PDF 原檔:260605_2059_川湖_gs_kingslide_original.pdf

原始內容

King Slide (2059.TW): AI server rail kits ramp up, supporting solid growth; TP raised to NT$7,664; Buy

King Slide April revenues increased by 35% MoM/ 79% YoY to NT$2.6bn, or 16% ahead of estimates, and we attribute it to AI server rail kit ramp up and general server rail kit growth. The strong growth echos our positive view on company's leading market positions in AI server rail kits, supported by its comprehensive architecture across rack/ baseboard/ ASIC, strong patents (~3.7k patents approved as of May 2026), diversi fi ed client group, and its high customization ability. Amid the larger revenues scale, the company's 1Q26 GM was up to 77.7% (vs. 76.0% in 2025) with automated production and strong cost control, and the company continues the capacity expansion to capture the growth opportunities. Maintain Buy with TP raised to NT$7,664.

Monthly revenues preview: For coming months, we model 68%/ 33% YoY revenues growth in May/ Jun 2026, while MoM decline on the high base and model transition, resulting in strong growth of 2Q26E revenues at 60% YoY/ 24% QoQ. We expect to see MoM increase from July, with accelerated ramp-up of rack-level AI servers, riding on dollar content increase, and the additional capacity expansion.

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Ting Song

+852-2978-6466 | ting.song@gs.com Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

\

Exhibit 1: We expect King Slide May/ Jun revenues to grow 68%/ 33% YoY King Slide monthly/ quarterly revenues

| Jan-26 | 26-Feb | 26-Mar | 26-Apr | May-26 (E) | Jun-26 (E) | Jul-26 (E) | Aug-26 (E) | Sep-26 (E) | 4Q25 | 1Q26 | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 1,775 | 1,757 | 1,918 | 2,596 | 2,336 | 1,842 | 2,118 | 2,542 | 3,009 | 4,949 | 5,450 | 6,774 | 7,670 |

| Rev YoY | 44% | 31% | 39% | 79% | 68% | 33% | 51% | 75% | 100% | 60% | 38% | 60% | 76% |

| RevMoM/QoQ | 3% | -1% | 9% | 35% | -10% | -21% | 15% | 20% | 18% | 13% | 10% | 24% | 13% |

| GS estimates | 1,627 | 1615 | 2,060 | 2,245 | 4,825 | 5,056 | |||||||

| Act. Vs. GS | 9% | 9% | -7% | 16% | 3% | 8% |

Source: Company data, Goldman Sachs Global Investment Research

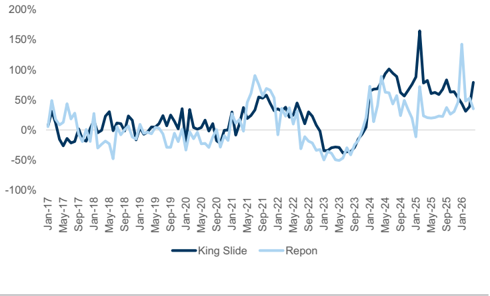

Exhibit 2: Monthly revenues YoY: King Slide vs. Repon

Source: Company data

Exhibit 4: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT$m | Old | New | Diff% | Old | New | Diff% | Old | New | Diff% |

| Revenues | 26,679 | 28,406 | 6% | 36,868 | 40,797 | 11% | 41,802 | 50,306 | 20% |

| GP | 20,001 | 21,698 | 8% | 27,343 | 31,054 | 14% | 30,948 | 38,701 | 25% |

| OP | 18,814 | 18,663 | -1% | 26,139 | 29,246 | 12% | 29,583 | 36,472 | 23% |

| Net income | 15,484 | 16,220 | 5% | 21,272 | 24,373 | 15% | 23,991 | 30,198 | 26% |

| Margins | |||||||||

| GM | 75.0% | 76.4% | 74.2% | 76.1% | 74.0% | 76.9% | |||

| OPM | 70.5% | 65.7% | 70.9% | 71.7% | 70.8% | 72.5% | |||

| NM | 58.0% | 57.1% | 57.7% | 59.7% | 57.4% | 60.0% |

Source: Company data, Goldman Sachs Global Investment Research

GSe vs. Bloomberg consensus: Our 2026E earnings are largely in line with consensus. Our 2027E earnings are 23% higher than Bloomberg consensus, mainly due to higher revenues of rack-level AI server rail kits, given our positive outlook of rising rail kits adoption in AI data centers and company's leading position in the market with customization capabilities.

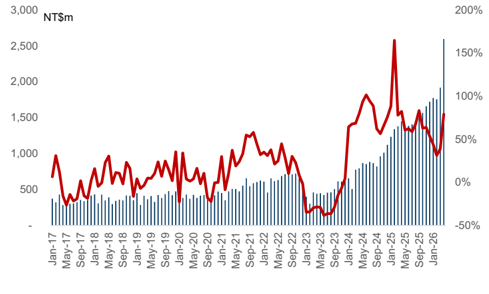

Exhibit 3: King Slide monthly revenues and YoY trend

Source: Company data

Earnings revision: We raise NI by 5%/ 15%/ 26% in 2026-28E mainly on higher revenues and higher GM. Revenues are raised on higher growth of (1) rack-level AI server rail kit, (2) baseboard-based AI server rail kit, (3) general server rail kit, as we factor in the latest server TAM estimates with higher shipment, and we expect King Slide to maintain leading position, meanwhile bene fi ting from the dollar content increase. We raise 2026-28E GM to re fl ect company's product mix upgrade towards high-end solution, and strong cost controls with larger business scale to support better pro fi tability e92c7a75ab8b4efbba794e6b187208c8

Exhibit 5: GSe vs. consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | |

|---|---|---|---|---|---|---|

| NT$m | GS | Cons. | Diff% | GS | Cons. | Diff% |

| Revenues | 28,406 | 27,474 | 3% | 40,797 | 34,287 | 19% |

| GP | 21,698 | 21,200 | 2% | 31,054 | 26,396 | 18% |

| OP | 18,663 | 19,107 | -2% | 29,246 | 24,021 | 22% |

| Net income | 16,220 | 16,189 | 0% | 24,373 | 19,747 | 23% |

| Margins | ||||||

| GM | 76.4% | 77.2% | 76.1% | 77.0% | ||

| OPM | 65.7% | 69.5% | 71.7% | 70.1% | ||

| NM | 57.1% | 58.9% | 59.7% | 57.6% |

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg

Valuation: We continue to use near-term P/E to derive our target price. We continue to derive the target P/E multiple via high-end of the company's PEG (0.8x), and with 37% avg. NI YoY in 2027-28E, our new target P/E multiple is now at 30x 2027E EPS (vs. previously at 20x). Nevertheless, our new target P/E is in the range of King Slide's historical P/E since 2019. With the updated target P/E, our 12M TP is revised up to NT$7,664 (vs. previously at NT$4,386). Maintain Buy.

Exhibit 6: King Slide P&L Summary

| NT$m | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Income statement | |||||||||||||||

| Revenue | 7,799 | 5,763 | 10,129 | 17,501 | 28,406 | 40,797 | 50,306 | 3,954 | 4,229 | 4,369 | 4,949 | 5,450 | 6,774 | 7,670 | 8,512 |

| Gross profit | 4,466 | 3,532 | 7,002 | 13,309 | 21,698 | 31,054 | 38,701 | 3,007 | 3,277 | 3,258 | 3,766 | 4,237 | 5,099 | 5,837 | 6,526 |

| Opex | (707) | (658) | (898) | (1,220) | (3,034) | (1,807) | (2,229) | (285) | (245) | (347) | (344) | (582) | (724) | (819) | (909) |

| OP income | 3,753 | 2,888 | 6,101 | 12,089 | 18,663 | 29,246 | 36,472 | 2,723 | 2,966 | 2,975 | 3,424 | 3,654 | 4,375 | 5,018 | 5,617 |

| Net income | 4,056 | 2,704 | 6,156 | 9,837 | 16,220 | 24,373 | 30,198 | 2,511 | 614 | 3,197 | 3,514 | 3,486 | 3,742 | 4,257 | 4,735 |

| EPS (diluted, NT$) | 41.84 | 28.02 | 63.44 | 101.36 | 170.02 | 255.47 | 316.53 | 26.32 | 6.44 | 33.52 | 35.08 | 36.54 | 39.23 | 44.62 | 49.63 |

| Margins | |||||||||||||||

| Gross margin | 57.3% | 61.3% | 69.1% | 76.0% | 76.4% | 76.1% | 76.9% | 76.1% | 77.5% | 74.6% | 76.1% | 77.7% | 75.3% | 76.1% | 76.7% |

| Operating margin | 48.1% | 50.1% | 60.2% | 69.1% | 65.7% | 71.7% | 72.5% | 68.9% | 70.1% | 68.1% | 69.2% | 67.1% | 64.6% | 65.4% | 66.0% |

| Net margin | 52.0% | 46.9% | 60.8% | 56.2% | 57.1% | 59.7% | 60.0% | 63.5% | 14.5% | 73.2% | 71.0% | 64.0% | 55.2% | 55.5% | 55.6% |

| Ratios | |||||||||||||||

| Opex ratio | 9.1% | 11.4% | 8.9% | 7.0% | 10.7% | 4.4% | 4.4% | 7.2% | 5.8% | 7.9% | 6.9% | 10.7% | 10.7% | 10.7% | 10.7% |

| Tax rate | 20% | 21% | 21% | 21% | 20% | 20% | 20% | 20% | 32% | 20% | 20% | 20% | 20% | 20% | 20% |

| YoY | |||||||||||||||

| Revenue | 23% | -26% | 76% | 73% | 62% | 44% | 23% | 104% | 68% | 70% | 60% | 38% | 60% | 76% | 72% |

| Gross profit | 33% | -21% | 98% | 90% | 63% | 43% | 25% | 149% | 87% | 79% | 69% | 41% | 56% | 79% | 73% |

| OP income | 38% | -23% | 111% | 98% | 54% | 57% | 25% | 169% | 93% | 85% | 76% | 34% | 47% | 69% | 64% |

| Net income | 96% | -33% | 128% | 60% | 65% | 50% | 24% | 81% | -58% | 177% | 63% | 39% | 509% | 33% | 35% |

| QoQ | |||||||||||||||

| Revenue | 28% | 7% | 3% | 13% | 10% | 24% | 13% | 11% | |||||||

| Gross profit | 35% | 9% | -1% | 16% | 12% | 20% | 14% | 12% | |||||||

| OP income | 40% | 9% | 0% | 15% | 7% | 20% | 15% | 12% | |||||||

| Net income | 16% | -76% | 421% | 10% | -1% | 7% | 14% | 11% |

Source: Company data, Goldman Sachs Global Investment Research

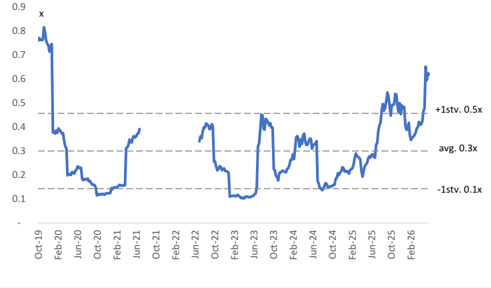

Exhibit 7: King Slide 12M forward PEG

Source: Company data, Goldman Sachs Global Investment Research

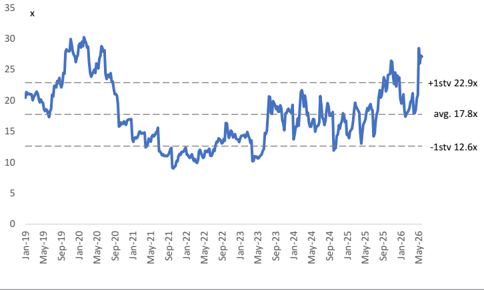

Exhibit 8: King Slide 12M forward PE ratio

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg e92c7a75ab8b4efbba794e6b187208c8

Price Target Risks and Methodology - King Slide

Valuation methodology : Our 12m target price for King Slide is based on a near-term P/E, consistent with our Taiwan Technology coverage. Our 12m TP of NT$7,664 is based on a target P/E multiple of 30x on our forward year EPS (2027E). Our target P/E is derived from the company's peak PEG at 0.8x, as we expect the migration to AI server rail kits to drive the company's pro fi tability.

Downside risks: (1) New entrants intensifying competition, (2) slower-than-expected AI server growth, (3) lower-than-expected general server shipment growth.

| 2059.TW | 12m Price Target: NT$7,664.00 | Price: NT$5,350.00 | Upside: 43.3% | Upside: 43.3% |

|---|---|---|---|---|

| Buy | Buy | |||

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | Revenue ( NT$m n ) N e w Revenue (NT$ mn) Old EBITDA (NT$ mn) E PS ( NT$) N e w EPS (NT$) Old P/E (X) P/B (X) | 12/25 12/26E 17 , 5 00. 7 28 ,40 6 .0 26,678.8 12,449.1 2 3 103.23 24.9 8.7 2.0 158.4 | 12/27E 40, 7 9 7 . 2 | 12/28E 5 0,30 6 .0 |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 17,500.7 | 36,867.8 | 41,801.9 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 19,054.3 | 29,684.0 | 36,915.1 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 1 03. 17 0. 21 | 255 . 75 | 3 16 . 88 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 162.48 | 223.21 | 251.75 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 31.4 | 20.9 | 16.9 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 14.1 | 10.5 | 8.0 | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | Dividend yield (%) | 1.6 | 2.4 | 2.9 |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | C RO C I (%) | 193.7 | 289.4 | 390.1 |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | 3 /26 6/26E | 9 /26E | 12/26E | |

| Market c ap: NT$510.4 bn / $1 6 . 2bn En terpr is e v a lu e: NT$4 79 . 7bn / $15. 2bn 3m AD T V : NT$ 2 . 8bn / $ 88 .1 mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 L ea s e s incl . in n et d e b t & EV? : Y e s | EPS (NT$) | 36.58 39.27 | 44.67 | 49.69 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 4 Jun 2026 close.

e92c7a75ab8b4efbba794e6b187208c8

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260605_2059_川湖_gs_kingslide_001.png |

41KB | 真資料圖 | 折線圖(對應原文 Exhibit 2: Monthly revenues YoY),King Slide 與 Repon 百分比走勢對比,橫軸 Jan-17至2026 |

260605_2059_川湖_gs_kingslide_003.png |

33KB | 真資料圖 | 倍數走勢折線圖(對應原文 Exhibit 7: King Slide 12M forward PEG,縱軸x倍數),含 avg 0.3x、+1stv 0.5x、-1stv 0.1x 虛線標示,橫軸 Oct-19至Feb-26 |

260605_2059_川湖_gs_kingslide_004.png |

38KB | 真資料圖 | 本益比倍數走勢折線圖(縱軸x倍數),含 +1stv 22.9x、avg 17.8x、-1stv 12.6x 虛線標示,橫軸 Jan-19至May-26 |