PDF 原檔:報告_MS_智邦_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的,不照 trimmed 引用順序猜。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_ms_accton_001.png |

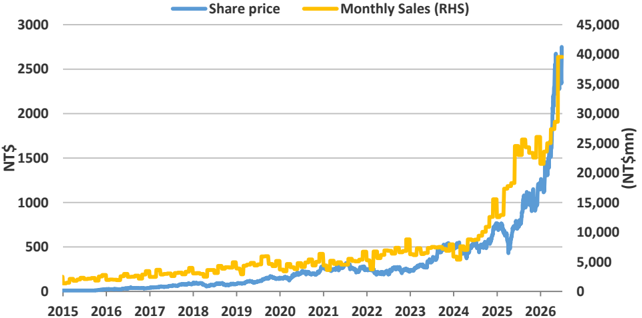

55KB | 真資料圖 | 智邦月營收(NT$mn, RHS 橘線)與股價(NT$, LHS 藍線)2015-2026 走勢圖,2026 年 6 月月營收衝至約 NT$40,000mn 創歷史新高 |

260706_ms_accton_002.png |

67KB | 裝飾·logo·banner | "Asia Summer School 2026" 水池 banner 圖,非資料圖 |

260706_ms_accton_003.png |

68KB | 真資料圖 | MS 智邦評等與目標價歷史折線圖(2023-2026),目標價沿革標示從 285 升至 3,800,評等含 E/I(Overweight)節點 |

原始內容

M July 6, 2026 02:15 PM GMT

Accton Technology Corporation | Asia Pacific

June Sales Rose 38% MoM, 61% YoY

In this report, we focus on Accton's monthly sales, which we believe could be a catalyst for share price movement.

Details:

- June sales were NT$39,555mn (+38% MoM/+61% YoY).

- 2Q26 revenue was NT$95,538mn (+36% QoQ/+58% YoY), exceeding MSe of NT$90,292mn (+29% QoQ/+49% YoY) by 6% and the consensus of NT $85,619mn (+22% QoQ/+41% YoY) by 12%.

Our view:

- We believe the strong monthly sales reflected some postponed shipments from last month and incremental contributions from both the new AI accelerator modules and 800G network switches.

- Looking ahead, we expect the momentum to remain elevated in 2H26, as the new AI accelerator model should enter the mass production stage and the network switch business will likely benefit from 800G migration.

- We expect sentiment toward Accton to improve in the coming months, as revenue should continue to grow on a sequential basis in 3Q26 and 4Q26.

- We remain OW with a PT of NT$3,800 (33x 2027 P/E, implying a PEG of 0.7).

Exhibit 1 : Accton's monthly sales vs. its share price since 2015

Past performance is no guarantee of future results. Results shown do not include transaction costs. Source: Company data, TEJ, Morgan Stanley Research.

Update

| Morgan Stanley Taiwan Limited+ Derrick Yang Equity Analyst Derrick.Yang@morganstanley.com | +886 2 2730-2862 |

|---|---|

| Vivi Huang Research Associate Vivi.Huang@morganstanley.com | +886 2 2730-2860 |

| Morgan Stanley Asia Limited+ Andy Meng, CFA Equity Analyst Andy.Meng@morganstanley.com | +852 2239-7689 |

Accton Technology Corporation (2345.TW, 2345 TT)

Top Pick

Greater China Technology Hardware | Taiwan

| Stock Rating | Overweight |

|---|---|

| Industry View | In-Line |

| Price target | NT$3,800.00 |

| Up/downside to price target (%) | 44 |

| Shr price, close (Jul 6, 2026) | NT$2,645.00 |

| 52-Week Range | NT$2,825.00-727.00 |

| Sh out, dil, curr (mn) | 559 |

| Mkt cap, curr (mn) | NT$1,478,312 |

| EV, curr (mn) | NT$1,417,660 |

| Avg daily trading value (mn) | NT$7,363 |

| Fiscal Year Ending | 12/25 | 12/26e | 12/27e | 12/28e |

|---|---|---|---|---|

| EPS (NT$)** | 47.13 | 85.77 | 115.77 | 145.77 |

| EPS (NT$)§ | 45.42 | 77.04 | 111.71 | 156.46 |

| Revenue, net (NT$ mn) | 248,320 | 396,284 | 507,015 | 619,002 |

| EBITDA (NT$ mn) | 33,894 | 63,604 | 85,643 | 106,946 |

| ModelWare net inc (NT | 26,342 | 47,937 | 64,707 | 81,469 |

| $ mn) | ||||

| P/E | 25.1 | 30.8 | 22.8 | 18.1 |

| P/BV | 11.5 | 15.7 | 10.3 | 7.2 |

| RNOA (%) | 622.3(1,508.8) | 4,169.4 | 1,577.1 | |

| ROE (%) | 72.6 | 83.2 | 68.6 | 56.6 |

| EV/EBITDA | 17.8 | 21.8 | 15.6 | 12.0 |

| Div yld (%) | 0.9 | 0.8 | 1.0 | 1.3 |

| FCF yld ratio (%)** | 4.5 | 2.9 | 4.1 | 5.3 |

| Leverage (EOP) (%) | (101.7) | (96.3) | (95.1) | (94.8) |

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

** = Based on consensus methodology

§ = Consensus data is provided by Refinitiv Estimates

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.