PDF 原檔:報告_GS_勤誠_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_gs_chenbro-DG_001.png |

32KB | — | <40KB,未 Read(預設 logo) |

260706_gs_chenbro-DG_002.png |

21KB | — | <40KB,未 Read(預設 logo) |

260706_gs_chenbro-DG_003.png |

28KB | — | <40KB,未 Read(預設 logo) |

260706_gs_chenbro-DG_004.png |

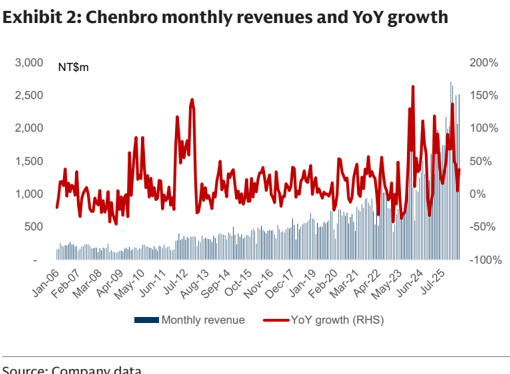

72KB | 真資料圖 | 勤誠月營收長條圖(NT$m,Jan-06 至 Jul-25)+ 右軸 YoY 成長折線(-100% 至 200%);Exhibit 2 |

260706_gs_chenbro-DG_005.png |

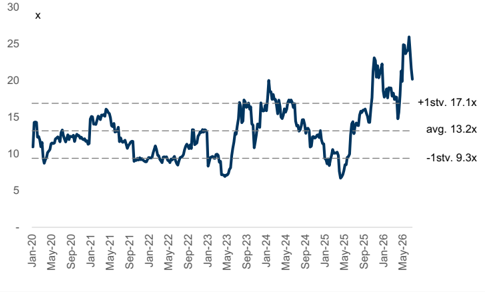

41KB | 真資料圖 | 勤誠 12M forward PE ratio 走勢(Jan-20 至 May-26);標示 avg. 13.2x、+1stv. 17.1x、-1stv. 9.3x |

260706_gs_chenbro-DG_006.png |

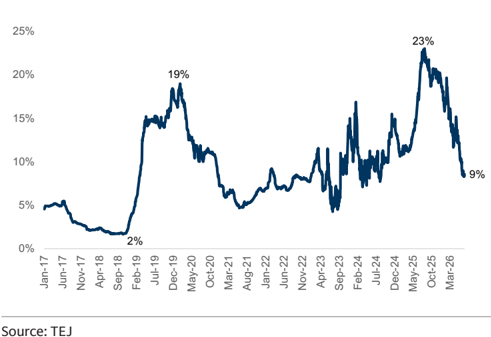

43KB | 真資料圖 | 勤誠 QFII 持股比例歷史(Jan-17 至 Mar-26);峰值 23%(May-25),Mar-26 降至 9% |

260706_gs_chenbro-DG_007.png |

75KB | 真資料圖 | 高盛勤誠(8210.TW)評等與目標價歷史(2023-2026);Aug-22 掛 Buy,目標價從 380 逐步上調至 1,162,含台灣加權指數對比 |

原始內容

For the exclusive use of KEVINLU@LENOVO.COM

Chenbro (8210.TW)

Chassis and Racks in expansion on AI infrastructure upcycle; TP up to NT$1,482, Down to Neutral on fair valuation

8 2 10.TW

12m Pri c e Target:

NT$1,48 2 .00

Pri c e:

NT$1,305.00

Upside:

13.6%

We are positive on Chenbro's leading market position in AI server chassis, riding on AI capex across US and China cloud service providers (CSPs), and expanding to full rack business (e.g. noise-cancellation racks, liquid cooling CDU racks, etc.). We raise our 12-month TP by 28% to NT$1,482 (20.2x 2027E PE), but downgrade the stock to Neutral (from Buy) on fair valuation. We could turn more positive on Chenbro in the event of faster-than-expected AI infrastructure investments, faster-than-expected rack business ramp-up, or healthier-than-expected competition. Since Chenbro was added to the Buy list on Aug 22, 2024, the share price has increased 342% vs. a 111% increase in the Taiwan SE Weighted Index; we attribute this outperformance to its large exposure to the server market with rising contribution from AI servers.

Source: Company data, Goldman Sachs Global Investment

Research

Chenbro's revenues in May increased by 22% MoM, and we expect the sequential increase continued in June, bringing 2Q26E revenue growth to +10% QoQ. Growth in 2H26 should remain strong, taking 2026E revenue growth to +61% YoY (vs. +52% YoY in 2025), and 1H:2H to 42%:58%, similar to the pattern in 2024-25. Catalysts in 2H26 include: (1) major ASIC AI servers customers' new models

NEUTRAL

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu

+852-2978-0996 | yifan.hu@gs.com Goldman Sachs (Asia) L.L.C.

Key Data _____________________________________

Market cap: NT$165.8bn / $5.2bn

Enterprise value: NT$163.4bn / $5.1bn

3m ADTV: NT$3.1bn / $97.2mn

Taiwan

Greater China Technology

M&A Rank: 3

Leases incl. in net debt & EV?: Yes

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue(NT$mn) New | 22,001.3 | 35,519.7 | 49,221.2 | 67,376.5 |

| Revenue (NT$ mn) Old | 22,004.3 | 35,058.7 | 44,200.4 | -- |

| EBITDA (NT$ mn) | 5,095.5 | 9,253.1 | 13,118.1 | 18,788.2 |

| EPS(NT$) New | 28.41 | 51.33 | 73.39 | 106.76 |

| EPS (NT$) Old | 29.32 | 52.81 | 67.19 | -- |

| P/E (X) | 18.1 | 25.4 | 17.8 | 12.2 |

| P/B (X) | 5.9 | 11.7 | 8.8 | 6.4 |

| Dividend yield (%) | 2.7 | 1.9 | 2.8 | 4.0 |

| CROCI (%) | 47.6 | 58.6 | 72.9 | 94.2 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | 10.52 | 11.18 | 13.50 | 16.13 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Chenbro (8210.TW)

Rating since Jul 6, 2026

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | 18.1 | 25.4 | 17.8 | 12.2 |

| P/B (X) | 5.9 | 11.7 | 8.8 | 6.4 |

| FCF yield (%) | 3.3 | 0.9 | 6.0 | 5.0 |

| EV/EBITD A R(X) | 11.8 | 17.3 | 11.7 | 8.0 |

| EV/EBITD A (excl. leases) (X) | 11.8 | 17.3 | 11.7 | 8.0 |

| CROCI (%) | 47.6 | 58.6 | 72.9 | 94.2 |

| ROE (%) | 39.4 | 52.0 | 56.3 | 60.7 |

| Net debt/equity (%) | (25.0) | (16.8) | (46.3) | (47.2) |

| Net debt/equity (excl. leases) (%) | (25.0) | (16.8) | (46.3) | (47.2) |

| Interest cover (X) | 58.2 | 71.7 | 101.7 | 149.8 |

| Days inventory outst, sales | 50.7 | 47.4 | 47.5 | 47.0 |

| Receivable days | 85.5 | 80.0 | 80.0 | 80.0 |

| Days payable outstandin g | 161.0 | 124.0 | 123.0 | 122.0 |

| DuPont ROE (%) | 32.1 | 45.0 | 48.2 | 51.5 |

| Turnover (X) | 0.9 | 1.2 | 1.2 | 1.4 |

| L evera g e (X) | 2.1 | 2.1 | 2.1 | 1.9 |

| G ross cas h invested (ex cas h ) (NT $ ) | 10,047.6 | 14,257.4 | 13,074.9 | 17,103.8 |

| A vera g e capital e m ployed (NT $ ) | 7,719.6 | 10,185.6 | 11,225.1 | 12,145.7 |

| BVP S (NT $ ) | 86.90 | 111.70 | 148.90 | 203.02 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | 51 . 6 | 61 . 4 | 38 . 6 | 36 . 9 |

| E BITDA growth | 82 . 7 | 81 . 6 | 41 . 8 | 43 . 2 |

| E PS growth | 83 . 5 | 80 . 7 | 43 . 0 | 45 . 5 |

| DPS growth | 92 . 8 | 80 . 7 | 43 . 0 | 45 . 5 |

| E BIT margin | 21 . 4 | 24 . 8 | 25 . 7 | 27 . 1 |

| E BITDA margin | 23 . 2 | 26 . 1 | 26 . 7 | 27 . 9 |

| Net income margin | 16 . 2 | 18 . 4 | 18 . 9 | 20 . 1 |

Price Performance __________________________________________

3m

55.2%

8.0%

6m

36.8%

12m

166.3%

(14.2)%

29.3%

Source: FactSet. Price as of 3 Jul 2026 close.

Absolute

Rel. to the Taiwan SE Weighted Index

Income Statement (NT$ mn) ________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Tota l r e v e nu e | 22,001.3 | 35,519.7 | 49,221.2 | 67,376.5 |

| Cost of goods sold | (15,407.2) | (24,381.5) | (33,887.3) | (45,935.4) |

| SG&A | (1,479.2) | (1,807.4) | (1,968.8) | (2,156.0) |

| R&D | (406.6) | (534.7) | (738.3) | (1,010.6) |

| Other operating inc./(exp.) | -- | -- | -- | -- |

| E BITDA | 5 ,09 5 . 5 | 9, 25 3. 1 | 1 3, 118 . 1 | 18 , 788 . 2 |

| Depreciation& amortization | (387.2) | (457.0) | (491.3) | (513.8) |

| E BIT | 4, 7 0 8 .3 | 8 , 7 9 6 . 1 | 12 , 626 . 8 | 18 , 27 4.4 |

| Net interest inc./(exp.) | (6.2) | (40.2) | (39.8) | (34.4) |

| Income/(loss) from associates | -- | -- | -- | -- |

| Pre-tax pro fi t | 4, 8 3 2 .0 | 8 , 7 9 1 .4 | 12 , 587 .0 | 18 , 2 40.0 |

| Provision for taxes | (1,171.4) | (2,154.4) | (3,146.7) | (4,560.0) |

| Minority interest | (102.3) | (116.2) | (116.2) | (116.2) |

| Preferred dividends | -- | -- | -- | -- |

| N et inc . ( pre-ex c ept i o n a ls) | 3, 558 .3 | 6 , 52 0.9 | 9,3 2 4. 1 | 1 3, 56 3. 8 |

| Post-tax exceptionals | -- | -- | -- | -- |

| N et inc . ( po s t-ex c ept i o n a ls) | 3, 558 .3 | 6 , 52 0.9 | 9,3 2 4. 1 | 1 3, 56 3. 8 |

| E P S(b a sic , pre-ex c ept ) (N T $) | 2 9.0 6 | 52 .3 6 | 7 4. 87 | 1 0 8 .9 1 |

| E P S(dilu te d , pre-ex c ept ) (N T $) | 28 .4 1 | 51 .33 | 7 3.39 | 1 0 6 . 76 |

| E P S(b a sic , po s t-ex c ept ) (N T $) | 2 9. 15 | 52 .3 6 | 7 4. 87 | 1 0 8 .9 1 |

| E P S(dilu te d , po s t-ex c ept ) (N T $) | 28 .4 1 | 51 .33 | 7 3.39 | 1 0 6 . 76 |

| DPS (NT$) | 14.01 | 25.31 | 36.19 | 52.64 |

| Div. payout ratio (%) | 48.2 | 48.3 | 48.3 | 48.3 |

| Balance Sheet (NT$ mn) | ______ | |||

| 12/25 | 12/26E | 12/27E | 12/28E | |

| C a sh& c a sh equiv a lents | 5 ,688.3 | 7,036. 5 | 10,9 5 3.4 | 13,430.6 |

| Accounts receiv a ble | 6, 5 6 5 .8 | 9,004. 5 | 12, 5 71.9 | 16,963.0 |

| Inventory | 3,92 5 .1 | 5 ,293.1 | 7, 5 19.1 | 9,848.3 |

| Other current a ssets | 404.0 | 404.0 | 404.0 | 404.0 |

| Total current assets | 16 , 58 3. 2 | 21 , 7 3 8 . 2 | 3 1 ,44 8 .4 | 40, 6 4 5 . 8 |

| Net PP&E | 5 , 5 90.6 | 6,8 5 1.0 | 7,184. 5 | 7, 5 18.9 |

| Net int a ngibles | 5 7.1 | 5 7.6 | 5 8.0 | 5 8.2 |

| Tot a l investments | 0.0 | 0.0 | 0.0 | 0.0 |

| Other long-term a ssets | 1,22 5 .4 | 1,22 5 .4 | 1,22 5 .4 | 1,22 5 .4 |

| Total assets | 2 3,4 56 .4 | 29 , 872 . 2 | 3 9 , 916 .3 | 4 9 ,44 8 .3 |

| Accounts p a y a ble | 8,3 5 6.0 | 8,210.0 | 14,629.1 | 16,078.4 |

| Short-term debt | 1, 5 88.8 | 1,900.0 | 1,000.0 | 5 00.0 |

| Short-term le a se li a bilities | -- | -- | -- | -- |

| Other current li a bilities | 968.7 | 2,429.4 | 3,811.6 | 5 ,902.0 |

| Total current liabilities | 1 0, 91 3. 6 | 12 , 5 3 9 . 5 | 19 ,440. 6 | 22 ,4 8 0.4 |

| Long-term debt | 1,332.0 | 2,700.0 | 1,000.0 | 5 00.0 |

| Long-term le a se li a bilities | -- | -- | -- | -- |

| Other long-term li a bilities | 134.1 | 134.1 | 134.1 | 134.1 |

| Total long-term liabilities | 1 ,4 66 . 1 | 2 , 8 34. 1 | 1 , 1 34. 1 | 6 34. 1 |

| Total liabilities | 12 ,3 79 . 6 | 15 ,3 7 3. 6 | 2 0, 57 4. 7 | 2 3, 11 4. 5 |

| Preferred sh a res | -- | -- | -- | -- |

| Tot a l commonequity | 10,884.9 | 14,190.6 | 18,917.3 | 2 5 ,793.4 |

| Minority interest | 191 . 9 | 30 8 .0 | 4 2 4. 2 | 5 40.4 |

| Total liabilities &equity | 2 3,4 56 .4 | 29 , 872 . 2 | 3 9 , 916 .3 | 4 9 ,44 8 .3 |

| Net debt, a djusted | (2,767. 5 ) | (2,436. 5 ) | (8,9 5 3.4) | (12,430.6) |

Cash Flow (NT$ mn) ________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Net income | 3,558.3 | 6 ,520.9 | 9,324.1 | 13,5 6 3.8 |

| D&Aadd-back | 387.2 | 457.0 | 491.3 | 513.8 |

| Minority interest add-back | 102.3 | 11 6 .2 | 11 6 .2 | 11 6 .2 |

| Net (inc)/dec w orking capital | (1,447.3) | (3,952.7) | 6 25. 6 | (5,270.8) |

| Other operating cash flo w | 48 6 .4 | 0.1 | -- | -- |

| Cash flow fro m operations | 3 ,0 86 .9 | 3 , 1 4 1 . 5 | 1 0, 557 . 2 | 8 ,9 23 .0 |

| Capital expenditures | (984.3) | (1,704.9) | (812.2) | (835.5) |

| Acquisitions | -- | -- | -- | -- |

| Divestitures | -- | -- | -- | -- |

| Others | 491.0 | (13.0) | (13.0) | (13.0) |

| Cash flow fro m investing | (49 3 . 3 ) | ( 1 , 718 .0) | ( 825 . 2 ) | ( 8 4 8 . 5 ) |

| Repayment of lease liabilities | -- | -- | -- | -- |

| Dividends paid(common& pref) | (907.4) | (1,754.5) | (3,215.2) | (4,597.3) |

| Inc/(dec) in debt | (745.1) | 1, 6 79.2 | (2, 6 00.0) | (1,000.0) |

| Other financing cash flo w s | 947.3 | 0.0 | 0.0 | 0.0 |

| Cash flow fro m financing | ( 7 0 5 . 2 ) | ( 75 . 2 ) | ( 5 , 815 . 2 ) | ( 5 , 5 9 7 . 3 ) |

| Total cash flow | 1 , 888 . 5 | 1 , 3 4 8 . 3 | 3 ,9 16 . 8 | 2 ,4 77 . 2 |

| Free cash flo w | 2,102. 6 | 1,43 6 .5 | 9,745.0 | 8,087.5 |

Source: Company data, Goldman Sachs Research estimates.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

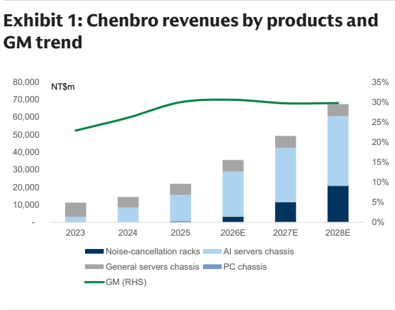

ramp up, (2) rack business expansion on noise-cancellation racks ramping up and expansion to liquid cooling CDU racks, (3) AI servers powered by NVIDIA (e.g. HGX, MGX) in expansion with new chipset platforms, and (4) new capacity in Malaysia to start in 3Q26. Other than chassis / racks for AI servers, we see more IT infrastructure in AI data center facilitating AI tasks work fl ow, such as CPU server racks, networking racks, storage racks, etc. enlarging Chenbro's addressable market in coming years. We expect Chenbro's revenues to grow at a 38% CAGR in 2026-28E with net income to grow at a 41% CAGR in 2026-28E on continuous improvements in operation e ffi ciency with increasing revenue scale, along with stable GM at 30-31% in 2026-28E.

Source: Company data

Exhibit 3: Chenbro monthly revenues preview

| Apr-26 | May-26 | Jun-26 (E) | Jul-26 (E) | Aug-26 (E) | Sep-26 (E) | 1Q26 | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 2,066 | 2,517 | 3,241 | 2,949 | 3,156 | 3,433 | 7,107 | 7,825 | 9,539 |

| YoY | 5% | 37% | 98% | 70% | 81% | 58% | 71% | 44% | 68% |

| MoM/QoQ | -18% | 22% | 29% | -9% | 7% | 9% | 5% | 10% | 22% |

| GS estimates (NT$m) | 6,782 | ||||||||

| Act. Vs. GS. | 5% |

Source: Company data, Goldman Sachs Global Investment Research

Earnings revision

We raise gross pro fi ts by 6% / 19% in 2026 / 27E mainly on higher revenues and GM, re fl ecting our positive view on Chenbro's leading market position in AI server chassis and the expanding rack business. The higher GM re fl ects the company's exposure to ASIC AI servers chassis, which enjoys higher customization level and more pure chassis delivery. Nevertheless, we raise our R&D investments to support the rack business expansion for various racks, leading to a smaller raise in OP income compared to GP income, leading to changes in net income of -1% / +11% in 2026 / 27E. We introduce 2028E estimates.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 4: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT$m | Old | New | Diff% | Old | New | Diff% | Old | New | Diff% |

| Revenues | 35,059 | 35,520 | 1% | 44,200 | 49,221 | 11% | 67,376 | ||

| GP | 10,526 | 11,138 | 6% | 12,938 | 15,334 | 19% | 21,441 | ||

| OP | 8,773 | 8,796 | 0% | 11,126 | 12,627 | 13% | 18,274 | ||

| Net income | 6,611 | 6,521 | -1% | 8,411 | 9,324 | 11% | 13,564 | ||

| EPS (diluted) | 52.8 | 51.3 | -3% | 67.2 | 73.4 | 9% | 106.8 | ||

| Margins | |||||||||

| GM | 30.0% | 31.4% | 29.3% | 31.2% | 31.8% | ||||

| OPM | 25.0% | 24.8% | 25.2% | 25.7% | 27.1% | ||||

| NM | 18.9% | 18.4% | 19.0% | 18.9% | 20.1% |

Source: Goldman Sachs Global Investment Research

Compared to Bloomberg consensus, we are 7% / 13% ahead on 2026 / 27E net income, re fl ecting our positive view on Chenbro's revenues expansion. Our GM is slightly lower than Bloomberg consensus, re fl ecting our positive view on its racks business expansion, which carries a lower GM compared to its AI servers chassis.

Exhibit 5: GS vs. Bloomberg consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | |

|---|---|---|---|---|---|---|

| NT$m | GS | Cons. | Diff% | GS | Cons. | Diff% |

| Revenues | 35,520 | 33,972 | 5% | 49,221 | 45,756 | 8% |

| GP | 11,138 | 10,793 | 3% | 15,334 | 14,237 | 8% |

| OP | 8,796 | 8,127 | 8% | 12,627 | 10,969 | 15% |

| Net income | 6,521 | 6,094 | 7% | 9,324 | 8,253 | 13% |

| Margins | ||||||

| GM | 31.4% | 31.8% | 31.2% | 31.1% | ||

| OPM | 24.8% | 23.9% | 25.7% | 24.0% | ||

| NM | 18.4% | 17.9% | 18.9% | 18.0% |

Source: Goldman Sachs Global Investment Research, Bloomberg

Valuation and upside risks

We continue to use near-term P/E to derive our 12m TP and roll over to 2027E. We derive our target PE multiple from (1) peers' avg. ratio of trading PE to forward year fundamentals (NI YoY and OPM), which is at 0.3x, and (2) Chenbro's forward year fundamentals: 2027-28E NI YoY at 44% on avg. and OPM is at 26.4% on avg. Our new target PE multiple is at 20.2x (vs. 17.6x of our previous TP implied 2027E PE). Our previous target PE multiple to forward year fundamentals was also 0.3x. Our new target PE multiple of 20.2x is between the company's avg.+1stv. PE of 17x and peak PE of 26x, re fl ecting our positive view on its expansion toward AI servers. We raise our target price by 28% to NT$1,482 (20.2x 2027E PE). With less upside compared to our Greater China Technology coverage, we downgrade Chenbro from Buy to Neutral.

Chenbro currently trades at 18x 2027E P/E, largely in line with our target PE multiple and based on peers' avg. ratio of trading PE to forward year fundamentals (NI YoY and OPM).

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 6: Chenbro peers comparison

| Company | Ticker | Rating | 2027E PE | 2027-28E NI YoY | 2027-28E OPM | Ratio |

|---|---|---|---|---|---|---|

| Chenbro | 8210.TW | Neutral | 17.8 | 44% | 26.4% | 0.3 |

| Chenbro (TP implied) | 8210.TW | Neutral | 20.2 | 44% | 26.4% | 0.3 |

| Peers | ||||||

| Karrie | 1050.HK | NC | 7.5 | 31% | 12% | 0.2 |

| King Slide | 2059.TW | Buy | 31.3 | 37% | 72.1% | 0.3 |

| AVC | 3017.TW | Buy | 20.9 | 32% | 25.4% | 0.4 |

| Repon | 6584.TW | NC | 26.9 | 64% | 44.3% | 0.2 |

| Auras | 3324.TWO | Buy | 14.2 | 23% | 19.1% | 0.3 |

| Fositek | 6805.TW | Buy | 17.7 | 32% | 26.1% | 0.3 |

| AVG. | 19.7 | 36% | 33% | 0.3 |

NC: Not Covered - estimates are from Bloomberg consensus

Source: Goldman Sachs Global Investment Research, Bloomberg

Exhibit 7: Chenbro 12M forward PE ratio

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg

Upside / Downside risks

- Faster / slower-than-expected AI infrastructure investments: Faster / n slower-than-expected AI infrastructure investments would enlarge / decrease the addressable market of servers chassis and racks for Chenbro, bringing potential upside / downside to our current estimates.

- Faster / slower-than-expected rack business ramp up , which could be caused by n more / less di ff erent racks needed in AI data center to facilitate AI tasks workloads, such as CPU server racks, networking racks, power racks, liquid cooling CDU racks, etc. It could enlarge / decrease Chenbro's racks business addressable market, bringing potential upside / downside to our current estimates.

- Healthier / fi ercer-than-expected competition , which could be caused by fast / n slow growth AI infrastructure upcycle with fast speci fi cation upgrade, leading to less new entrants and healthy competition, bringing potential upside / downside to our current estimates.

Exhibit 8: Chenbro QFII holdings

Source: TEJ

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Financial tables

Exhibit 9: Chenbro P&L

| NT$ mn | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Income statement | ||||||||||||||

| Revenue | 11,247 | 14,517 | 22,001 | 35,520 | 49,221 | 67,376 | 4,154 | 5,443 | 5,665 | 6,740 | 7,107 | 7,825 | 9,539 | 11,049 |

| Gross profit | 2,574 | 3,790 | 6,594 | 11,138 | 15,334 | 21,441 | 1,199 | 1,628 | 1,775 | 1,992 | 2,333 | 2,492 | 2,923 | 3,390 |

| OP income | 1,435 | 2,443 | 4,708 | 8,796 | 12,627 | 18,274 | 834 | 1,229 | 1,290 | 1,355 | 1,766 | 1,913 | 2,336 | 2,781 |

| Net income | 1,085 | 1,934 | 3,558 | 6,521 | 9,324 | 13,564 | 667 | 829 | 993 | 1,069 | 1,336 | 1,420 | 1,716 | 2,049 |

| EPS, diluted (NT$) | 8.95 | 15.48 | 28.41 | 51.33 | 73.39 | 106.76 | 5.33 | 6.64 | 7.93 | 8.51 | 10.52 | 11.18 | 13.50 | 16.13 |

| Ratios | ||||||||||||||

| Opex ratio | 10% | 9% | 9% | 7% | 6% | 5% | 9% | 7% | 9% | 9% | 8% | 7% | 6% | 6% |

| Tax rate | 23% | 24% | 24% | 25% | 25% | 25% | 25% | 26% | 24% | 23% | 24% | 24% | 25% | 25% |

| Margins | ||||||||||||||

| Gross margin | 22.9% | 26.1% | 30.0% | 31.4% | 31.2% | 31.8% | 28.9% | 29.9% | 31.3% | 29.6% | 32.8% | 31.9% | 30.6% | 30.7% |

| Operating margin | 12.8% | 16.8% | 21.4% | 24.8% | 25.7% | 27.1% | 20.1% | 22.6% | 22.8% | 20.1% | 24.9% | 24.4% | 24.5% | 25.2% |

| Net margin | 9.7% | 13.3% | 16.2% | 18.4% | 18.9% | 20.1% | 16.1% | 15.2% | 17.5% | 15.9% | 18.8% | 18.2% | 18.0% | 18.5% |

| YoY | ||||||||||||||

| Revenue | 7% | 29% | 52% | 61% | 39% | 37% | 50% | 51% | 33% | 74% | 71% | 44% | 68% | 64% |

| Gross profit | 21% | 47% | 74% | 69% | 38% | 40% | 74% | 78% | 44% | 108% | 95% | 53% | 65% | 70% |

| OP income | 25% | 70% | 93% | 87% | 44% | 45% | 110% | 111% | 46% | 135% | 112% | 56% | 81% | 105% |

| Net income | 9% | 78% | 84% | 83% | 43% | 45% | 83% | 83% | 54% | 127% | 100% | 71% | 73% | 92% |

| QoQ | ||||||||||||||

| Revenue | 7% | 31% | 4% | 19% | 5% | 10% | 22% | 16% | ||||||

| Gross profit | 25% | 36% | 9% | 12% | 17% | 7% | 17% | 16% | ||||||

| OP income | 44% | 47% | 5% | 5% | 30% | 8% | 22% | 19% | ||||||

| Net income | 41% | 24% | 20% | 8% | 25% | 6% | 21% | 19% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 10: Chenbro balance sheet

| NT$ mn | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|

| Balance Sheet | ||||||

| Cash and equivalents | 2,947 | 3,800 | 5,688 | 7,037 | 10,953 | 13,431 |

| Accounts receivable | 3,667 | 3,736 | 6,566 | 9,005 | 12,572 | 16,963 |

| Inventory | 1,843 | 2,187 | 3,925 | 5,293 | 7,519 | 9,848 |

| Other current assets | 131 | 862 | 404 | 404 | 404 | 404 |

| Current assets | 8,588 | 10,585 | 16,583 | 21,738 | 31,448 | 40,646 |

| Net PP&E/Fixed assets | 4,875 | 5,314 | 5,591 | 6,851 | 7,184 | 7,519 |

| Net intangibles | 73 | 65 | 57 | 58 | 58 | 58 |

| Other long-term assets | 451 | 680 | 1,225 | 1,225 | 1,225 | 1,225 |

| Non-current assets | 5,399 | 6,059 | 6,873 | 8,134 | 8,468 | 8,803 |

| Total assets | 13,987 | 16,644 | 23,456 | 29,872 | 39,916 | 49,448 |

| Accounts payable | 4,491 | 5,236 | 8,356 | 8,210 | 14,629 | 16,078 |

| Short-term debt | 820 | 995 | 1,589 | 1,900 | 1,000 | 500 |

| Other current liabilities | 372 | 402 | 969 | 2,429 | 3,812 | 5,902 |

| Current liabilities | 5,683 | 6,632 | 10,914 | 12,539 | 19,441 | 22,480 |

| Long-term debt | 2,701 | 2,671 | 1,332 | 2,700 | 1,000 | 500 |

| Other long-term liabilities | 26 | 76 | 134 | 134 | 134 | 134 |

| Non-current liabilities | 2,726 | 2,748 | 1,466 | 2,834 | 1,134 | 634 |

| Total liabilities | 8,409 | 9,380 | 12,380 | 15,374 | 20,575 | 23,115 |

| Common stock | 1,355 | 1,593 | 2,825 | 2,825 | 2,825 | 2,825 |

| Retained earnings | 4,359 | 5,691 | 8,344 | 11,650 | 16,376 | 23,252 |

| Other common equity | (187) | (110) | (284) | (284) | (284) | (284) |

| Total common equity | 5,527 | 7,174 | 10,885 | 14,191 | 18,917 | 25,793 |

| Minority interest | 51 | 90 | 192 | 308 | 424 | 540 |

| Total equity | 5,578 | 7,264 | 11,077 | 14,499 | 19,342 | 26,334 |

| BVPS | 45.59 | 57.44 | 86.90 | 111.70 | 148.90 | 203.02 |

| Cash conversion cycle | ||||||

| Account receivable days | 99 | 93 | 85 | 80 | 80 | 80 |

| Inventory days | 89 | 69 | 72 | 69 | 69 | 69 |

| Net payable days | 157 | 165 | 161 | 124 | 123 | 122 |

| Cash conversion cycle | 31 | (4) | (3) | 25 | 26 | 27 |

| Ratios | ||||||

| ROE (common equity) | 21% | 30% | 39% | 52% | 56% | 61% |

| ROA | 8% | 13% | 18% | 24% | 27% | 30% |

| Net debt to total equity | 10% | -2% | -25% | -17% | -46% | -47% |

| Net cash per share (NTD) | (4.77) | 1.11 | 22.60 | 19.56 | 71.89 | 99.81 |

| Total liabilities to total assets | 60% | 56% | 53% | 51% | 52% | 47% |

| Dupont analysis | ||||||

| Asset turnover | 0.9 | 0.9 | 1.1 | 1.3 | 1.4 | 1.5 |

| Leverage (assets to equity) | 2.5 | 2.4 | 2.2 | 2.1 | 2.1 | 2.0 |

| Net margin | 10% | 13% | 16% | 18% | 19% | 20% |

| ROE (total equity) | 21% | 30% | 39% | 51% | 55% | 59% |

| ROE (common equity) | 21% | 30% | 39% | 52% | 56% | 61% |

| ROA | 8% | 13% | 18% | 24% | 27% | 30% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 11: Chenbro cash fl ow

| NT$ mn | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|

| Cash flow statement | ||||||

| Net income | 1,085 | 1,934 | 3,558 | 6,521 | 9,324 | 13,564 |

| Minority interest add-back | 22 | 38 | 102 | 116 | 116 | 116 |

| Depreciation and amortization add-back | 298 | 346 | 387 | 457 | 491 | 514 |

| (Increase)/decrease in working capital | 847 | 332 | (1,447) | (3,953) | 626 | (5,271) |

| Other operating cash flow items | 272 | 48 | 486 | 0 | - | - |

| Cash flow from operating | 2,524 | 2,697 | 3,087 | 3,141 | 10,557 | 8,923 |

| Capital expenditure | (215) | (789) | (984) | (1,705) | (812) | (835) |

| Other investment cash flow items | (18) | (800) | 491 | (13) | (13) | (13) |

| Cash flow from investing | (234) | (1,589) | (493) | (1,718) | (825) | (849) |

| Dividends paid | (483) | (603) | (907) | (1,754) | (3,215) | (4,597) |

| Change in common stock | - | 238 | 1,231 | - | - | - |

| Increase/(decrease) in short-term debt | (733) | 175 | 594 | 311 | (900) | (500) |

| Increase/(decrease) in long-term debt | 48 | (29) | (1,339) | 1,368 | (1,700) | (500) |

| Other financing cash flow items | (7) | (129) | (284) | - | - | - |

| Cash flow from financing | (1,175) | (348) | (705) | (75) | (5,815) | (5,597) |

| Net change in cash | 1,094 | 853 | 1,888 | 1,348 | 3,917 | 2,477 |

| FCF | 2,309 | 1,907 | 2,103 | 1,437 | 9,745 | 8,088 |

| Ratio | ||||||

| Capex to revenue | 2% | 5% | 4% | 5% | 2% | 1% |

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology: Chenbro

Valuation: We use near-term P/E to derive our 12-month target price for Chenbro, consistent with our Taiwan Technology coverage. We base our target price of NT$1,482 on a target P/E multiple of 20.2x on forward year EPS (2027E). Our target P/E of 20.2x is derived from the peers avg. ratio of trading PE to forward year fundamentals (NI YoY and OPM). We have a Neutral rating on Chenbro on fair valuation. Key upside / downside risks: faster / slower-than-expected AI infrastructure investments, fast / slow-than-expected rack business ramp up, or healthier / fi ercer-than-expected competition.

Investment Thesis: Chenbro

Chenbro is a global leading server chassis supplier mainly serving CSP (cloud service providers) clients, o ff ering L3 to L6 services, which is chassis and layout, and integrate the chassis with power supply units, cables, backplanes, and motherboard, and testing services (e.g. input / output testing and power on test). We expect Chenbro to grow on AI servers ramp up and general servers recovery along with new rack business. At current levels, we believe positives are largely in the price, and we are Neutral-rated on Chenbro.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM