | M &A R a n k: 3 | P/B (X) | 1.8 | 2.4 | 2.3 | 2.2 |

| L ea s e s incl . in n et d ebt & EV? : s | L ea s e s incl . in n et d ebt & EV? : s | Dividend yield (%) | 6.5 | 4.3 | 5.3 | 6.1 |

| Y e | Y e | CROCI (%) | 26.9 | 19.7 | 22.1 | 22.7 |

| 3 /26 | 6/26E | 9 /26E | 12/26E | |||

| EPS (NT$) | 13.19 | 13.62 | 15.35 | 14.11 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 5 Jun 2026 close.

e92c7a75ab8b4efbba794e6b187208c8

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260606_2357_華碩_gs_asustek_001.png |

57KB | 真資料圖 | 營收長條圖+YoY%折線圖,縱軸左 NT$m(0-100,000)、右 YoY%(-60%~120%),橫軸 Jan-11至Sep-25,藍色柱狀為「Series1」,紅線為「YoY (RHS)」 |

260606_2357_華碩_gs_asustek_002.png |

54KB | 真資料圖 | 標題「Exhibit 8: ASUS 12M forward PE ratio」藍線走勢圖,橫軸 Jan-19至May-26,縱軸0-30x,標示三條水平虛線:+1st.v 14.4x、avg 10.2x、-1st.v 5.9x |

260606_2357_華碩_gs_asustek_003.png |

58KB | 真資料圖 | 標題「Exhibit 9: ASUS QFII」藍線走勢圖,橫軸Jan-19至May-26,縱軸0-70%,標示三個數字節點66%(起點)、42%(低點)、36%(末端),來源 TEJ |

260606_2357_華碩_gs_asustek_004.png |

80KB | 真資料圖 | 標題「Asus (2357.TW) Goldman Sachs rating and stock price target history」雙軸圖:藍色方塊為評等區間(NA/B/N,含日期)、藍點+數字為歷次目標價(522~890區間多個數字)、淺藍線為股價、灰線為Taiwan SE Weighted Index,來源 Goldman Sachs Investment Research,FactSet closing prices as of 3/31/2026 |