PDF 原檔:報告_GS_川湖2059_20260709_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_GS_川湖2059_20260709_001.png |

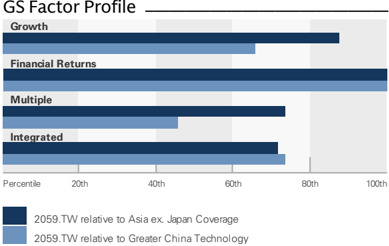

21.9KB | 真資料圖 | GS Factor Profile 橫條圖(Growth/Financial Returns/Multiple/Integrated,相對 Asia ex. Japan 與 Greater China Technology 覆蓋範圍百分位) |

報告_GS_川湖2059_20260709_002.png |

27.4KB | 真資料圖 | 2059.TW 股價 vs 台灣加權指數雙軸線圖(Oct-25 至 Jul-26) |

報告_GS_川湖2059_20260709_003.png |

48.1KB | 真資料圖 | King Slide vs Repon 月營收 YoY 比較線圖(Jan-17 至 2026) |

報告_GS_川湖2059_20260709_004.png |

47.2KB | 真資料圖 | 川湖月營收長條圖疊 YoY 折線圖(Jan-17 至 2026,近期急升至約 NT$4,443m、YoY 221%) |

報告_GS_川湖2059_20260709_005.png |

41.9KB | 真資料圖 | Exhibit 7:川湖 12 個月遠期 PEG 線圖(Oct-19 至 Jun-26,最新升至約 1.05x,遠高於 -1stv/avg/+1stv 區間) |

報告_GS_川湖2059_20260709_006.png |

35.4KB | 真資料圖 | 川湖 QFII(境外機構投資人)持股比例線圖(Jan-08 至 Jan-26,區間 0-35%,最新約 24%) |

報告_GS_川湖2059_20260709_007.png |

51.7KB | 真資料圖 | Exhibit 8:川湖 12 個月遠期 P/E 線圖(Jan-19 至 2026,區間標示 -1stv 12.2x/avg 17.2x/+1stv 22.2x,近期升破上緣至約 27x) |

報告_GS_川湖2059_20260709_008.png |

27.8KB | 真資料圖 | Exhibit 10:川湖淨利長條圖疊 OPM 折線圖 2024-2028E(淨利 2024 約 6,156mn → 2028E 約 44,644mn;OPM 由約 60% 升至逾 70%) |

報告_GS_川湖2059_20260709_009.png |

79.5KB | 真資料圖 | GS 對 2059.TW 評等與目標價沿革圖(股價/指數雙軸,2023-2026),標註歷次目標價(1405→...→4386),惟圖中資料標註至 2026-03-31,早於本次報告新訂 TP NT$12,000 |

原始內容

For the exclusive use of KEVINLU@LENOVO.COM

King Slide (2059.TW)

June revenues strong beat; Global leader riding on AI capex upcycle; Buy with raised NT$12,000 TP

2059.TW

12m Pri c e Target:

NT$12,000.00

Pri

c

e:

NT$8,095.00

Upside:

48.2%

King Slide's Jun revenue was up 221% YoY / 17% MoM, leading the company's 2Q26 revenue 60% / 41% higher than our estimate / Bloomberg consensus. The strong revenue growth in Jun rea ffi rms our positive view on King Slide's leading market position, AI servers ramp up with speci fi cation upgrade and rising non-computing IT racks in AI data center to support AI workloads (e.g. storage servers, CPU servers, LPU rack, power rack, cooling rack, networking rack, CPO switch rack, etc.), enlarging rail kits addressable market. We raise our 12m TP to NT$12,000 (from NT$7,664 previously) with higher net income in 39% / 36% / 48% in 2026E-28E and target P/E multiple from 30x to 34.5x on the stronger earnings growth in forward years. Maintain Buy.

June strong beat: Jun revenue implies 2Q26 revenues are up 99% QoQ, and we expect 3Q26 revenues to stay high at 4% QoQ, driven by the shipments ramp up of rail kits for new rack-level AI server. Our estimate assumes +157% YoY growth for 3Q26 revenue, re fl ecting our positive view on King Slide bene fi ting from the growing AI infrastructure trend, dollar content increase, and its capacity expansion. We continue to expect normalizing market share of King Slide given the high base; however, amid the fast technology migration and AI servers expanding shipments, we expect King Slide to remain in the market leading position through 2028E at least.

BUY

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu

+852-2978-0996 | yifan.hu@gs.com Goldman Sachs (Asia) L.L.C.

Key Data _____________________________________

Market cap: NT$772.3bn / $24.1bn

Enterprise value: NT$737.1bn / $23.0bn

3m ADTV: NT$3.8bn / $121.0mn

Taiwan

Greater China Technology

M&A Rank: 3

Leases incl. in net debt & EV?: Yes

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue(NT$mn) New | 17,500.7 | 39,452.2 | 56,907.1 | 74,377.3 |

| Revenue (NT$ mn) Old | 17,500.7 | 28,406.0 | 40,797.2 | 50,306.0 |

| EBITDA (NT$ mn) | 12,449.1 | 27,554.3 | 41,404.7 | 55,363.4 |

| EPS(NT$) New | 103.23 | 236.01 | 348.33 | 468.47 |

| EPS (NT$) Old | 103.23 | 170.21 | 255.75 | 316.88 |

| P/E (X) | 24.9 | 34.3 | 23.2 | 17.3 |

| P/B (X) | 8.7 | 19.6 | 13.8 | 9.9 |

| Dividend yield (%) | 2.0 | 1.5 | 2.1 | 2.9 |

| CROCI (%) | 158.3 | 290.2 | 540.3 | 963.8 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | 36.58 | 54.47 | 70.15 | 74.82 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to ed as research e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

BUY

King Slide (2059.TW)

Rating since Feb 5, 2024

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | 24.9 | 34.3 | 23.2 | 1 7 .3 |

| P/B (X) | 8. 7 | 19.6 | 13.8 | 9.9 |

| FCF yield (%) | 4.3 | 2.1 | 4.1 | 5.1 |

| EV/EBITD A R(X) | 1 7 .8 | 26. 7 | 1 7 .3 | 12.5 |

| EV/EBITD A (excl. leases) (X) | 1 7 . 7 | 26. 7 | 1 7 .3 | 12.5 |

| CROCI (%) | 158.3 | 290.2 | 540.3 | 963.8 |

| ROE (%) | 39.9 | 66.8 | 69.8 | 66.6 |

| Net debt/equity (%) | (82.4) | (88.3) | (99.4) | (99.9) |

| Net debt/equity (excl. leases) (%) | (84.2) | (89.5) | (99.4) | (99.9) |

| Interest cover (X) | 368.5 | 8 7 6.9 | 1 , 345.8 | 1 , 803. 7 |

| Days inventory outst , sales | 25.0 | 14.3 | 13.6 | 13.0 |

| Receivable days | 82.0 | 65.0 | 64.0 | 63.0 |

| Days p ayable outstandin g | 4 7 . 7 | 28.0 | 28.0 | 28.0 |

| DuPont ROE (%) | 35.1 | 5 7 .3 | 59.4 | 5 7 .1 |

| Turnover (X) | 0.5 | 0. 7 | 0.8 | 0. 7 |

| L evera g e (X) | 1.3 | 1.3 | 1.3 | 1.3 |

| G ross cas h invested (ex cas h ) (NT $ ) | 7, 624.1 | 7,7 31.4 | 4 , 415.0 | 4 , 683. 7 |

| A vera g e ca p ital e mp loyed (NT $ ) | 4 , 483.9 | 4 , 2 7 1.4 | 2 , 228.0 | 204.5 |

| BVP S (NT $ ) | 294.09 | 412.10 | 586.26 | 820.49 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | 72.8 | 125. 4 | 44 .2 | 30.7 |

| EBITDA growth | 93.6 | 121.3 | 50.3 | 33.7 |

| EPS growth | 59.8 | 128.6 | 4 7.6 | 3 4 .5 |

| DPS growth | 58.5 | 131. 4 | 4 7.6 | 3 4 .5 |

| EBIT margin | 69.1 | 68.8 | 71.9 | 73.7 |

| EBITDA margin | 71.1 | 69.8 | 72.8 | 7 4 . 4 |

| Net income margin | 56.2 | 57.0 | 58.3 | 60.0 |

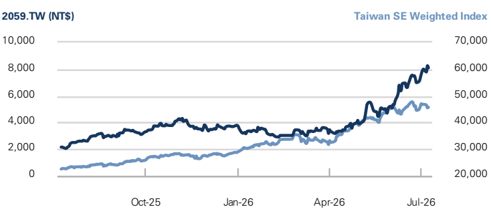

Price Performance __________________________________________

| 3m | 6m | 12m | |

|---|---|---|---|

| Absolute | 144.2% | 156.6% | 277.4% |

| Rel. to the TaiwanSE Weighted Index | 85.6% | 70.3% | 84.5% |

Source: FactSet. Price as of 8 Jul 2026 close.

Income Statement (NT$ mn) ________________________________

12/25

17,500.7

(4,191.9)

(743.1)

(476.9)

(0.3)

12

,449.

1

(360.5)

12

88

.

,0

6

692.1

--

12

1

3.

2

,4

(2,586.1)

--

--

7

.

1

--

7

3

8

9,

9,

3

8

1

.

1

03.

2

3

1

03.

1

0

1

2

3

03.

1

0

1

03.

50.94

49.3

44,

44,

12/28E

74,377.3

(16,167.9)

(2,082.6)

(1,294.2)

(0.5)

55

6

,3

3.4

(531.3)

5

8

3

2

1

4,

.

1,678.7

--

56

51

0.

8

,

(11,867.3)

--

--

6

43.

6

--

6

43.

4

6

68

.4

4

7

67

.94

4

68

7

.4

4

.94

67

233.97

49.9

22

,49

22

12/26E

39,452.2

(9,414.3)

(1,867.8)

(1,026.5)

(0.5)

27

4.3

55

,

(411.2)

27

1

43.

1

,

787.8

--

28

,43

.

1

2

(5,940.0)

--

--

1

.

2

--

,49

2

1

.

2

3

6

.0

2

3

5

1

.

2

3

75

6

.0

1

2

3

5

75

.

117.87

49.9

ls)

a

n

n

o

a

e

t

l

r

v

e

nu

To

e

Cost of goods sold

SG&A

R&D

Ot er operating inc./(exp.)

h

E

BITDA

Depreciation & amortization

E

BIT

Net interest inc./(exp.)

Income/(loss) from associates

Pre-tax pro

t

fi

Provision for taxes

Minority interest

Preferred dividends

N

et ept

c

pre-ex

(

.

inc

i

Post-tax exceptionals

N

et inc

.

(

po

s

t-ex

c

ept

E

P

E

E

S

P

P

(b

a

S

S

sic

(dilu

i

o

, pre-ex ept

c

te

(b

a

ls)

a

)

(N

, pre-ex

d

sic

c

, po

E

ept

c

$)

T

)

ept

s

t-ex te

(N

)

t-ex

P

S

(dilu

d

, po

s

DPS (NT$)

Div. payout ratio (%)

12/27E

56,907.1

(12,859.1)

(1,991.7)

(1,143.8)

(0.5)

4

1

7

,404.

(492.9)

40,9

8

.

11

1,106.5

--

4

.3

2

,0

18

(8,823.8)

--

--

1

94.4

--

33,

1

94.4

34

8

.33

34

7

.94

34

8

.33

34

7

.94

173.97

49.9

Balance Sheet (NT$ mn) ____________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| C a sh& c a sh equiv a lents | 24,079.6 | 35,471.3 | 55,853.0 | 78,437.3 |

| Accounts receiv a ble | 4,687.0 | 9,364.5 | 10,592.0 | 15,083.5 |

| Inventory | 1,165.3 | 1,929.8 | 2,297.8 | 3,017.6 |

| Other current a ssets | 58.1 | 58.1 | 58.1 | 58.1 |

| Total current assets | 2 9 , 99 0.0 | 4 6,82 3 .8 | 68,800. 9 | 9 6,5 9 6.6 |

| Net PP&E | 3,881.6 | 4,657.8 | 5,022.3 | 5,387.5 |

| Net int a ngibles | 6.0 | 6.4 | 6.6 | 6.6 |

| Tot a l investments | 0.0 | 0.0 | 0.0 | 0.0 |

| Other long-term a ssets | 1,205.8 | 1,205.8 | 1,205.8 | 1,205.8 |

| Total assets | 3 5,08 3 . 4 | 52,6 93 .8 | 75,0 3 5.6 | 10 3 ,1 9 6.6 |

| Accounts p a y a ble | 654.4 | 789.9 | 1,183.0 | 1,297.6 |

| Short-term debt | 99.1 | 70.0 | 70.0 | 70.0 |

| Short-term le a se li a bilities | 26.4 | 24.7 | -- | -- |

| Other current li a bilities | 4,587.0 | 10,974.1 | 16,350.5 | 22,075.1 |

| Total current liabilities | 5, 3 66. 9 | 11,858.8 | 17,60 3 .5 | 2 3 , 44 2.6 |

| Long-term debt | 377.2 | 250.0 | 250.0 | 250.0 |

| Long-term le a se li a bilities | 495.2 | 464.1 | -- | -- |

| Other long-term li a bilities | 818.2 | 849.3 | 1,313.4 | 1,313.4 |

| Total long-term liabilities | 1,6 9 0.5 | 1,56 3 . 4 | 1,56 3 . 4 | 1,56 3 . 4 |

| Total liabilities | 7,057.5 | 1 3 , 4 22.2 | 1 9 ,166.8 | 25,006.0 |

| Preferred sh a res | -- | -- | -- | -- |

| Tot a l commonequity | 28,026.0 | 39,271.6 | 55,868.8 | 78,190.6 |

| Minority interest | -- | -- | -- | -- |

| Total liabilities &equity | 3 5,08 3 . 4 | 52,6 93 .8 | 75,0 3 5.6 | 10 3 ,1 9 6.6 |

| Net debt, a djusted | (23,603.4) | (35,151.3) | (55,533.0) | (78,117.3) |

Cash Flow (NT$ mn) ________________________________________

12/25

9,83

7

.1

360.5

--

(1,22

.8)

7

2,364.0

11

7

,333.

(92

.9)

7

--

--

1.1

(9

8

26

)

.

--

(3,068.6)

(265.0)

(482.0)

(3,

.

6

)

815

6

,

5

9

1

.3

10,405.

7

(

1

12/26E

22,491.2

411.2

--

(5,306.6)

(0.2)

17

9

5

6

,

5

.

(1,183.6)

--

--

(4.0)

,

187

)

.

6

--

(4,860.2)

(156.2)

0.0

(

16

,0

5

.4)

11

,39

1

.

7

2

11

(

12/27E

33,194.4

492.9

--

(1,202.4)

--

3

2

8

4.9

,4

(853.6)

--

--

(4.0)

857

6

.

)

--

(11,245.6)

--

0.0

4

,

5

.

6

)

2

0,3

81

.

7

12/28E

44,643.6

531.3

--

(5,096.8)

--

40,0

78

.

1

(892.5)

--

--

(4.0)

(

8

(16,59

9

6

.

5

)

--

7

.2)

--

0.0

(

16

,

5

9

7

.

2

)

22

,

58

4.3

16,412.1

31,631.3

39,185.5

Source: Company data, Goldman Sachs Research estimates.

T

(N

c

$)

T

$)

ept

)

(N

T

$)

Net income

D&A add-back

Minority interest add-back

Net (inc)/dec working capital

Other operating cash flow

Cash flow fro

m

operations

Capital expenditures

Acquisitions

Divestitures

Others

Cash flow fro

m

investing

Repayment of lease liabilities

Dividends paid (common & pref)

Inc/(dec) in debt

Other financing cash flows

Cash flow fro financing

m

Total cash flow

Free cash flow

(

33, e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

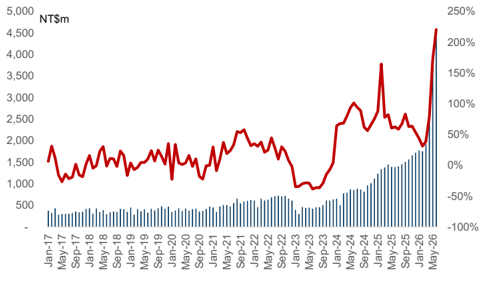

Exhibit 1: We expect King Slide Jul / Aug revenues to grow 156%/ 152% YoY King Slide monthly / quarterly revenues

| Apr-26 | May-26 | Jun-26 | Jul-26 (E) | Aug-26 (E) | Sep-26 (E) | 1Q26 | 2Q26 | 3Q26E | |

|---|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 2,596 | 3,791 | 4,443 | 3,598 | 3,670 | 3,980 | 5,450 | 10,830 | 11,249 |

| Rev YoY | 79% | 172% | 221% | 156% | 152% | 164% | 38% | 156% | 157% |

| RevMoM/QoQ | 35% | 46% | 17% | -19% | 2% | 8% | 10% | 99% | 4% |

| GS estimates | 2,245 | 2336 | 1,842 | 5,056 | 6,774 | ||||

| Act. Vs. GS | 16% | 62% | 141% | 8% | 60% |

Source: Company data, Goldman Sachs Global Investment Research

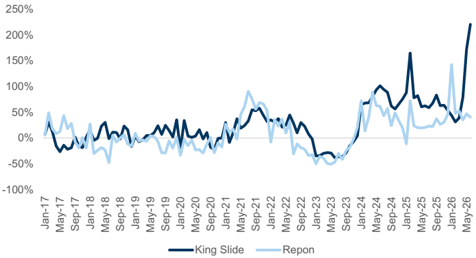

Exhibit 2: Monthly revenues YoY: King Slide vs. Repon

Source: Company data

Exhibit 3: King Slide monthly revenues and YoY trend

Source: Company data

Earnings revision: We revise up our 2026E-28E net incomes by 39% / 36% / 48%, mainly on higher revenues and GMs. Our 2026E-28E revenues are raised by 39% / 39% / 48%, mainly on (1) factoring in Global Server TAM update, where AI servers implied AI chips was raised by 14% / 22% / 14% in 2026E-28E, (2) rising non-computing IT racks in AI data center to support AI workloads (e.g. storage servers, CPU servers, LPU rack, power rack, cooling rack, networking rack, CPO switch rack, etc.), enlarging rail kits addressable market, and (3) lifted King Slide market share considering its strong revenues growth, outperforming peers, and the fast technology migration and AI infrastructure upcycle to support healthier competition. Our GM revisions are mainly on product mix upgrade, with growing AI rail kits carrying a higher GM compared to non-AI rail kits (general server rail kit, kitchen rail kit). We raise our opex ratio estimates mainly on higher R&D to support the rail kits speci fi cation upgrades and expanding SKUs for various rack products.

Exhibit 4: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT$m | Old | New | Diff% | Old | New | Diff% | Old | New | Diff% |

| Revenues | 28,406 | 39,452 | 39% | 40,797 | 56,907 | 39% | 50,306 | 74,377 | 48% |

| GP | 21,698 | 30,038 | 38% | 31,054 | 44,048 | 42% | 38,701 | 58,209 | 50% |

| OP | 18,663 | 27,143 | 45% | 29,246 | 40,912 | 40% | 36,472 | 54,832 | 50% |

| Net income | 16,220 | 22,491 | 39% | 24,373 | 33,194 | 36% | 30,198 | 44,644 | 48% |

| Margins | |||||||||

| GM | 76.4% | 76.1% | 76.1% | 77.4% | 76.9% | 78.3% | |||

| OPM | 65.7% | 68.8% | 71.7% | 71.9% | 72.5% | 73.7% | |||

| NM | 57.1% | 57.0% | 59.7% | 58.3% | 60.0% | 60.0% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 5: Rev and GM change by product

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025E |

|---|---|---|---|---|---|---|---|

| Revenues (NT$m) | 2026E | 2027E | 2028E | GM | 2026E | 2027E | 2028E |

| NEW | 39,452 | 56,907 | 74,377 | NEW | 76.1% | 77.4% | 78.3% |

| AI servers rail kit | 16,037 | 27,483 | 42,474 | AI servers rail kit | 86.3% | 85.7% | 85.0% |

| General server rail kit | 8,237 | 9,841 | 11,480 | General server rail kit | 66.4% | 66.3% | 66.2% |

| Rail kits for other IT | 12,693 | 16,942 | 17,544 | Rail kits for other IT | 75.0% | 75.0% | 75.0% |

| Non-servers rail kit | 2,173 | 2,330 | 2,568 | Non-servers rail kit | 49.5% | 48.4% | 47.4% |

| Others | 311 | 311 | 311 | Others | 41.1% | 41.1% | 41.1% |

| OLD | 28,406 | 40,797 | 50,306 | OLD | 76.4% | 76.1% | 76.9% |

| AI servers rail kit | 18,007 | 26,268 | 34,563 | AI servers rail kit | 86.3% | 85.5% | 85.2% |

| General server rail kit Rail kits for other IT | 7,538 | 11,121 | 11,677 | General server rail kit Rail kits for other IT | 64.0% | 63.0% | 63.0% |

| Non-servers rail kit | 2,548 | 3,083 | 3,730 | Non-servers rail kit | 47.3% | 47.3% | 47.3% |

| Others | 313 | 325 | 336 | Others | 40.7% | 39.9% | 39.3% |

| CHG | 39% | 39% | 48% | CHG (New - Old) | -0.2% | 1.3% | 1.3% |

| AI servers rail kit | -11% | 5% | 23% | AI servers rail kit | 0.1% | 0.2% | -0.2% |

| General server rail kit Rail kits for other IT | 9% | -12% | -2% | General server rail kit Rail kits for other IT | 2.4% | 3.3% | 3.2% |

| Non-servers rail kit | -15% | -24% | -31% | Non-servers rail kit | 2.2% | 1.1% | 0.1% |

| Others | -1% | -4% | -7% | Others | 0.4% | 1.1% | 1.8% |

Source: Company data, Goldman Sachs Global Investment Research

GSe vs. Bloomberg consensus: Our 2026E-27E net income is 33% / 55% higher than the BBG consensus, mainly on higher revenues and lower opex ratios. Our higher revenues re fl ects the strong 2Q26 revenues beat, which rea ffi rms our positive view on King Slide's leading market position in AI server rail kits, and the growing IT racks in AI data centers enlarging rail kits addressable market, bene fi ting King Slide's growth ahead. Our lower opex ratio is mainly on larger revenues scale, driving better operation e ffi ciency.

Exhibit 6: GS vs. Bloomberg consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | |

|---|---|---|---|---|---|---|

| NT$m | GS | Cons. | Diff% | GS | Cons. | Diff% |

| Revenues | 39,452 | 29,385 | 34% | 56,907 | 38,266 | 49% |

| GP | 30,038 | 22,715 | 32% | 44,048 | 29,478 | 49% |

| OP | 27,143 | 19,980 | 36% | 40,912 | 26,113 | 57% |

| Net income | 22,491 | 16,939 | 33% | 33,194 | 21,460 | 55% |

| Margins | ||||||

| GM | 76.1% | 77.3% | 77.4% | 77.0% | ||

| OPM | 68.8% | 68.0% | 71.9% | 68.2% | ||

| NM | 57.0% | 57.6% | 58.3% | 56.1% |

Source: Goldman Sachs Global Investment Research, Bloomberg

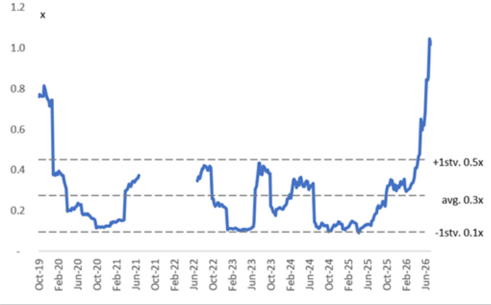

Valuation: We continue to use a near-term P/E to derive our target price. We continue to derive the target P/E multiple via a correlation of the high-end of the company's historical PEG at 1.0x (vs. 0.8x previously), and with 2028E net income growth at 34% YoY. With this, our new target P/E multiple is now at 34.5x on our 2027E EPS (vs. previously at 30.0x). With the updated target P/E and earnings estimate, our 12M TP is revised up to NT$12,000 (vs. previously at NT$7,664). Our new TP implied PEG&M is at 0.3x, which is within peers' range from 0.2x to 0.5x. Maintain Buy.

e92c7a75ab8b4efbba794e6b187208c8

1.2

Company

King Slide

1.0

King Slide (TP implied)

Peers

0.8

Repon

Karrie

0.6

AVC

Auras

Fositek

0.4

VPEC

Landmark

0.2

Avg.

For the exclusive use of KEVINLU@LENOVO.COM

Ticker

Rating

Buy

- TW

Buy

35

2027 PE 2028 NI YOY

23

34

27

8

34%

30

34%

25

Exhibit 7: King Slide 12M forward PEG

66%

20

21%

May-19

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 9: King Slide QFII

Source: TEJ

Sep-19

202B OPM

74%

74%

Ratio

0.2

0.3

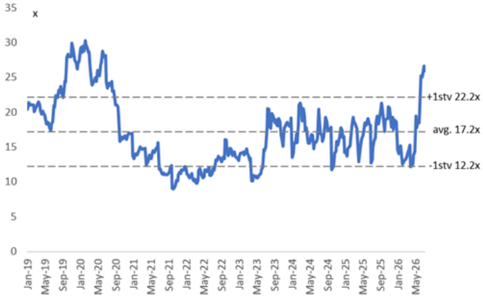

Exhibit 8: King Slide 12M forward P/E ratio

Jan-20

Source: Company data, Goldman Sachs Global Investment Research

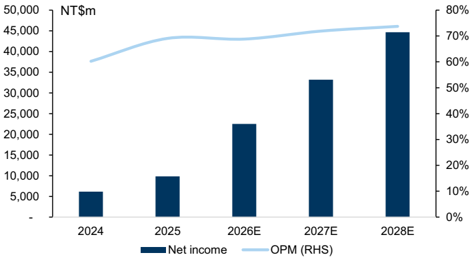

Exhibit 10: King Slide's net income and OPM trend

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 11: King Slide and peers' PEG&M

NC = not covered.

Source: Company data, Goldman Sachs Global Investment Research, Re fi nitiv Eikon

e92c7a75ab8b4efbba794e6b187208c8

NTS m

Revenue

Gross profit

Opex

OP income

2024 2025 2026E 2027E 2028E

7,002

39,452

56,907

(898)

30,038

(2,894)

6,101

Net income

44,048

(3,136)

40,912

Exhibit 12: King Slide P&L Summary

EPS (diluted, NT:

Margins

Gross margin

Operating margi

Net margin

Ratios

Opex ratio

Tax rate

YoY

Revenue

Gross profit

OP income

Net income

QoQ

Revenue

Gross profit

OP income

Net income

For the exclusive use of KEVINLU@LENOVO.COM

28.32

1025 2025 3025 4025 1026 2026E 3026E 4026E

3,954

3,007

(285)

2,723

2,511

26.32

4,229

3,277

(245)

2,966

614

6.44

4,369

3,258

(347)

2,975

3,197

33.52

| 16847 | 156 52 1646 | 116912331 | 116025 | 14588 | ||

|---|---|---|---|---|---|---|

| 1555 | 1388 445 | |||||

| 13438834 | ||||||

| 13% | 4% | |||||

| 4% | ||||||

| 16% 15% | 4% | |||||

| 10% |

Source: Company data, Goldman Sachs Global Investment Research

331213

308131

606011

2023

3,532

e92c7a75ab8b4efbba794e6b187208c8

Samble 19. his Shue s balance Sheet

NT$ m

Cash and equivalents

Net receivables

Inventory

Other current assets

Current assets

Net PP&E/Fixed assets

Net intangibles

Other long-term assets

Long-term assets

Total assets

Accounts payable

Short-term debt

Other current liabilities

Current liabilities

Long-term debt

Other long-term liabilities

Long term liabilities

Total liabilities

Common stock

Treasury stock

Retained earnings

Other common equity

Total common equity

Minority interest

For the exclusive use of KEVINLU@LENOVO.COM

2023

12,603

1,656

2024

17,488

2025

2026E

2027E

24,080

35,471

4,687

9,364

55,853

10,592

Exhibit 13: King Slide's balance sheet

16,202

3,192

1,184

4,379

20,581

309

126

1,740

2,174

741

1,229

1,970

4,145

1,750

-

14,694

(8)

16,436

-

16,436

172.14

112

158

56

214

(11,736)

-71%

123.15

0.29

1.24

47%

17%

14%

2,298

58

2028E

78,437

15,083

3,018

58

| 29,990 | 46,824 68,801 | 96,597 |

|---|---|---|

| 21,949 3,287 | 4,658 5,022 | 5,388 |

| 3 2 3,882 6 | 6 7 | 7 |

| 1,234 1,206 | 1,206 1,206 | 1,206 |

| 5,870 6,235 | 6,600 | |

| 4,524 26,472 5,093 35,083 | 75,036 | |

| 441 654 | 52,694 790 1,183 | 103,197 1,298 |

| 127 99 | 70 70 | 70 |

| 2,581 | 10,999 16,350 | |

| 3,149 4,513 5,367 | 11,859 17,603 | 22,075 23,443 |

| 615 377 | 250 250 | 250 |

| 1,416 1,313 | 1,313 1,313 | 1,313 |

| 2,031 1,691 | 1,563 1,563 | 1,563 |

| 5,180 7,057 | 13,422 19,167 | 25,006 |

| 1,750 1,750 | 1,750 1,750 | |

| 1,750 | ||

| 19,499 | 37,509 54,106 | |

| 43 26,264 13 | 13 13 | 76,428 13 |

| 21,292 28,026 | 39,272 55,869 | 78,191 |

| 21,292 28,026 | 39,272 55,869 | 78,191 |

| 223.02 | 411.63 585.60 | |

| 293.74 | 819.57 | |

| 87 82 | 64 | |

| 131 104 | 65 60 60 | 63 60 |

| 44 48 | 28 28 | 28 |

| 174 139 | 97 96 | 95 |

| (16,747) (23,603) | (35,151) (55,533) | (78,117) |

| -79% -84% | -90% -99% | -100% |

| 175.74 247.68 | 368.86 582.74 | 819.73 |

| 0.43 0.57 | 0.90 0.89 | |

| 1.30 | 0.83 1.33 | |

| 61% 56% | 57% 58% | 60% |

| 33% 40% | 67% 70% | 67% |

| 26% 32% | 51% 52% | 50% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

camble 19n15 clues last now statement

NT$ m

Net income

Minority interest add-back

Depreciation and amortization add-back

Net loss/(gain) on asset sales

(Increase)/decrease in working capital

Other operating cash flow items

Cash flow from operating

Capital expenditure

Other investment cash flow items

Cash flow from investing

Dividends paid

Change in common stock

Increase/(decrease) in short-term debt

Increase/(decrease) in long-term debt

Other financing cash flow items

Cash flow from financing

Others

Net change in cash

Ratio

Capex to revenues

For the exclusive use of KEVINLU@LENOVO.COM

2023

2,704

269

2024

6,156

-

328

2026E

22,491

-

360

411

2027E

33,194

493

Exhibit 14: King Slide's cash fl ow statement

52

2028E

44,644

-

531

-

(5,097)

| 253 314 5,187 2,365 11,334 17,596 | 32,485 | 40,078 |

|---|---|---|

| 3,278 | (893) | |

| (378) (355) (928) (1,184) | (854) | |

| 217 885 1 (4) (1,188) | (4) | (4) |

| (161) 530 (927) | (858) | (897) |

| (1,906) (1,352) (3,069) (4,860) | (11,246) | (16,597) |

| - | - | |

| 126 1 (27) (238) (29) | ||

| (153) (127) (127) | - | |

| (33) (30) (30) (3,363) - (5,016) | ||

| (1,966) (1,508) 676 | (11,246) | (16,597) |

| (141) (452) - | 20,382 | 22,584 |

| 1,010 4,886 6,591 11,392 | ||

| 7% 4% 3% | ||

| 5% | 2% | 1% |

(1,611)

(1,228)

(5,307)

(1,202)

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - King Slide

Valuation methodology : Our 12m target price for King Slide is based on a near-term P/E, consistent with our Taiwan Technology coverage. Our 12m TP of NT$12,000 is based on a target P/E multiple of 34.5x on our forward year EPS (2027E). Our target P/E is derived from the company's peak PEG at 1.0x and with 2028E net income growth at 34% YoY, as we expect the migration to AI server rail kits to drive the company's pro fi tability.

Downside risks: (1) New entrants intensifying competition, (2) slower-than-expected AI server growth, (3) lower-than-expected general server shipment growth.

2025

9,837

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM