PDF 原檔:報告_Daiwa_順德2351_20260709_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_順德2351_20260709_001.png |

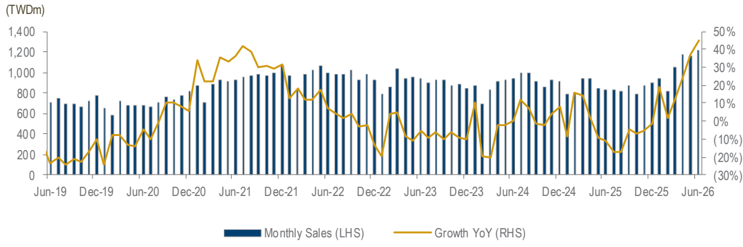

57.2KB | 真資料圖 | 順德合併月營收長條圖疊 YoY 成長率折線圖(Jun-19 至 Jun-26),2026 年中月營收與 YoY 皆創圖表區間新高(月營收逾 NT$1,200m、YoY 逾 40%) |

原始內容

SDI Corp (2351 TT)

Share price (9 Jul): TWD200.00

12-mth rating: Buy (1)

Record-high 2Q26 revenue beat expectations

Helen Chien

(886) 2 8758 6254

helen.chien@daiwacm-cathay.com.tw

Neil Teng

(886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Summary: SDI reported June 2026 revenue of TWD1,214m (+5.0% MoM and +45.1% YoY; +23.3% YoY for 6M26), a record-high, after market hours on 9 July 2026. Its 2Q26 revenue, also a record-high, accounted for 103.6% and 115.4% of our estimate and the Bloomberg consensus forecasts of 2Q26 revenue, respectively.

We have a Buy (1) rating on SDI with a 12-month TP of TWD265, based on a PER of 39x on our 1-year-forward EPS forecast. For more information on the company, please refer to our latest flash, Stronger-than-expected order visibility , on 27 May.

What's the impact

- Record-high 2Q26 revenue beat expectations. SDI reported June 2026 revenue of TWD1,214m (+5.0% MoM and +45.1% YoY; +23.3% YoY for 6M26), a record-high. Its 2Q26 revenue (TWD3,545m, +26.4% QoQ and +36.6% YoY), also a record-high, accounted for 103.6% and 115.4% of our (TWD3,421m, +22.0% QoQ and +31.9% YoY) and the Bloomberg consensus forecasts of 2Q26 revenue, respectively. We attribute the stronger-than-expected growth to the price hike effect and rush orders.

SDI: consolidated monthly sales

Source: Company

- Brighter-than-expected lead frame outlook; rising revenue contribution from AI lead frame and heat spreader. The company expects its 2H26 revenue to grow by 5-10% HoH. SDI's utilisation rate is high at its plants in China (from auto demand with contribution from new products) and Taiwan (from AI, auto, and industrial demand for IDM and OSAT clients). Its AI lead frame accounted for 6% of revenue in 1Q26, and management targets to reach double-digit revenue contribution by 4Q26. SDI highlights that it has received many rush orders for AI lead frames, and 50-60 new AI-related products are expected to be launched in 2H26. SDI is planning another price hike for 2H26.

What we recommend

We have a Buy (1) rating on SDI with a 12-month TP of TWD265, based on a PER of 39x on our 1-year-forward EPS forecast. The stock is currently trading at PERs of 35.5x/26.4x, based on our 2026/27E EPS, at the lower end of its past-5-year range of 13-73x [average PER: 29x]). Key downside risks: worse-than-expected end demand; worse-than-expected gross-margin expansion.

In the interests of timeliness, this document has not been edited.

9 July 2026

Information Technology: Taiwan