PDF 原檔:260601_6285_起碁_gs_WNC_original.pdf

原始內容

WNC (6285.TW): Mgmt. visit: 800G switches, Optical switches, AI-RAN to ride on growing AI infrastructure; Buy

We hosted WNC management on June 1 in Taipei during the Taiwan Corporate Day. Management remains positive on its growth outlook driven by both technology and product expansion. We are positive on WNC due to (1) LEO satellite user terminal riding on the growing satellite communications industry, (2) ongoing wireless speci fi cation upgrades toward WiFi 7 and 8, and (3) AI infrastructure to drive growth ahead: 800G switches, Optical switches, AI-RAN, to drive the networking speed, networking coverage and enhance power consumption in AI infrastructure. Maintain Buy.

Key takeaways

- Product expansion continues: Management highlights their continuous R&D investments and product line expansion, from wireless to wireline and computing technology. On wireless, the company already showcased a WiFi 8 solution at CES 2026; on wireline, multiple products are in expansion (e.g., xPON / Wi-Fi gateways, etc.); on computing, automotive or IoT computing modules are one of the key focus areas. The company is also expanding from devices to edge equipment, such as AI-RAN (optimizing base stations, easing networking burdens), Ethernet & Optical switches, PQC cards or modules, etc. The company maintains a strong R&D commitment, and enjoys 2,716 patents as of April 2026.

- Growth outlook: Management remains positive on 2026: (1) revenue growth at low double digits, (2) the GM to be higher than the 2025 level (12.5%); WNC's 1Q26 GM came in at 13.8%, re fl ecting its strong product mix and revenue growth along with solid raw material cost management as the company mainly serves leading brand customers, (3) the Opex ratio to be lower than the 2025 level (9.1%). The key drivers include: LEO satellite broadband user terminals, 5G FWA CPE, WiFi 7 enterprise APs, 5G all-in-one small cells, 800G switches, etc. The company's 800G switches aim for enterprises, and its liquid crystal optical switches could have potential for CSP customers, supporting the company's long-term growth.

Price Target Risks and Methodology: WNC

Valuation: We use a near-term P/E to derive our 12m target price for WNC, consistent with our Taiwan Technology coverage. We base our TP of NT$364.0 on a target P/E multiple of 28.0x on a forward year EPS (2027E). Our target P/E is derived from the correlation between P/E and EPS growth of its peers. We are Buy rated on WNC. Key downside risks: fi ercer-than-expected competition in satellite

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research

Allen Chang +852-2978-2930 |

allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng +852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

communication, slower-than-expected Wi-Fi 7 or 5G FWA ramp-up in US and Europe markets.

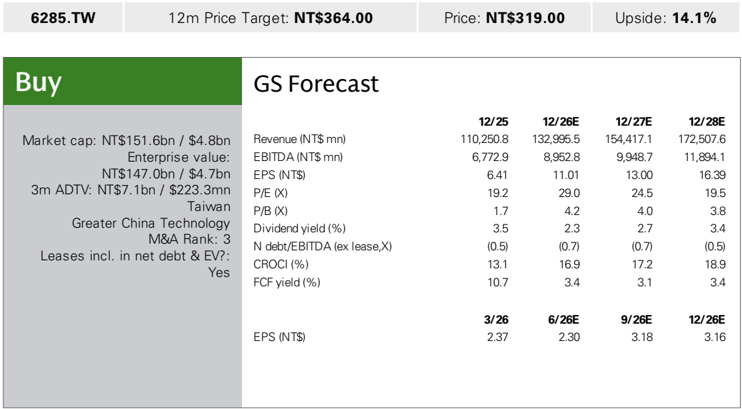

| 6285.TW | 12m Price Target: NT$364.00 | 12m Price Target: NT$364.00 | Price: NT$319.00 | Price: NT$319.00 | Upside: 14.1% | Upside: 14.1% |

|---|---|---|---|---|---|---|

| Buy | Buy | GS Forecast | GS Forecast | GS Forecast | GS Forecast | GS Forecast |

| Market c ap: NT$151.6b n / $ 4 . 8 b n En terpr is e v a lu e: NT$1 47 . 0 b n / $ 4 . 7 b n 3m AD T V : NT$ 7 .1b n / $ 223 . 3mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 EV? : | Market c ap: NT$151.6b n / $ 4 . 8 b n En terpr is e v a lu e: NT$1 47 . 0 b n / $ 4 . 7 b n 3m AD T V : NT$ 7 .1b n / $ 223 . 3mn Ta iw a n G reater Chin a Te chnology M &A R a n k: 3 EV? : | Revenue (NT$ mn) EBITDA (NT$ mn) EPS (NT$) P/E (X) P/B (X) Dividend yield (%) | 1 2 / 25 110,250.8 6,772.9 6.41 19.2 1.7 3.5 | 1 2 / 2 6E 132,995.5 8,952.8 11.01 29.0 4.2 2.3 (0.7) 16.9 | 1 2 / 2 7E 154,417.1 9,948.7 | 1 2 / 2 8E 172,507.6 |

| L ea s e s incl . in n et d ebt & | L ea s e s incl . in n et d ebt & | 11,894.1 | ||||

| 13.00 | 16.39 | |||||

| 24.5 | 19.5 | |||||

| 4.0 | 3.8 | |||||

| 2.7 | 3.4 | |||||

| N debt/EBITDA (ex lease,X) | (0.5) | (0.7) | (0.5) | |||

| Y e s | Y e s | CROCI (%) | 13.1 | 17.2 | 18.9 | |

| FCF yield (%) | 10.7 | 3.4 | 3.1 | 3.4 | ||

| 3/ 2 6 | 6/ 2 6E | 9/ 2 6E | 1 2 / 2 6E | |||

| EPS (NT$) | 2.37 | 2.30 | 3.18 | 3.16 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 29 May 2026 close.

e92c7a75ab8b4efbba794e6b187208c8

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260601_6285_起碁_gs_WNC_001.png |

89KB | 真資料圖 | 報告封面資訊卡,左上 6285.TW,12m Price Target NT$364.00,Price NT$319.00,Upside 14.1%,左側綠色 Buy 評等方塊,右側 GS Forecast 財務數字表(Revenue/EBITDA/EPS/P-E/P-B/Dividend yield/Net debt-EBITDA/CROCI/FCF yield,12/25 至 12/28E)及 EPS 季度預估表(3/26–12/26E) |