PDF 原檔:260601_6805_富世達_daiwa_Fositek_original.pdf

原始內容

Fositek Corp (6805 TT)

Target price:

TWD2,600.00 (from TWD2,600.00)

Share price (1 Jun):

TWD2,120.00

|

Up/downside:

+22.6%

Positive tone on the 2026-27 outlook

- Stronger revenue outlook in 2H26 vs. 1H26

- The server segment should be the key revenue driver

- Reaffirming our Buy (1) rating with an unchanged 12M TP of TWD2,600

What's new: Fositek joined our Daiwa Corporate Day on 29 May and shared an update on its business. We expect the company to benefit from the AI server trend in the coming years, with rising server revenue from QDs and slides over 2026-28E and share-gain potential in GPU and ASIC applications. We reaffirm our Buy (1) rating. See our previous flash, Server segment should be the key earnings driver , 7 May 2026.

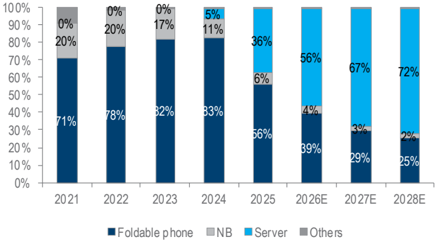

What's the impact: Positive tone from the investor conference. For 2Q26, Fositek guided revenue to be flat to up 5% QoQ, with double-digit QoQ revenue growth in both 3Q26 and 4Q26. We believe 2H26 revenue should be stronger than 1H26, supported by more ASIC projects, VR, LPX and Vera CPU projects. For CPO, Fositek is sampling QDs to CSP and GPU clients, which is likely to contribute revenue in 2027, according to management. Apart from AVC (see our latest flash on 14 May), Fositek is also testing with other thermal solution vendors, as well as new segments such as power rack. For slides, the company plans to tap into the liquid cooling segment in 2H26, with target revenue set to more than double YoY in 2026. For hinges for foldable phones, Fositek aims for flat YoY revenue in 2026, with the launch of three-fold phones in 3Q26 in a sole-supplier position. The company is also positive on the 2027 outlook, thanks to rising liquid cooling applications in VR and ASICs. It sees a high utilisation rate for QDs, with intact order visibility (without product transition concerns), and we believe there could be some upside potential to gross margin on improving yield rates and automation levels. On the gross margin side, Fositek expects to grow QoQ in 2026. We slightly cut our 2026E EPS by 2% on more conservative revenue assumptions, but raise our 2027-28E EPS by 4-5% on our more aggressive revenue and gross margin assumptions. Note: Its product mix for 1Q26 is as below: foldable phone 37.7% (-4.7% YoY), notebook 5.2% (+6.2% YoY), server 56.4% (+546.9% YoY) and others 0.7% (+8.4% YoY); its April 2026 product mix is: foldable phone 40.2%, notebook 5.7%, server 53.5% and others 0.6%

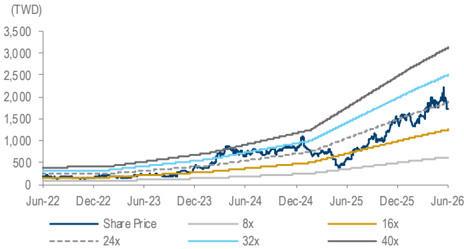

What we recommend: We reaffirm our Buy (1) call with an unchanged 12M TP of TWD2,600, still based on a target PER of 33x (vs. its past-3year range of 9-43x [average of 23x]), translating to a 0.42x PEG over 2025-27E on our 1-year forward EPS. Key downside risks: lower-thanexpected market share for key clients; slower-than-expected penetration rate of foldable phones; and geopolitical risks.

How we differ: Our 2026-28E EPS are 1-7% above Bloomberg consensus, likely as we are more positive on its revenue and gross margins.

Helen Chien

(886) 2 8758 6254

helen.chien@daiwacm-cathay.com.tw

Neil Teng (886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | (4.6) | 2.8 | 3 |

| Net profit change | (2.1) | 4.7 | 4.8 |

| Core EPS (FD) change | (2.1) | 4.7 | 4.8 |

Source: Daiwa forecasts

Share price performance

| 12-month range | 580.00-2,215.00 |

|---|---|

| Market cap (USDbn) | 4.64 |

| 3m avg daily turnover (USDm) | 125.53 |

| Shares outstanding (m) | 69 |

| Major shareholder | AVC (16.9%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 18,644 | 26,294 | 31,998 |

| Operating profit (m) | 5,314 | 7,914 | 9,839 |

| Net profit (m) | 4,560 | 6,720 | 8,318 |

| Core EPS (fully-diluted) | 66.473 | 97.964 | 121.257 |

| EPS change (%) | 114.6 | 47.4 | 23.8 |

| Daiwa vs Cons. EPS (%) | 3.5 | 0.9 | 7.4 |

| PER (x) | 31.9 | 21.6 | 17.5 |

| Dividend yield (%) | 1.6 | 2.3 | 2.9 |

| DPS | 33.3 | 49.0 | 60.7 |

| PBR (x) | 12.9 | 9.3 | 7.1 |

| EV/EBITDA (x) | 23.4 | 15.5 | 12.0 |

| ROE (%) | 49.4 | 49.9 | 45.9 |

Source: FactSet, Daiwa forecasts

Fositek: revenue and earnings forecast revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | New | Previous | Change | New | Previous | Change | New | Previous | Change |

| Sales | 18,644 | 19,546 | -4.6% | 26,294 | 25,573 | 2.8% | 31,998 | 31,061 | 3.0% |

| Gross profit | 6,283 | 6,450 | -2.6% | 9,071 | 8,695 | 4.3% | 11,199 | 10,716 | 4.5% |

| Gross margin | 33.7% | 33.0% | 0.7pp | 34.5% | 34.0% | 0.5pp | 35.0% | 34.5% | 0.5pp |

| Operating profit | 5,314 | 5,434 | -2.2% | 7,914 | 7,570 | 4.6% | 9,839 | 9,396 | 4.7% |

| Operating margin | 28.5% | 27.8% | 0.7pp | 30.1% | 29.6% | 0.5pp | 30.8% | 30.3% | 0.5pp |

| Net profit | 4,560 | 4,660 | -2.1% | 6,720 | 6,417 | 4.7% | 8,318 | 7,933 | 4.8% |

| Net margin | 24.5% | 23.8% | 0.6pp | 25.6% | 25.1% | 0.5pp | 26.0% | 25.5% | 0.5pp |

| Fully diluted EPS (TWD) | 66.47 | 67.92 | -2.1% | 97.96 | 93.55 | 4.7% | 121.26 | 115.65 | 4.8% |

Source: Daiwa forecasts

Fositek: quarterly and annual P&L

| 2026E | 2026E | 2026E | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2027E | ||

| Revenue | 4,184 | 4,253 | 4,700 | 5,508 | 5,400 | 5,800 | 7,100 | 7,994 | 18,644 | 26,294 | 31,998 |

| Gross profit | 1,352 | 1,404 | 1,598 | 1,930 | 1,809 | 1,972 | 2,428 | 2,862 | 6,283 | 9,071 | 11,199 |

| Operating profit | 1,120 | 1,159 | 1,353 | 1,682 | 1,544 | 1,697 | 2,153 | 2,520 | 5,314 | 7,914 | 9,839 |

| Pre-tax profit | 1,165 | 1,204 | 1,398 | 1,727 | 1,590 | 1,743 | 2,199 | 2,566 | 5,494 | 8,097 | 10,022 |

| Net profit | 917 | 1,011 | 1,174 | 1,457 | 1,319 | 1,446 | 1,825 | 2,130 | 4,560 | 6,720 | 8,318 |

| Basic EPS (TWD) | 13.38 | 14.75 | 17.13 | 21.26 | 19.24 | 21.10 | 26.62 | 31.06 | 66.52 | 98.03 | 121.33 |

| Margin | |||||||||||

| Gross margin | 32.3% | 33.0% | 34.0% | 35.0% | 33.5% | 34.0% | 34.2% | 35.8% | 33.7% | 34.5% | 35.0% |

| Operating margin | 26.8% | 27.2% | 28.8% | 30.5% | 28.6% | 29.3% | 30.3% | 31.5% | 28.5% | 30.1% | 30.8% |

| Pre-tax margin | 27.9% | 28.3% | 29.7% | 31.4% | 29.4% | 30.0% | 31.0% | 32.1% | 29.5% | 30.8% | 31.3% |

| Net margin | 21.9% | 23.8% | 25.0% | 26.5% | 24.4% | 24.9% | 25.7% | 26.6% | 24.5% | 25.6% | 26.0% |

| YoY | |||||||||||

| Revenue | 85.8% | 62.3% | 31.8% | 38.5% | 29.1% | 36.4% | 51.1% | 45.1% | 50.2% | 41.0% | 21.7% |

| Gross profit | 171.2% | 122.6% | 62.0% | 67.1% | 33.8% | 40.5% | 52.0% | 48.3% | 92.1% | 44.4% | 23.5% |

| Operating profit | 206.3% | 133.2% | 70.7% | 93.5% | 37.8% | 46.5% | 59.1% | 49.9% | 110.5% | 48.9% | 24.3% |

| Pre-tax profit | 177.1% | 205.0% | 68.4% | 92.1% | 36.4% | 44.8% | 57.3% | 48.6% | 115.9% | 47.4% | 23.8% |

| Net profit | 157.3% | 206.0% | 71.0% | 93.9% | 43.8% | 43.1% | 55.4% | 46.1% | 114.6% | 47.4% | 23.8% |

| QoQ | |||||||||||

| Revenue | 5.2% | 1.7% | 10.5% | 17.2% | -2.0% | 7.4% | 22.4% | 12.6% | |||

| Gross profit | 17.1% | 3.8% | 13.9% | 20.8% | -6.3% | 9.0% | 23.1% | 17.9% | |||

| Operating profit | 28.9% | 3.4% | 16.8% | 24.3% | -8.2% | 9.9% | 26.9% | 17.0% | |||

| Pre-tax profit | 29.6% | 3.3% | 16.2% | 23.5% | -8.0% | 9.6% | 26.2% | 16.7% | |||

| Net profit | 22.1% | 10.2% | 16.2% | 24.1% | -9.5% | 9.6% | 26.2% | 16.7% |

Source: Company, Daiwa forecasts

Fositek: product mix

Source: Company, Daiwa forecasts

Fositek: 1-year forward PER

Source: Bloomberg, Daiwa forecasts

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Foldable phone revenue YoY growth | 0 | 8.9 | 19.1 | 45.9 | 3.6 | 5 | 5 | 5 |

| (%) NB YoY growth (%) | 0 | 2.4 | (5.5) | (7.7) | (11.1) | 0 | 0 | 0 |

| Server revenue YoY growth (%) | 0 | 0 | 0.0 | 0.0 | 935.9 | 130 | 70 | 30 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Foldable phone | 3,572 | 3,889 | 4,633 | 6,759 | 7,001 | 7,352 | 7,719 | 8,105 |

| Server | 0 | 0 | 0 | 435 | 4,506 | 10,364 | 17,619 | 22,905 |

| Other Revenue | 1,449 | 1,125 | 1,011 | 994 | 906 | 929 | 955 | 988 |

| Total Revenue | 5,020 | 5,014 | 5,644 | 8,188 | 12,414 | 18,644 | 26,294 | 31,998 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (3,827) | (3,848) | (4,326) | (6,361) | (9,144) | (12,361) | (17,223) | (20,799) |

| SG&A | (133) | (153) | (151) | (180) | (187) | (261) | (342) | (400) |

| Other op.expenses | (251) | (238) | (286) | (450) | (559) | (708) | (815) | (960) |

| Operating profit | 809 | 775 | 881 | 1,197 | 2,524 | 5,314 | 7,914 | 9,839 |

| Net-interest inc./(exp.) | (9) | (15) | 1 | 52 | 41 | 43 | 42 | 42 |

| Assoc/forex/extraord./others | (24) | 76 | 30 | 245 | (21) | 138 | 140 | 140 |

| Pre-tax profit | 776 | 835 | 911 | 1,495 | 2,545 | 5,494 | 8,097 | 10,022 |

| Tax | (243) | (271) | (283) | (267) | (419) | (934) | (1,376) | (1,704) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 533 | 564 | 628 | 1,227 | 2,125 | 4,560 | 6,720 | 8,318 |

| Net profit (adjusted) | 533 | 564 | 628 | 1,227 | 2,125 | 4,560 | 6,720 | 8,318 |

| EPS (reported)(TWD) | 9.289 | 9.331 | 10.185 | 17.904 | 31.002 | 66.515 | 98.027 | 121.335 |

| EPS (adjusted)(TWD) | 9.289 | 9.331 | 10.185 | 17.904 | 31.002 | 66.515 | 98.027 | 121.335 |

| EPS (adjusted fully-diluted)(TWD) | 9.276 | 9.311 | 10.174 | 17.890 | 30.982 | 66.473 | 97.964 | 121.257 |

| DPS (TWD) | 3.688 | 4.000 | 6.115 | 8.000 | 10.500 | 33.258 | 49.013 | 60.667 |

| EBIT | 809 | 775 | 881 | 1,197 | 2,524 | 5,314 | 7,914 | 9,839 |

| EBITDA | 910 | 966 | 1,043 | 1,638 | 2,801 | 5,776 | 8,473 | 10,492 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 776 | 835 | 911 | 1,495 | 2,545 | 5,494 | 8,097 | 10,022 |

| Depreciation and amortisation | 126 | 115 | 132 | 196 | 298 | 325 | 419 | 513 |

| Tax paid | (78) | (128) | (125) | (173) | (337) | (934) | (1,376) | (1,704) |

| Change in working capital | (726) | 1,400 | 221 | (212) | (260) | (562) | (16) | (257) |

| Other operational CF items | 386 | 96 | 80 | 103 | (274) | (43) | (42) | (42) |

| Cash flow from operations | 484 | 2,318 | 1,218 | 1,409 | 1,970 | 4,280 | 7,081 | 8,532 |

| Capex | (204) | (106) | (189) | (541) | (322) | (500) | (500) | (500) |

| Net (acquisitions)/disposals | 0 | 3 | 5 | (70) | 6 | 0 | 0 | 0 |

| Other investing CF items | 54 | (16) | 2 | (53) | (47) | 0 | 0 | 0 |

| Cash flow from investing | (150) | (119) | (182) | (664) | (362) | (500) | (500) | (500) |

| Change in debt | 644 | 77 | (521) | (10) | (10) | 0 | 0 | 0 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (19) | (272) | (242) | (377) | (548) | (720) | (2,280) | (3,360) |

| Other financing CF items | 650 | (19) | 1,833 | (35) | (45) | 0 | 0 | 0 |

| Cash flow from financing | 1,275 | (214) | 1,071 | (422) | (603) | (720) | (2,280) | (3,360) |

| Forex effect/others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Change in cash | 1,609 | 1,985 | 2,107 | 324 | 1,005 | 3,060 | 4,301 | 4,672 |

| Free cash flow | 280 | 2,131 | 949 | 713 | 1,881 | 3,780 | 6,581 | 8,032 |

Source: FactSet, Daiwa forecasts

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 1,854 | 3,841 | 5,898 | 6,336 | 7,446 | 10,506 | 14,808 | 19,479 |

| Inventory | 1,111 | 943 | 999 | 2,902 | 3,606 | 5,584 | 6,641 | 8,258 |

| Accounts receivable | 1,375 | 452 | 1,462 | 2,166 | 2,300 | 4,189 | 5,388 | 6,873 |

| Other current assets | 49 | 36 | 105 | 260 | 143 | 143 | 143 | 143 |

| Total current assets | 4,390 | 5,272 | 8,464 | 11,664 | 13,494 | 20,422 | 26,979 | 34,753 |

| Fixed assets | 324 | 312 | 359 | 758 | 817 | 992 | 1,073 | 1,060 |

| Goodwill & intangibles | 13 | 12 | 15 | 18 | 17 | 17 | 17 | 17 |

| Other non-current assets | 113 | 107 | 92 | 318 | 351 | 351 | 351 | 351 |

| Total assets | 4,840 | 5,704 | 8,930 | 12,758 | 14,678 | 21,781 | 28,420 | 36,181 |

| Short-term debt | 369 | 703 | 440 | 430 | 420 | 420 | 420 | 420 |

| Accounts payable | 1,502 | 1,865 | 3,224 | 5,811 | 5,911 | 9,215 | 11,454 | 14,297 |

| Other current liabilities | 129 | 133 | 166 | 291 | 503 | 228 | 228 | 228 |

| Total current liabilities | 1,999 | 2,701 | 3,830 | 6,533 | 6,833 | 9,863 | 12,102 | 14,946 |

| Long-term debt | 515 | 258 | 22 | 22 | 22 | 22 | 22 | 22 |

| Other non-current liabilities | 256 | 359 | 483 | 657 | 629 | 629 | 629 | 629 |

| Total liabilities | 2,770 | 3,318 | 4,335 | 7,212 | 7,485 | 10,515 | 12,754 | 15,597 |

| Share capital | 605 | 605 | 686 | 686 | 686 | 686 | 686 | 686 |

| Reserves/R.E./others | 1,466 | 1,781 | 3,910 | 4,861 | 6,507 | 10,581 | 14,980 | 19,898 |

| Shareholders' equity | 2,070 | 2,386 | 4,595 | 5,546 | 7,193 | 11,266 | 15,666 | 20,583 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 4,840 | 5,704 | 8,930 | 12,758 | 14,678 | 21,781 | 28,420 | 36,181 |

| EV | 144,364 | 142,454 | 139,898 | 139,451 | 138,331 | 135,271 | 130,969 | 126,298 |

| Net debt/(cash) | (971) | (2,880) | (5,437) | (5,884) | (7,003) | (10,064) | (14,365) | (19,037) |

| BVPS (TWD) | 36.079 | 39.467 | 74.534 | 80.906 | 104.919 | 164.339 | 228.520 | 300.250 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 125.8 | (0.1) | 12.6 | 45.1 | 51.6 | 50.2 | 41.0 | 21.7 |

| EBITDA (YoY) | 158.0 | 6.1 | 8.0 | 57.1 | 71.0 | 106.2 | 46.7 | 23.8 |

| Operating profit (YoY) | 179.5 | (4.2) | 13.7 | 36.0 | 110.8 | 110.5 | 48.9 | 24.3 |

| Net profit (YoY) | 153.3 | 5.8 | 11.3 | 95.5 | 73.2 | 114.6 | 47.4 | 23.8 |

| Core EPS (fully-diluted) (YoY) | 48.7 | 0.4 | 9.3 | 75.8 | 73.2 | 114.6 | 47.4 | 23.8 |

| Gross-profit margin | 23.8 | 23.3 | 23.3 | 22.3 | 26.3 | 33.7 | 34.5 | 35.0 |

| EBITDA margin | 18.1 | 19.3 | 18.5 | 20.0 | 22.6 | 31.0 | 32.2 | 32.8 |

| Operating-profit margin | 16.1 | 15.5 | 15.6 | 14.6 | 20.3 | 28.5 | 30.1 | 30.8 |

| Net profit margin | 10.6 | 11.3 | 11.1 | 15.0 | 17.1 | 24.5 | 25.6 | 26.0 |

| ROAE | 36.1 | 25.3 | 18.0 | 24.2 | 33.4 | 49.4 | 49.9 | 45.9 |

| ROAA | 13.9 | 10.7 | 8.6 | 11.3 | 15.5 | 25.0 | 26.8 | 25.8 |

| ROCE | 39.6 | 24.6 | 21.0 | 21.7 | 37.0 | 54.9 | 56.9 | 53.0 |

| ROIC | 56.2 | n.a | n.a. | n.a. | n.a. | n.a | n.a | n.a |

| Net debt to equity | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Effective tax rate | 31.3 | 32.4 | 31.1 | 17.9 | 16.5 | 17.0 | 17.0 | 17.0 |

| Accounts receivable (days) | 65.8 | 66.5 | 61.9 | 80.9 | 65.7 | 63.5 | 66.5 | 69.9 |

| Current ratio (x) | 2.2 | 2.0 | 2.2 | 1.8 | 2.0 | 2.1 | 2.2 | 2.3 |

| Net interest cover (x) | 91.5 | 50.1 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Net dividend payout | 39.7 | 42.9 | 60.0 | 44.7 | 33.9 | 50.0 | 50.0 | 50.0 |

| Free cash flow yield | 0.2 | 1.5 | 0.7 | 0.5 | 1.3 | 2.6 | 4.5 | 5.5 |

Source: FactSet, Daiwa forecasts

Company profile

Fositek is a provider of foldable phone hinges, foldable laptop/tablet hinges, AR/VR glasses hinges, ultra-thin laptop hinges and keyboard hinges, as well as hinges for medical instruments and automobile applications. Its major clients include Huawei and Motorola.

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| G | Executive/board quality | 1 | The CEO and chairperson of Fositek are not the same individual, and we see no issue with its board quality. Besides, we note that the chairperson has 24 years of experience in this industry and took over the role of chairman at Fositek in 2014, which is a positive sign from a governance perspective. |

| G | Capital management | 2 | Fositek's dividend payout ratio was 40-60% over 2022-25, due likely to its capacity expansion plans. |

| G | Related party & transaction | 2 | Revenue generated from related-party transactions (mainly for AVC and SZFSD) was 0-16% of total revenue during 2022-25, and we found no suspicious activity. |

| E | Supply chain management | 1 | Fositek maintains smooth communication channels with its suppliers and executes its business operations effectively. In response to ESG issues, Fositek actively implements supply chain management, striving to optimise the overall environment through product design, raw-material procurement, manufacturing, transportation, packaging and recycling processes. It integrates upstream and downstream suppliers to establish a green supply chain. For example, Fositek has required its suppliers to sign environmental protection agreements since 2021, committing to comply with hazardous substance control regulations. |

| G | Data security | 2 | To protect company information and customer data, Fositek has passed the IEC/ISO 27001 information security management system certification and will continue to enhance execution in various management areas. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 7 May 2026

Source: Daiwa, Company

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260601_6805_富世達_daiwa_Fositek_002.png |

36960 bytes | 真資料圖 | 堆疊長條圖,橫軸2021-2028E,依產品別Foldable phone/NB/Server/Others分類,顯示各年營收占比(如2024年Foldable phone佔83%,2028E降至25%、Server升至72%) |