PDF 原檔:報告_GS_上詮_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的,不照 trimmed 引用順序猜。建立步驟見

ingest_steps.mdStep 2.5。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_gs_FOCI-buy-initiation_009.png |

42KB | 真資料圖 | FOCI FAU 實物尺寸對比照,黑色 FAU 元件放在新台幣 1 元硬幣旁,顯示元件尺寸極小 |

260706_gs_FOCI-buy-initiation_001.png |

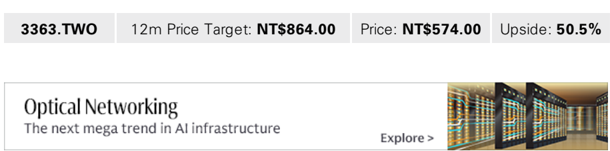

51KB | 文字卡 | GS 報告標頭:3363.TWO 12m PT NT$864.00 / Price NT$574.00 / Upside 50.5%;下方「Optical Networking」橫幅 |

260706_gs_FOCI-buy-initiation_005.png |

60KB | 真資料圖 | 美國雲端服務商 Capex 趨勢長條圖 2019–2028E(Amazon / Meta / Alphabet / Microsoft / Oracle),附 Blended YoY 折線 |

260706_gs_FOCI-buy-initiation_018.png |

77KB | 真資料圖 | FAU 與 GlassBridge 結構對比圖:左側 FAU 含 Fiber→Lens→V-groove→Glue→PIC;右側 GlassBridge 以玻璃直接橋接 Fiber 至 PIC |

260706_gs_FOCI-buy-initiation_017.png |

92KB | 真資料圖 | FOCI 光纖陣列電纜實物照片,多彩色光纖排列在白色連接頭兩端 |

260706_gs_FOCI-buy-initiation_010.png |

108KB | 真資料圖 | FAU 在 CPO switch 中位置的 3D 渲染圖,標示「1 FAU」,顯示 FAU 與晶片封裝整合示意 |

260706_gs_FOCI-buy-initiation_022.png |

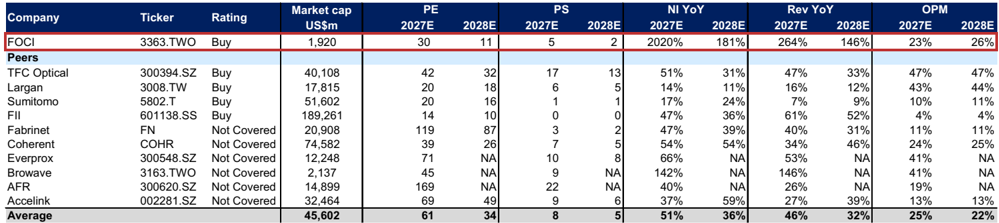

111KB | 真資料圖 | FOCI 同業比較表:PE / PS / NI YoY / Rev YoY / OPM(2027E/2028E),列示 FOCI vs TFC Optical / Largan / Sumitomo / FII / Fabrinet / Coherent / Everprox / Browave / AFR / Accelink |

260706_gs_FOCI-buy-initiation_013.png |

112KB | 真資料圖 | CPO 架構示意圖:兩個 XPU 透過 FAU 連接各自的 Optical Engine(含 PIC / Modulator / Photo detector / EIC / Driver / TIA) |

260706_gs_FOCI-buy-initiation_015.png |

130KB | 真資料圖 | 光學技術遷移路線圖:Pluggable transceivers(EML→Silicon Photonics,2024)→ CPO with switch(2026)→ CPO with XPU(時程未定),含硬體示意圖 |

260706_gs_FOCI-buy-initiation_014.png |

136KB | 真資料圖 | 資料中心 Scale-up racks 與 Scale-out clusters 連接架構圖:標示 TOR/EoR Switches、Servers、PCB midplanes、AEC/AOC/DAC 纜線及 CPO/NPO 位置 |

260706_gs_FOCI-buy-initiation_021.png |

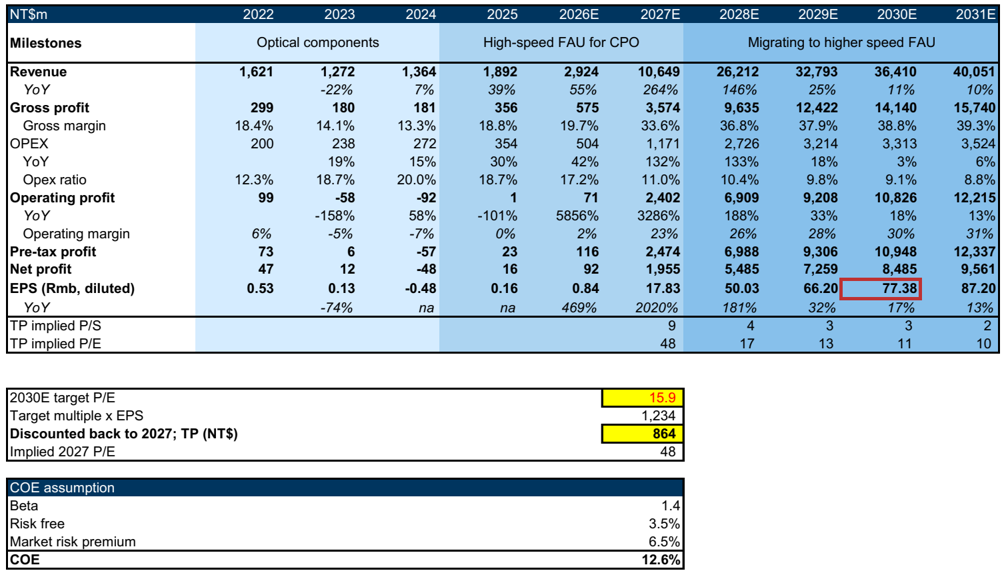

221KB | 真資料圖 | FOCI P&L 摘要表(2022-2031E)含 Revenue / Gross profit / OPEX / Operating profit / Net profit / EPS;下方折現 P/E 估值計算:2030E P/E 15.9x → 目標 NT$1,234,折現至 2027E TP=NT$864(COE 12.6%) |

原始內容

For the exclusive use of KEVINLU@LENOVO.COM

FOCI (3363.TWO)

FAU for CPO switch riding on optical networking migration; Initiate at Buy with TP at NT$864

We identify FOCI as a key bene fi ciary of the optical networking migration trend and expect its net income to grow at a 250% CAGR in 2025-30E, driven by (1) FAU ( fi ber array unit) used in CPO switches, carrying higher ASP and GM, along with healthier competition and continuous speci fi cation upgrades (3.2T, 6.4T, and more advanced), (2) growing CPO switch demand (see our Optical Networking thematic), riding on the AI infrastructure upcycle, (3) early participation with global-leading CPO switch brand makers and chipset suppliers, supporting its timely product design amid fast technology migration, (4) automated production driving manufacturing e ffi ciency and yield rates, and (5) a strong commitment to capacity expansion to support the CPO FAU shipment ramp-up. We initiate FOCI at Buy with a 12-month target price of NT$864 (which implies 48x 2027E P/E vs. 1,100% NI YoY in 2027-28E).

Key debate: There are market concerns that new technologies (e.g., GlassBridge) could replace FAU; however, we argue that for a technology to become mainstream, it requires stable performance and a ff ordable costs in mass production, along with the related system support and supply chain readiness. Our supply chain checks suggest: (1) it is normal that other solutions (e.g., glass, metal, etc.) are proposed to connect fi bers and chips, but FAU continues to be the one chosen by customers, and (2) FAU is also evolving, including more channels (toward 100+ channels vs. 24+ channels for GlassBridge, link), narrower pitch, 2D architecture, and heat-resistant materials to withstand the heat during the re fl ow process. We believe GlassBridge is a complement to FAU rather than a replacement, and the strong AI server rack ramp-up, along with fast bandwidth upgrades, would continue to support FAU demand,

BUY

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu

+852-2978-0996 | yifan.hu@gs.com Goldman Sachs (Asia) L.L.C.

Key Data _____________________________________

Market cap: NT$62.9bn / $2.0bn

Enterprise value: NT$60.2bn / $1.9bn

3m ADTV: NT$2.8bn / $87.4mn

Taiwan

Greater China Technology

M&A Rank: 3

Leases incl. in net debt & EV?: Yes

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue (NT$ mn) | 1,892.0 | 2,924.3 | 10,648.7 | 26,212.1 |

| EBITDA (NT$ mn) | 124.2 | 248.5 | 2,897.4 | 7,764.7 |

| EPS (NT$) | 0.16 | 0.84 | 17.83 | 50.03 |

| P/E (X) | NM | NM | 32.2 | 11.5 |

| P/B (X) | 12.3 | 10.6 | 8.0 | 4.7 |

| Dividend yield (%) | 0.0 | 0.0 | 0.0 | 0.0 |

| N debt/EBITDA (ex lease,X) | (10.1) | (10.9) | (1.0) | (0.7) |

| CROCI (%) | 3.6 | 9.2 | 49.6 | 81.5 |

| FCF yield (%) | (0.8) | (2.9) | 0.4 | 4.4 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | (0.98) | (0.92) | 1.23 | 1.51 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

FOCI (3363.TWO)

Rating since Jul 6, 2026

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | NM | NM | 32.2 | 11.5 |

| P/B (X) | 12.3 | 10.6 | 8.0 | 4.7 |

| FCF yie l d (%) | (0.8) | (2.9) | 0.4 | 4.4 |

| EV/EBITDAR (X) | 242.5 | 242.4 | 20.7 | 7.4 |

| EV/EBITDA (exc l . l eases) (X) | 242.5 | 242.4 | 20.7 | 7.4 |

| CROCI (%) | 3.6 | 9.2 | 49.6 | 81.5 |

| ROE (%) | 0.6 | 2.2 | 28.3 | 51.6 |

| Net debt/equity (%) | (49.4) | (45.8) | (37.6) | (42.9) |

| Net debt/equity (exc l . l eases) (%) | (49.4) | (45.8) | (37.6) | (42.9) |

| Interest cover (X) | 0.1 | 8.4 | 285.2 | 820.3 |

| Days inventory outst, sa l es | 67.2 | 64.3 | 39.9 | 34.8 |

| Receivab l e days | 55.6 | 50.0 | 25.0 | 22.0 |

| Days p ayab l e outstandin g | 75.6 | 60.0 | 60.0 | 60.0 |

| DuPont ROE (%) | 0.6 | 1.6 | 24.8 | 41.0 |

| Turnover (X) | 0.6 | 0.4 | 1.1 | 1.5 |

| L evera g e (X) | 1.2 | 1.1 | 1.3 | 1.3 |

| G ross cas h invested (ex cas h ) (NT $ ) | 1,624.1 | 3,723.4 | 5,925.2 | 9,490.5 |

| Avera g e ca p ita l e mpl oyed (NT $ ) | 1,175.6 | 2,251.1 | 4,065.4 | 6,273.4 |

| BVP S (NT $ ) | 24.60 | 54.09 | 71.92 | 121.95 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | 38.7 | 54.6 | 264.1 | 146.2 |

| EBITDA growth | 445.7 | 100.1 | NM | 168.0 |

| EPS growth | 132.8 | 438.3 | 2,019.7 | 180.6 |

| DPS growth | NM | NM | NM | NM |

| EBIT margin | 0.1 | 2.4 | 22.6 | 26.4 |

| EBITDA margin | 6.6 | 8.5 | 27.2 | 29.6 |

| Net income margin | 0.9 | 3.2 | 18.4 | 20.9 |

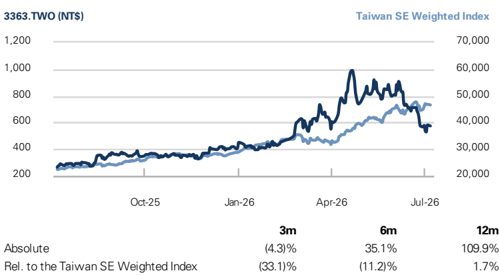

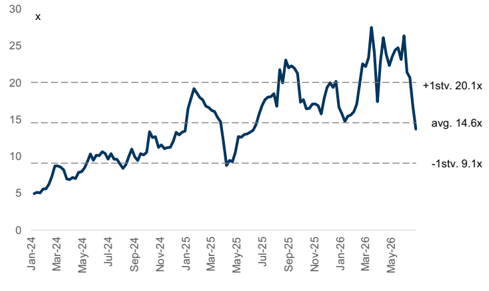

Price Performance __________________________________________

Source: FactSet. Price as of 6 Jul 2026 close.

Income Statement (NT$ mn) ________________________________

12/25

1,892.0

(1,536.4)

(142.2)

(212.3)

--

12

4.

2

(123.0)

1

2

.

11.1

4.4

22

8

.

(6.6)

--

--

16

.

2

--

16

2

.

0.

16

0.

16

0.

16

0.

16

--

0.0

,4

5

5

,4

12/28E

26,212.1

(16,577.2)

(891.2)

(1,834.8)

--

7

,

7

76

4.

(855.9)

6

.

8

8

,90

78.9

--

6

,9

87

7

.

(1,502.4)

--

--

85

.

3

--

85

3

.

5

0.0

3

5

3

0.0

5

0.0

3

5

0.0

3

--

0.0

9

9

12/26E

2,924.3

(2,349.4)

(200.3)

(303.6)

--

2

.

5

8

4

(177.5)

7

0.9

31.1

2.9

115

.9

(23.7)

--

--

2

.

2

--

2

2

.

0.

4

8

0.

4

8

0.

8

4

0.

8

4

--

0.0

12/27E

10,648.7

(7,075.1)

(425.9)

(745.4)

--

2

8

9

.4

7

,

(495.1)

2

,40

2

.

2

72.0

--

2

2

4.

,4

7

(519.6)

--

--

5

4.

6

--

,9

1

,9

1

5

4.

17

6

.

83

17

.

83

17

.

83

17

.

83

--

0.0

v

e

l

To

r

e

t

a

nu

e

Co

s

t of good

SG&A

R&D

Other operating inc./(exp.)

E

BITDA

Depreciation & amortization

E

BIT

Net intere t inc./(exp.)

s

Income/(lo ss

Pre-ta ss

) from a x p

t

r

ofi

Provi

s

s

ion for taxe

Minority intere

t

s

Preferred dividend

s

N

re-e et

.

inc xc

(p

Po

p

t

e

s

ion t-tax exceptional

N

ociate

s

a

ls)

s

et

E

P

E

E

xc inc

e

(pos

.

t-e

S (b

P

P

p

re-e sic

a

,

S (dilu

p

te

S (b

t

xc

,

ion

e

ls)

a

p

re-e

p

d

sic

,

a

t

xc pos

E

P

S (dilu t-e

te

d

,

) (N

e

xc pos

$)

T

p

e

t

p

t-e

DPS (NT$)

Div. payout ratio (%)

Balance Sheet (NT$ mn) ____________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| C a sh& c a sh equiv a lents | 1,412. 0 | 2,871.3 | 3,119.3 | 5,895.3 |

| Accounts receiv a ble | 281.3 | 519.9 | 938.8 | 2,221. 0 |

| Inventory | 4 0 8.7 | 621.2 | 1,7 0 4.9 | 3,291. 0 |

| Other current a ssets | 1 0 5.4 | 1 0 5.4 | 1 0 5.4 | 1 0 5.4 |

| Total c u rrent assets | 2 , 2 0 7 .4 | 4, 117 . 8 | 5 , 868 .4 | 11 , 512 . 7 |

| Net PP&E | 647.4 | 2,225.5 | 3,869.1 | 5,383.9 |

| Net int a ngibles | 22.4 | 22.4 | 29.1 | 33.1 |

| Tot a l investments | 0 . 0 | 0 . 0 | 0 . 0 | 0 . 0 |

| Other long-term a ssets | 279.9 | 279.9 | 279.9 | 279.9 |

| Total assets | 3, 157 . 1 | 6 , 6 4 5 . 6 | 1 0,04 6 . 5 | 17 , 2 09. 6 |

| Accounts p a y a ble | 332.5 | 439.9 | 1,886.1 | 3,563.9 |

| Short-term debt | 153.1 | 153.1 | 153.1 | 153.1 |

| Short-term le a se li a bilities | -- | -- | -- | -- |

| Other current li a bilities | 36.3 | 36.3 | 36.3 | 36.3 |

| Total c u rrent liabilities | 522 .0 | 62 9.4 | 2 ,0 75 . 6 | 3, 75 3.4 |

| Long-term debt | -- | -- | -- | -- |

| Long-term le a se li a bilities | -- | -- | -- | -- |

| Other long-term li a bilities | 86. 0 | 86. 0 | 86. 0 | 86. 0 |

| Total long-term liabilities | 86 .0 | 86 .0 | 86 .0 | 86 .0 |

| Total liabilities | 6 0 8 .0 | 715 .4 | 2 , 161 . 6 | 3, 8 39.4 |

| Preferred sh a res | -- | -- | -- | -- |

| Tot a l commonequity | 2,549.1 | 5,93 0 .2 | 7,884.9 | 13,37 0 .2 |

| Minority interest | -- | -- | -- | -- |

| Total liabilities &eq u ity | 3, 157 . 1 | 6 , 6 4 5 . 6 | 1 0,04 6 . 5 | 17 , 2 09. 6 |

| Net debt, a djusted | (1,258.8) | (2,718.2) | (2,966.2) | (5,742.2) |

Cash Flow (NT$ mn) ________________________________________

12/25

16.2

123.0

--

(78.3)

(78.3)

(

)

17

5

.

(218.9)

--

--

54.0

16

4.

)

8

--

--

153.1

(28.6)

12

5

4.

(

.

57

8

)

(236.3)

12/26E

92.2

177.5

--

(343.7)

--

(

4.0)

7

(1,740.0)

--

--

(15.7)

,

755

.

6

)

--

--

--

3,288.9

3,

288

.9

1

,4

5

9.4

12/27E

1,954.6

495.1

--

(56.4)

--

2

,393.3

(2,129.7)

--

--

(15.7)

,

1

4

5

.4)

--

--

--

0.0

0.0

2

4

7

.9

12/28E

5,485.3

855.9

--

(1,190.5)

--

5

15

,

8

0.

(2,359.1)

--

--

(15.7)

2

,3

7

4.

8

)

--

--

--

0.0

0.0

2

,

776

.0

(1,813.9)

263.6

2,791.7

Source: Company data, Goldman Sachs Research estimates.

) (N

t

xc

T

) (N

e

p

$)

T

$)

t

) (N

T

$)

s

Net income

D&A add-back

Minority interest add-back

Net (inc)/dec orking capital

w

Other operating cash flo

w

Cash flow

from operations

Capital expenditures

Acquisitions

Divestitures

Others

Cash from

investing flow

Repayment of lease liabilities

Dividends paid (common & pref)

Inc/(dec) in debt

Other financing cash flo

s

w

Cash financing

from flow

Total flow

cash

Free cash flo

w

s

old

(

(

1

(

2

(

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

driving FOCI's growth going forward.

Valuation: Our target price is based on a 2030E discounted P/E. Our target P/E multiple is derived from peers' trading P/E relative to their forward-year EPS YoY. Our TP implies 48x 2027E P/E with NI YoY at 1,100% in 2027-28E. Key downside risks: fi ercer-than-expected market competition, technology migration trends in optical networking, and slower-than-expected capacity ramp up.

e92c7a75ab8b4efbba794e6b187208c8

cambles. oo cor caper tellu

USSm

1,400,000

1,200,000

1,000,000

800,000

600,000

400,000

200,000

For the exclusive use of KEVINLU@LENOVO.COM

FOCI in six charts

34%

35%

90%

80%

70%

60%

50%

40%

Exhibit 1: FOCI's revenue and GM trends 30%

GM improvement on rising contribution from CPO FAU

0%

10%

0%

Source: Company data, Goldman Sachs Global Investment Research

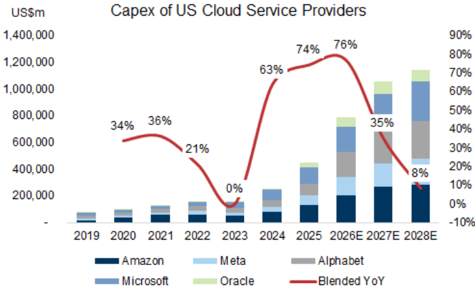

Exhibit 3: US CSP Capex trend

Data include Microsoft, Amazon, Meta, Alphabet and Oracle. For Microsoft, we use capex incl. fi nancial lease. In FY24, 50% of the capex of Microsoft was spent on land and 50% on AI/Cloud.

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 5: FOCI 12M forward P/S

Source: Company data, Goldman Sachs Global Investment Research

63% -

74%

76%

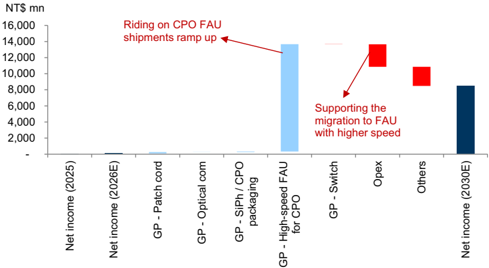

Exhibit 2: FOCI's NI waterfall chart 2025-30E CPO FAU as a key driver ahead

Source: Company data, Goldman Sachs Global Investment Research

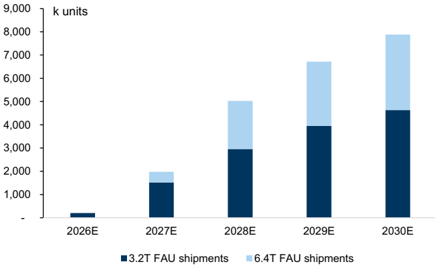

Exhibit 4: FOCI's FAU shipments trend

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 6: FOCI's 40 channel FAU for 3.2T or above CPO switch

Source: Company data

e92c7a75ab8b4efbba794e6b187208c8

eaiont.noee teSlie ToSA

1

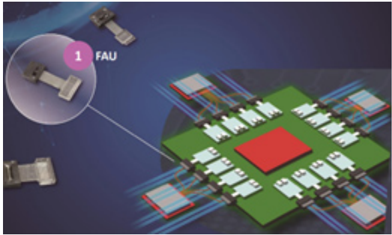

FAU

FOCI's products

Exhibit 7: FOCI's FAU in CPO switch

Source: Company data

Exhibit 9: FOCI's 100G LR4 TOSA

Source: Company data

Exhibit 11: FOCI's data center AOC

Source: Company data

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 8: FOCI's fi lter devices

Source: Company data

Exhibit 10: FOCI's 100G LR4 ROSA

Source: Company data

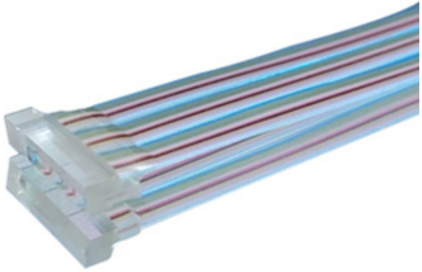

Exhibit 12: FOCI's polarization maintaining fi ber patchcords

Source: Company data

e92c7a75ab8b4efbba794e6b187208c8

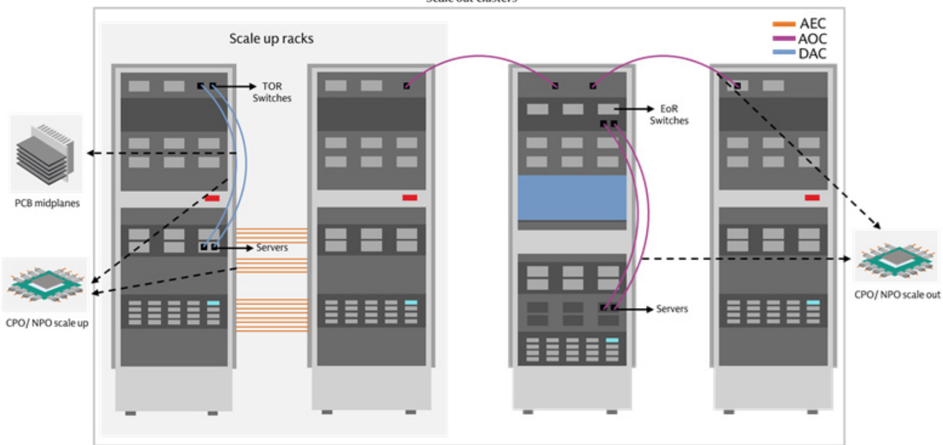

camble 14 comectrons I udla cellet. oedle up vo. oedle out

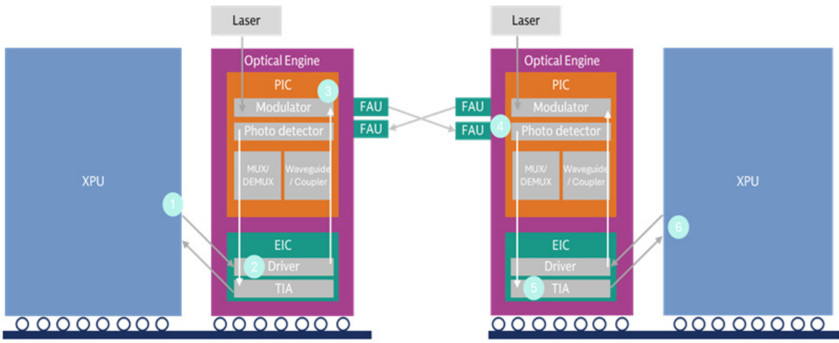

Laser

Scale up racks

Optical Engine

FAU to grow on rising CPO switch demand

Switches

Modulator

¡ Photo detector

Scale out clusters

FAU

FAU

FAU

Laser

Optical Engine

PIC

Modulator

EOR

Switches

Photo detector

To meet the increasing demand for bandwidth, power consumption, and miniaturization, the form of optical connection is evolving, such as expanding from the pluggable optical module to onboard optics (NPO) and co-packaged optics (CPO), covering short-distance connections with high bandwidth and better power e ffi ciency. We expect CPO will initially be integrated with the switch ASIC, followed by XPUs (GPUs, CPUs, ASICs, etc.). CPO/ NPO scale out

0000000-

00

Servers

00 • 00000000.

PCB midplanes

CPO/ NPO scale up

Exhibit 13: How CPO works in data transmission

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

Exhibit 14: Connections in data center: Scale-up vs. Scale-out

TOR Switch: Top of rack switch; EoR Switch: End of row switch

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

For the exclusive use of KEVINLU@LENOVO.COM

XPU

AEC

AOC

DAC

e92c7a75ab8b4efbba794e6b187208c8

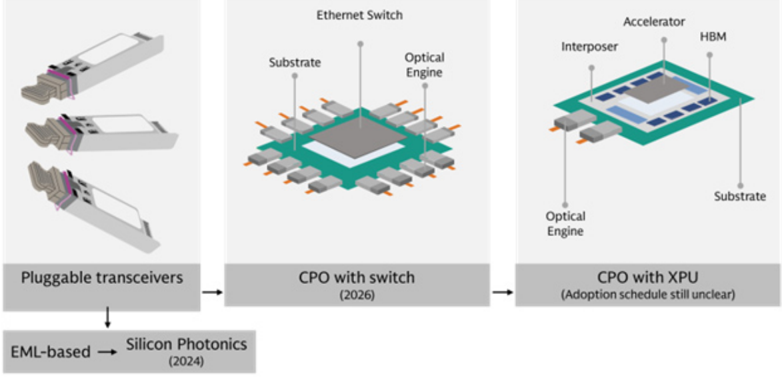

exmore 1o. ero switen specheation comparison

Nvid ia

Ethernet Switch

Spectrum-X Photonics

Substrate

InfiniBand

115.2Tb/s

4

28.8Tb/s

Accelerator

Interposer

Tomahawk 5 - Bailly

Engine

Optical

Ethernet

Ethernet

409.6 Tb/s

51.2 Tb/s

Exhibit 15: Optics technology migrations

102.4Tb/s

144 x 800G

200G/lane SerDes

18

72 (1.6T)

4U

Network

Switching capacity

of Switch ASIC

Switch ASIC

Ports

Speed

External laser source

Optical engines

Size

Pluggable transceivers

EML-based → Silicon Photonics

(2024)

For the exclusive use of KEVINLU@LENOVO.COM

51.2Tb/s

Ethernet

102.4 Tb/s

1

102.4Tb/s

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

Exhibit 16: CPO switch speci fi cation comparison

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

Co-Packaged Optics (CPO) expands optics to cover short-distance connections and higher bandwidth requirements. It places optical engines as close as possible to the chips, shortening the electrical paths from several centimeters to the millimeter level, lowering power consumption. The shorter transmission path also reduces latency and eliminates the need for DSPs and retimers, further reducing the overall power consumption of these devices. Additionally, this higher integration results in a smaller form factor.

On the other hand, CPO requires a comprehensive supply chain technology migration rather than a single-device upgrade, which could take time to develop. Furthermore, the co-packaging leads to higher maintenance costs. For instance, in a pluggable optical module, if the optical engine fails, one simply replaces the optical module while the switch system remains intact. Conversely, failures in highly-integrated systems have broader impacts: (1) with onboard optics / NPO, one would need to replace the switch PCB; (2) with CPO integrated into the switch, a failure would a ff ect the switch ASIC, and (3) with CPO integrated into a XPU, a failure would a ff ect the entire XPU (e.g., GPU, CPU, NPU, etc.).

Moreover, the lifecycles of PICs (Photonic Integrated Circuits) and EICs (Electronic Integrated Circuits) are di ff erent, with PICs being more delicate, which led to the design of the pluggable optical modules. As a result, we expect that: (1) pluggable optical

HBM

Broadcom e92c7a75ab8b4efbba794e6b187208c8

Exmolt 1o. ero switch bom redkaowll, by value (use)

BROADCOM

- nVIDIA

CPO switch BoM (Quantum-X Photonics)

US$

800G

Switch ASIC

1.6T

RANOVUS

MEDIATEK

Optical engines (1.6T)

3.2T

FAU

CPO

ELS

Scale up

Among which: CW laser (300mw)

Scale out

Shuffle box

OCS

MPO connectors/ cables

Scale up or scale out

Single mode Fiber

BoM

Note:

Markup

For the exclusive use of KEVINLU@LENOVO.COM

Microsoft

ASP|

Value

3,000

12,000

Exmore 19. ero switch bom bredkaown, by 7o (use)

Meta

V

Single mode

Fiber, 16%

Amazon

V

MPO

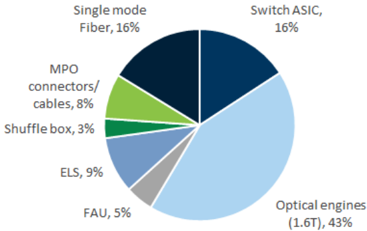

modules will co-exist with NPO / CPO, and continue speed migration toward 3.2T; (2) CPO will become more attractive to clients for short-distance and higher bandwidth applications that pluggable optical module cannot support; and (3) pluggable optical module suppliers will also enjoy new optics device opportunities within the NPO / CPO ecosystem, such as providing optical engines, FAUs, ELS modules.

75,803

Exhibit 17: CPO: Key development of major players

0: See progress in adoption

| Key players | Progress | Progress details | Highlights |

|---|---|---|---|

| - CPO Switch commercially available in 2026 (Scale out) | Mar-2025: Announced CPO switch (Quantum-X InfiniBand, Spectrum-X Ethernet) Early 2026: Commercial availability of CPO switch | Adopt MRM(Micro Ring Modulator) technology, achieving higher density and efficiency | |

| - Davisson (102.4T) CPO switch sampling in Oct 2025 (Scale-out and scale-up) | Mar-2022 : world's first 25.6T CPO Demo June-2023: 51.2T CPO sampling Mar-2024: Bailly (51.2T) CPO switch delivered to customers Oct-2025: Davisson (102.4T) CPO switch delivered to customers | Adopt MZM (Mach-Zehnder Modulator), which is more matured, while also developingMRM | |

| - CPO ethernet swith sampling in 2027 (Scale-out) - Developing CPO for XPUs (Scale-up) | Feb-2026: Acquired Celestial AI, a startup focusing on CPO for XPUs 2027: CPO (204T) Ethernet switch sampling | CPO solution to combine with custom XPUs for CSPs | |

| Announced co-developed CPO for ASIC in 2024 | Mar-2024: Announced Odin CPO solutions (6.4T) collaborating with Mediatek's ASIC platform | Targeting CPO technology on XPU |

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

Exhibit 18: CPO switch BoM breakdown, by value (GSe)

ASP estimates are based on industry checks

Exhibit 19: CPO switch BoM breakdown, by % (GSe)

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 20: Technology adoption by cloud service providers (CSPs)

(1.6T), 43%

Oracle

Switch ASIC,

16%

V

Chinese CSP

Nvidia

V

V

O (2028)

V

4

Source: Company data, Data compiled by Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

P Au Ae

U Ou

FAU vs. GlassBridge

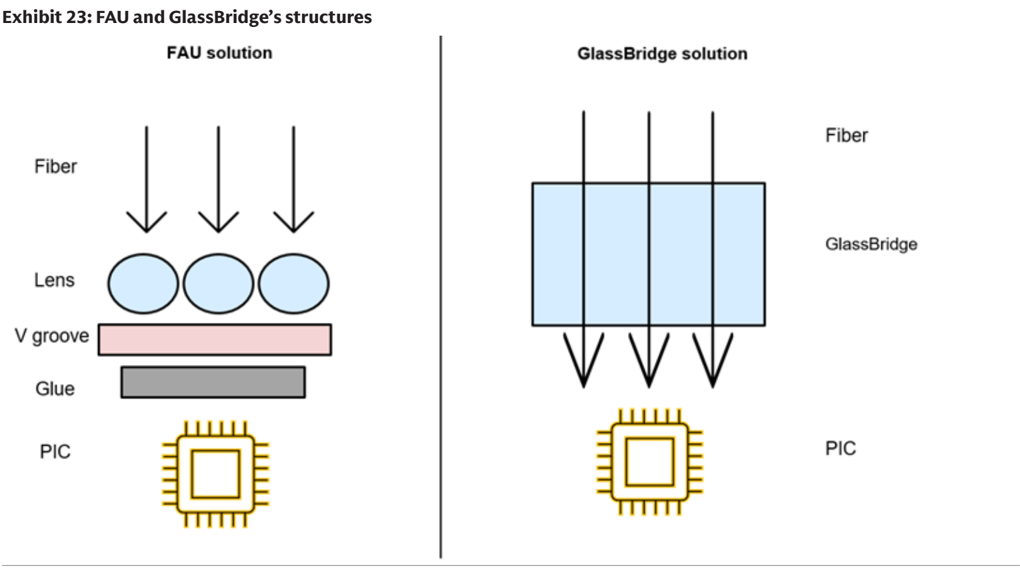

The FAU is a passive optical component that holds multiple optical fi bers in a precisely aligned array, typically using a V-groove substrate. Its functions include: (1) high-precision optical coupling: providing micron-level alignment between optical fi bers and the on-chip waveguides of the silicon photonic engine, (2) polarization management: FAUs often adopt polarization-maintaining fi bers to ensure stable optical performance and high Polarization Extinction Ratios (PER), and (3) high-density interconnect: FAUs enable high-density interconnect by arranging fi bers at a very tight pitch.

Exhibit 21: FOCI's FA solution for SiPh chip (1)

Source: Company data

Exhibit 22: FOCI's FA solution for SiPh chip (2)

Source: Company data

Corning Inc. (GLW, Not Covered) is the major player in GlassBridge in the market (link), which is a wafer level-manufactured fi ber-to-PIC technology designed as a detachable connector that supports 24+ optical channels. GlassBridge acts both as a high-precision glass component and as an integrated connector for fi ber and optical engine, used in next-generation optical networking products (e.g., NPO, CPO, etc.). GlassBridge adopts IOX (ion-exchange) waveguides, which are optical pathways integrated in glass that enable high-precision optical alignment and low-loss performance, ful fi lling the strict requirements in optical networking products used in AIDC.

The market is concerned that new technologies (e.g., GlassBridge) could replace

FAU ; however, we argue that for a technology to become mainstream, it requires stable performance and a ff ordable costs in mass production, along with related system support and supply chain readiness. Our supply chain checks suggest: (1) it is normal that other solutions (e.g., glass, metal) are proposed to connect fi bers and chips, but FAU continues to be the one chosen by customers, and (2) FAU is also evolving, including more channels (toward 100+ channels vs. 24+ channels for GlassBridge, link), narrower pitch, 2D architecture, and heat-resistant materials to withstand the heat during the re fl ow process. We believe GlassBridge is a complement to FAU rather than a replacement, and the strong AI server rack ramp-up, along with fast bandwidth upgrades, would continue to support FAU demand, driving FOCI's growth.

For the exclusive use of KEVINLU@LENOVO.COM

e92c7a75ab8b4efbba794e6b187208c8

Calwilco.rhu anlu dlaseblllse sotuctures

FAU solution

Fiber

Lens

V groove

Glue

PIC

For the exclusive use of KEVINLU@LENOVO.COM

GlassBridge solution

The rising demand for high-speed transmission drives high density, high precision, and high integration, lifting the entry barrier for FAUs: the size of FAUs will not increase, but the number of fi bers will keep doubling with the rising transmission speed if per-channel speed stays the same. The increasing density will raise the di ffi culty in both design and manufacturing, and in CPO, the FAU couples with the PIC via optical co-packaging, with one end connecting with the PIC, and the other end connecting to high-density fi ber optic cables, further lifting the entry barrier. FOCI works closely with a global-leading foundry to develop a standardized platform (IP ReLFACon: re fl owable lensed fi ber array connector). The ReLFACon is a connector or I/O (input/output) on the optical engine (EIC and PIC packaged together), connecting the optical engine and fi ber optic cables to transmit data in and out. The ReLFACon can withstand the high temperature (up to 280 degrees Celsius) during semiconductor packaging, and can connect multiple fi bers in a small space.

Source: Goldman Sachs Global Investment Research

Earnings estimates

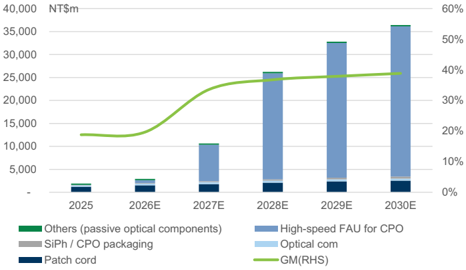

Revenues: +81% CAGR in 2025-30E, driven by: (1) Expanding from telecom to AIDC optical networking: FOCI provides optical components to telecom operators and is expanding to high-speed FAU used in the AIDC CPO switch, riding on the growing AI infrastructure trend globally, (2) CPO switch shipment ramp-up: FOCI serves major CPO switch players in the global market, and the rising end demand would drive FOCI's high-speed FAU shipment growth ahead, (3) Product migration: We model FOCI to enjoy the product migration from 3.2T to 6.4T FAU in coming years, leading to an ASP uptrend, and (4) Capacity expansion: FOCI raised capital in 2026 to support its capacity expansion plan for FAU, supporting the company's shipment growth ahead.

GM: Up from 19% in 2025 to 39% in 2030E on rising contribution from CPO FAU and e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

migration toward FAU with higher speed, which carries a higher GM than other product lines. Opex ratio: Improving from 18.7% in 2025 to 9.1% in 2030E on growing revenue scale and higher operational e ffi ciency, with R&D expense at a +59% CAGR to support the product speci fi cation upgrades. NI: +250% CAGR in 2025-30E, driven by the rising revenue scale and pro fi tability improvement.

Exhibit 24: FOCI P&L summary

| (NT$ m) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 411 | 582 | 508 | 391 | 382 | 433 | 1,032 | 1,077 | 1,364 | 1,892 | 2,924 | 10,649 | 26,212 | 32,793 | 36,410 |

| Gross profit | 71 | 115 | 121 | 49 | 7 | 12 | 257 | 298 | 181 | 356 | 575 | 3,574 | 9,635 | 12,422 | 14,140 |

| Operating expense | (77) | (83) | (110) | (84) | (163) | (147) | (95) | (99) | (272) | (354) | (504) | (1,171) | (2,726) | (3,214) | (3,313) |

| Operating income | (6) | 33 | 11 | (36) | (156) | (135) | 162 | 199 | (92) | 1 | 71 | 2,402 | 6,909 | 9,208 | 10,826 |

| Net income | 1 | 17 | 21 | (22) | (107) | (101) | 135 | 165 | (48) | 16 | 92 | 1,955 | 5,485 | 7,259 | 8,485 |

| EPS, diluted (NT$) | 0.01 | 0.16 | 0.20 | (0.22) | (0.98) | (0.92) | 1.23 | 1.51 | (0.48) | 0.16 | 0.84 | 17.83 | 50.03 | 66.20 | 77.38 |

| Margins / ratio | |||||||||||||||

| Gross margin | 17.2% | 19.8% | 23.8% | 12.4% | 1.9% | 2.7% | 24.9% | 27.7% | 13.3% | 18.8% | 19.7% | 33.6% | 36.8% | 37.9% | 38.8% |

| Opex ratio | -18.8% | -14.2% | -21.7% | -21.6% | -42.7% | -33.9% | -9.2% | -9.2% | -20.0% | -18.7% | -17.2% | -11.0% | -10.4% | -9.8% | -9.1% |

| Operating margin | -1.6% | 5.6% | 2.2% | -9.2% | -40.8% | -31.2% | 15.7% | 18.5% | -6.7% | 0.1% | 2.4% | 22.6% | 26.4% | 28.1% | 29.7% |

| Net margin | 0.3% | 2.9% | 4.1% | -5.7% | -28.0% | -23.4% | 13.1% | 15.3% | -3.5% | 0.9% | 3.2% | 18.4% | 20.9% | 22.1% | 23.3% |

| QoQ | |||||||||||||||

| Revenue | 14% | 41% | -13% | -23% | -2% | 13% | 139% | 4% | |||||||

| Gross profit | 110% | 63% | 5% | -60% | -85% | 63% | 2091% | 16% | |||||||

| Operating income | nm | nm | -66% | nm | nm | nm | nm | 23% | |||||||

| Net income | nm | 1420% | 22% | nm | nm | nm | nm | 22% | |||||||

| YoY | |||||||||||||||

| Revenue | 53% | 65% | 33% | 9% | -7% | -26% | 103% | 176% | 7% | 39% | 55% | 264% | 146% | 25% | 11% |

| Gross profit | 235% | 62% | 121% | 44% | -90% | -90% | 113% | 514% | 0% | 97% | 62% | 522% | 170% | 29% | 14% |

| Operating income | nm | 376% | nm | nm | nm | nm | 1382% | nm | nm | nm | 5856% | 3286% | 188% | 33% | 18% |

| Net income | nm | -34% | nm | nm | nm | nm | 557% | nm | nm | nm | 469% | 2020% | 181% | 32% | 17% |

Source: Company data, Goldman Sachs Global Investment Research

We expect CCC days to improve from 63 days in 2025 to 18 days in 2030E, mainly due to the gradually improving accounts receivable, inventory, and accounts payable days in the coming years, driven by the CPO FAU shipment ramp-up. We forecast ROE to increase to 34% in 2030E from 1% in 2025, mainly on improving asset turnover and net margins driven by the rising contribution from the high-margin CPO FAU business. We believe FCF should keep improving in the coming years, driven by higher operating cash fl ow as earnings scale up.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 25: FOCI's balance sheet

| NT$m | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|---|---|

| Balance Sheet | |||||||

| Cash and equivalents | 1,470 | 1,412 | 2,871 | 3,119 | 5,895 | 12,976 | 21,561 |

| Accounts receivable | 295 | 281 | 520 | 939 | 2,221 | 2,271 | 2,317 |

| Inventory | 288 | 409 | 621 | 1,705 | 3,291 | 3,406 | 3,549 |

| Other current assets | 88 | 105 | 105 | 105 | 105 | 105 | 105 |

| Current assets | 2,141 | 2,207 | 4,118 | 5,868 | 11,513 | 18,759 | 27,533 |

| Net PP&E/Fixed assets | 485 | 647 | 2,226 | 3,869 | 5,384 | 5,521 | 5,413 |

| Net intangibles | 32 | 22 | 22 | 29 | 33 | 36 | 37 |

| Other long-term assets | 309 | 280 | 280 | 280 | 280 | 280 | 280 |

| Non-current assets | 826 | 950 | 2,528 | 4,178 | 5,697 | 5,837 | 5,730 |

| Total assets | 2,967 | 3,157 | 6,646 | 10,047 | 17,210 | 24,596 | 33,263 |

| Accounts payable | 304 | 332 | 440 | 1,886 | 3,564 | 3,692 | 3,874 |

| Short-term debt | - | 153 | 153 | 153 | 153 | 153 | 153 |

| Other current liabilities | 43 | 36 | 36 | 36 | 36 | 36 | 36 |

| Current liabilities | 347 | 522 | 629 | 2,076 | 3,753 | 3,881 | 4,064 |

| Long-term debt | - | - | - | - | - | - | - |

| Other long-term liabilities | 89 | 86 | 86 | 86 | 86 | 86 | 86 |

| Non-current liabilities | 89 | 86 | 86 | 86 | 86 | 86 | 86 |

| Total liabilities | 437 | 608 | 715 | 2,162 | 3,839 | 3,967 | 4,150 |

| Common stock | 2,476 | 2,500 | 5,789 | 5,789 | 5,789 | 5,789 | 5,789 |

| Retained earnings | 276 | 273 | 366 | 2,320 | 7,806 | 15,064 | 23,549 |

| Other common equity | (222) | (225) | (225) | (225) | (225) | (225) | (225) |

| Total common equity | 2,531 | 2,549 | 5,930 | 7,885 | 13,370 | 20,629 | 29,113 |

| Minority interest | - | - | - | - | - | - | - |

| Total equity | 2,531 | 2,549 | 5,930 | 7,885 | 13,370 | 20,629 | 29,113 |

| BVPS (NT$) | 25.00 | 24.59 | 54.09 | 71.92 | 121.95 | 188.15 | 265.53 |

| Cash conversion cycle | |||||||

| Account receivable days | 78 | 56 | 50 | 25 | 22 | 25 | 23 |

| Inventory days | 82 | 83 | 80 | 60 | 55 | 60 | 57 |

| Net payable days | 73 | 76 | 60 | 60 | 60 | 65 | 62 |

| Cash conversion cycle | 87 | 63 | 70 | 25 | 17 | 20 | 18 |

| Ratios | |||||||

| ROE (common equity) | -2% | 1% | 2% | 28% | 52% | 43% | 34% |

| ROA | -2% | 1% | 2% | 23% | 40% | 35% | 29% |

| Net debt to total equity | -58% | -49% | -46% | -38% | -43% | -62% | -74% |

| Net cash per share (NT$) | 14.52 | 12.15 | 24.79 | 27.05 | 52.37 | 116.95 | 195.26 |

| Total liabilities to total assets | 15% | 19% | 11% | 22% | 22% | 16% | 12% |

| Dupont analysis | |||||||

| Asset turnover | 0.5 | 0.6 | 0.6 | 1.3 | 1.9 | 1.6 | 1.3 |

| Leverage (assets to equity) | 1.2 | 1.2 | 1.2 | 1.2 | 1.3 | 1.2 | 1.2 |

| Net margin | -4% | 1% | 3% | 18% | 21% | 22% | 23% |

| CROCI (EDBITA/total equity) | 1% | 5% | 4% | 37% | 58% | 50% | 41% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 26: FOCI's cash fl ow statement

| NT$m | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E |

|---|---|---|---|---|---|---|---|

| Cash flow statement | |||||||

| Net income | (48) | 16 | 92 | 1,955 | 5,485 | 7,259 | 8,485 |

| Minority interest add-back | - | - | - | - | - | - | - |

| Depreciation and amortization add-back | 114 | 123 | 178 | 495 | 856 | 1,187 | 1,215 |

| (Increase)/decrease in working capital | 81 | (78) | (344) | (56) | (1,191) | (38) | (6) |

| Other operating cash flow items | (77) | (78) | - | - | - | - | - |

| Cash flow from operating | 70 | (17) | (74) | 2,393 | 5,151 | 8,408 | 9,693 |

| Capital expenditure | (182) | (219) | (1,740) | (2,130) | (2,359) | (1,312) | (1,092) |

| Other investment cash flow items | 200 | 54 | (16) | (16) | (16) | (16) | (16) |

| Cash flow from investing | 19 | (165) | (1,756) | (2,145) | (2,375) | (1,327) | (1,108) |

| Dividends paid | (49) | - | - | - | - | - | - |

| Change in common stock | 473 | 24 | 3,289 | - | - | - | - |

| Increase/(decrease) in short-term debt | - | 153 | - | - | - | - | - |

| Increase/(decrease) in long-term debt | - | - | - | - | - | - | - |

| Other financing cash flow items | 30 | (56) | - | - | - | - | - |

| Cash flow from financing | 453 | 122 | 3,289 | - | - | - | - |

| Net change in cash | 557 | (58) | 1,459 | 248 | 2,776 | 7,081 | 8,585 |

| FCF | (112) | (236) | (1,814) | 264 | 2,792 | 7,096 | 8,601 |

| Ratio | |||||||

| Capex to revenue | 13% | 12% | 60% | 20% | 9% | 4% | 3% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Valuation and Risks

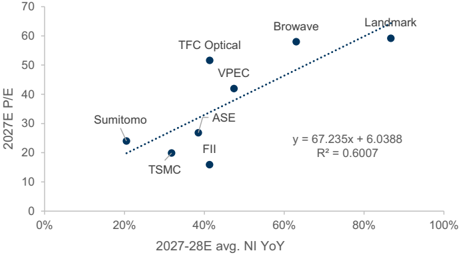

We derive our 12-month target price of NT$864 based on a discounted P/E methodology to capture the company's long-term growth, which is consistent with our Greater China Tech coverage. Our 2030E target P/E multiple of 15.9x is based on the peers' correlation between forward-year trading P/E and earnings growth, with FOCI's 2030-31E average net income YoY at 15%. We apply the 15.9x target P/E to 2030E EPS and discount it back to 2027E with a COE of 12.6%. With a potential 49% upside to our target price, we initiate coverage on FOCI at Buy. Our TP-implied PEG is at 0.8x, within the peers' range of 0.3x-1.2x.

Exhibit 27: Our target P/E multiple is derived from peers' correlation between P/E and forward-year NI YoY growth

Estimates for not covered (NC) names are based on consensus.

Source: Company data, Goldman Sachs Global Investment Research, Re fi nitiv Eikon

Exhibit 29: FOCI and peers' PEG ratio

| Company | FOCI | Company | FII | Browave | Landmark | VPEC | TFC Optical | Sumitomo | ASE | TSMC |

|---|---|---|---|---|---|---|---|---|---|---|

| Ticker | 3363.TWO | Ticker | 601138.SS | 3163.TWO | 3081.TWO | 2455.TW | 300394.SZ | 5802.T | ASX | 2330.TW |

| Rating | Buy | Rating | Buy | NC | Buy | Buy | Buy | Buy | NC | Buy |

| 2030E TP implied P/E | 11 | 2027E trading P/E | 16 | 58 | 59 | 42 | 52 | 24 | 27 | 20 |

| 2030-31E avg. NI YoY | 15% | 2027-28E avg. NI YoY | 41% | 63% | 87% | 47% | 41% | 1.2 | 0.7 | 0.6 |

| PEG | 0.8 | PEG | 0.4 | 0.9 | 0.7 | 0.9 | 1.2 | 0.2 | 0.4 | 0.3 |

Estimates for not covered (NC) names are based on consensus.

Source: Company data, Goldman Sachs Global Investment Research, Re fi nitiv Eikon

Exhibit 28: FOCI's 12M forward P/S

Source: Re fi nitiv Eikon

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 30: FOCI's discounted P/E

| NT$m | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E | 2031E |

|---|---|---|---|---|---|---|---|---|---|---|

| Milestones | Optical components | Optical components | Optical components | High-speed FAU for CPO | High-speed FAU for CPO | High-speed FAU for CPO | Migrating to higher speed FAU | Migrating to higher speed FAU | Migrating to higher speed FAU | Migrating to higher speed FAU |

| Revenue | 1,621 | 1,272 | 1,364 | 1,892 | 2,924 | 10,649 | 26,212 | 32,793 | 36,410 | 40,051 |

| YoY | -22% | 7% | 39% | 55% | 264% | 146% | 25% | 11% | 10% | |

| Gross profit | 299 | 180 | 181 | 356 | 575 | 3,574 | 9,635 | 12,422 | 14,140 | 15,740 |

| Gross margin | 18.4% | 14.1% | 13.3% | 18.8% | 19.7% | 33.6% | 36.8% | 37.9% | 38.8% | 39.3% |

| OPEX | 200 | 238 | 272 | 354 | 504 | 1,171 | 2,726 | 3,214 | 3,313 | 3,524 |

| YoY | 19% | 15% | 30% | 42% | 132% | 133% | 18% | 3% | 6% | |

| Opex ratio | 12.3% | 18.7% | 20.0% | 18.7% | 17.2% | 11.0% | 10.4% | 9.8% | 9.1% | 8.8% |

| Operating profit | 99 | -58 | -92 | 1 | 71 | 2,402 | 6,909 | 9,208 | 10,826 | 12,215 |

| YoY | -158% | 58% | -101% | 5856% | 3286% | 188% | 33% | 18% | 13% | |

| Operating margin | 6% | -5% | -7% | 0% | 2% | 23% | 26% | 28% | 30% | 31% |

| Pre-tax profit | 73 | 6 | -57 | 23 | 116 | 2,474 | 6,988 | 9,306 | 10,948 | 12,337 |

| Net profit | 47 | 12 | -48 | 16 | 92 | 1,955 | 5,485 | 7,259 | 8,485 | 9,561 |

| EPS (Rmb, diluted) | 0.53 | 0.13 | -0.48 | 0.16 | 0.84 | 17.83 | 50.03 | 66.20 | 77.38 | 87.20 |

| YoY | -74% | na | na | 469% | 2020% | 181% | 32% | 17% | 13% | |

| TP implied P/S | 9 | 4 | 3 | 3 | 2 | |||||

| TP implied P/E | 48 | 17 | 13 | 11 | 10 |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 31: FOCI's peers comp table

| Company | Ticker | Rating | Market cap | PE | PE | PS | PS | NI YoY | NI YoY | Rev YoY | Rev YoY | OPM | OPM |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Company | Ticker | Rating | US$m | 2027E | 2028E | 2027E | 2028E | 2027E | 2028E | 2027E | 2028E | 2027E | 2028E |

| FOCI | 3363.TWO | Buy | 1,920 | 30 | 11 | 5 | 2 | 2020% | 181% | 264% | 146% | 23% | 26% |

| Peers | |||||||||||||

| TFC Optical | 300394.SZ | Buy | 40,108 | 42 | 32 | 17 | 13 | 51% | 31% | 47% | 33% | 47% | 47% |

| Largan | 3008.TW | Buy | 17,815 | 20 | 18 | 6 | 5 | 14% | 11% | 16% | 12% | 43% | 44% |

| Sumitomo | 5802.T | Buy | 51,602 | 20 | 16 | 1 | 1 | 17% | 24% | 7% | 9% | 10% | 11% |

| FII | 601138.SS | Buy | 189,261 | 14 | 10 | 0 | 0 | 47% | 36% | 61% | 52% | 4% | 4% |

| Fabrinet | FN | Not Covered | 20,908 | 119 | 87 | 3 | 2 | 47% | 39% | 40% | 31% | 11% | 11% |

| Coherent | COHR | Not Covered | 74,582 | 39 | 26 | 7 | 5 | 54% | 54% | 34% | 46% | 24% | 25% |

| Everprox | 300548.SZ | Not Covered | 12,248 | 71 | NA | 10 | 8 | 66% | NA | 53% | NA | 41% | NA |

| Browave | 3163.TWO | Not Covered | 2,137 | 45 | NA | 9 | NA | 142% | NA | 146% | NA | 41% | NA |

| AFR | 300620.SZ | Not Covered | 14,899 | 169 | NA | 22 | NA | 40% | NA | 26% | NA | 19% | NA |

| Accelink | 002281.SZ | Not Covered | 32,464 | 69 | 49 | 9 | 6 | 37% | 59% | 27% | 39% | 13% | 13% |

| Average | 45,602 | 61 | 34 | 8 | 5 | 51% | 36% | 46% | 32% | 25% | 22% |

Data as of Jul 3, 2026. Estimates for not covered (NC) names are based on consensus.

Source: Company data, Goldman Sachs Global Investment Research, Re fi nitiv Eikon

M&A framework: We assign an M&A rank of 3 (indicating a low probability of the company being acquired) to FOCI, given its long operational history and that it is currently in a rapid growth stage driven by its CPO FAU business, and therefore, we do not include any M&A component in our price target.

Key downside risks

- Fiercer-than-expected market competition: We see peers proactively developing n and promoting their FAU products, and fi ercer-than-expected market competition could weigh on FOCI's revenue and earnings growth.

- Technology migration trend in optical networking: We see fast technology n migration in the optical networking market, and the development of new solutions that could outperform FAU could drag on FOCI's growth going forward, as we model

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

FAU as FOCI's key growth driver.

- Slower-than-expected capacity ramp up: FOCI is expanding its CPO FAU capacity n to support rising end demand. If FOCI's capacity expansion pace or yield rate is lower than expected, it would pose downside risks to our forecasts for FOCI's shipment and revenue growth.

FOCI is an optical component supplier expanding from telecom to AIDC, co-designing and providing high-speed FAU for global-leading CPO switch players. We are positive on FOCI's earnings growth going forward, driven by (1) business expansion from optical components for telecom operators to FAU ( fi ber array unit) used in CPO switches, (2) increasing CPO switch shipments globally, (3) collaboration with global-leading CPO switch players in FAU design and manufacturing, (4) fully-automated FAU packaging technology supporting manufacturing e ffi ciency and driving yield rates, (5) pro fi tability improvement driven by the rising contribution from CPO FAU, (6) product migration toward higher-speed FAU (e.g., from 3.2T to 6.4T), and (7) capacity expansion in the coming years. We are Buy-rated on FOCI.

Valuation: Our 12-month target price of NT$864 is based on a 15.9x 2030E P/E, discounted back to 2027E at a COE of 12.6%. Our target multiple is derived from peers' correlation between forward-year trading P/E and earnings growth.

Key downside risks: Fiercer-than-expected market competition, technology migration trends in optical networking, and slower-than-expected capacity ramp-up.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM