PDF 原檔:報告_Daiwa_長廣7795_20260626_original.pdf

原始內容

Taiwan

Eternal Precision Mechanics (7795 TT)

Eternal Precision Mechanics

Target price:

TWD600.00

Share price (26 Jun): TWD460.50 | Up/downside: +30.3%

Initiation: a hidden gem in the ABF upcycle

- Dominant vacuum laminator supplier riding the substrate upcycle

- Price hikes and capacity expansion amid tight supply

- Initiating coverage with a Buy (1) rating and 12M TP of TWD600

Investment case: We initiate coverage of Eternal Precision Mechanics (Eternal), the leading global manufacturer of vacuum lamination equipment for ABF substrates, with a Buy (1) rating. Eternal holds a dominant c.95% share in the high-end vacuum laminator market, and direct exposure to the ABF (Ajinomoto build-up film) substrate industry ongoing expansion cycle.

ABF upcycle boosts high-end laminator demand. We forecast ABF substrate demand to exceed industry supply by 19%/20% in 2027-28E, supporting aggressive capacity expansion among substrate makers. Given Eternal's strong correlation with industry capex and increasing demand for high-end equipment driven by AI chip complexity, we forecast a revenue CAGR of 96% in 2026-28E, with the 90-tonne laminator revenue contribution to increase from c.10% in 2025 to c.70% by 2028E.

Market leader entering a new growth cycle. Eternal's decades-long partnership with Ajinomoto (2802 JP, JPY5,721, Outperform [2]; covered by Japan analyst Shun Igarashi) has helped it secure a c.95% global share in high-end vacuum laminators. With order visibility extending into 2028 and lengthening lead times, capacity in Eternal's Japan plant is set to expand by 26% YoY in 2027E. Combined with the recent price increases, we expect increasing revenue growth visibility from 3Q26 onwards.

Expanding beyond substrates. Eternal is expanding into next-generation packaging applications, including panel-level packaging (PLP), glass core substrates (GCS), and wafer-level packaging. These opportunities could gradually diversify the company's end-market exposure while reducing reliance on the substrate industry. Given the significantly higher ASPs and margins associated with semiconductor-grade equipment, successful penetration into advanced packaging applications could further enhance the company's product mix and long-term growth trajectory.

Catalysts: 1) Revenue inflection in 3Q26 as orders convert to sales; 2) widening ABF substrate supply-demand gap driving substrate makers' capex; 3) high-end laminator mix expansion boosting margins.

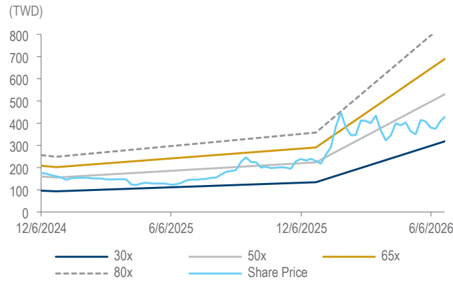

Valuation: We initiate coverage on Eternal with a Buy (1) rating and 12month TP of TWD600, based on a target PER of 40x (vs. its historical 3year trading range of 30-80x), applied to our 1-year forward EPS. We believe valuation is attractive with growing ABF substrate consumption, and Eternal's competitive edge. Based on our 2026-28E EPS CAGR of 126%, our valuation implies a PEG of only 0.3x, which we view as undemanding.

Risks: 1) Slower-than-expected substrate capex growth; 2) market share loss; 3) slower commercialisation of PLP and GCS applications.

26 June 2026

Daiwa

5

2

1

Buy

Stacy Lin

Stacy Lin (886) 2 8758 6252 stacy.lin@daiwacm-cathay.com.tw

Leon Chen (886) 2 8758 6247 leon.chen@daiwacm-cathay.com.tw

Share price performance

| 12-month range | 12-month range | 142.00-460.50 |

|---|---|---|

| Market cap (USDbn) | Market cap (USDbn) | 1.11 |

| 3m avg daily turnover (USDm) | 3m avg daily turnover (USDm) | 7.21 |

| Shares outstanding (m) | Shares outstanding (m) | 77 |

| Major shareholder | Eternal Materials Co Ltd | (61.7%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 3,045 | 9,150 | 11,659 |

| Operating profit (m) | 649 | 2,617 | 3,500 |

| Net profit (m) | 343 | 1,307 | 1,745 |

| Core EPS (fully-diluted) | 4.473 | 17.053 | 22.759 |

| EPS change (%) | 44.0 | 281.3 | 33.5 |

| Daiwa vs Cons. EPS (%) | n.a. | n.a. | n.a. |

| PER (x) | 103.0 | 27.0 | 20.2 |

| Dividend yield (%) | 0.7 | 2.6 | 3.5 |

| DPS | 3.1 | 11.9 | 15.9 |

| PBR (x) | 12.1 | 8.8 | 7.4 |

| EV/EBITDA (x) | 46.6 | 12.6 | 9.5 |

| ROE (%) | 15.0 | 36.7 | 38.5 |

Source: FactSet, Daiwa forecasts

Table of contents

| Vacuum laminator market analysis ..........................................................................6 | |

|---|---|

| Accelerating substrate capex amid widening supply-demand gap ......................................6 | |

| Chip complexity drives high-end equipment demand | ........................................................11 |

| Competitive landscape ............................................................................................14 | |

| Competitive advantages underpin market leadership........................................................14 | |

| Capacity expansion and price hikes ..................................................................................15 | |

| Future opportunities ................................................................................................17 | |

| From wafer to panel, from liquid to dry films ......................................................................17 | |

| From organic to glass ........................................................................................................19 | |

| Financial analysis.....................................................................................................21 | |

| Revenue CAGR of 96% over 2026-28E | ............................................................................21 |

| Margin expansion underway..............................................................................................22 | |

| Balance sheet and cash flow .............................................................................................22 | |

| Valuation and risks ..................................................................................................23 | |

| Initiating with a Buy (1) rating and a 12M TP of TWD600..................................................23 | |

| Risks to our call..................................................................................................................24 | |

| Company profile.......................................................................................................25 | |

| Company background........................................................................................................25 | |

| Shareholder structure | ........................................................................................................25 |

| Glossary of terms.....................................................................................................26 | |

| ESG analysis.............................................................................................................27 |

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

valuation

5

Daiwa

4

Growth outlook

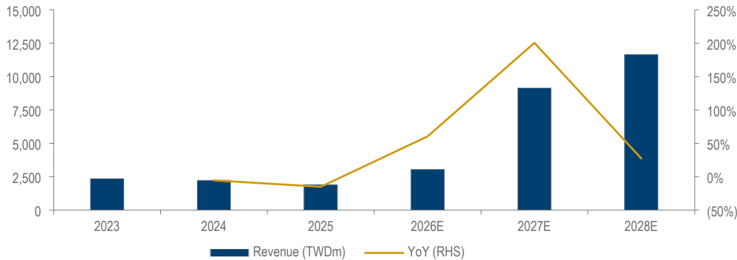

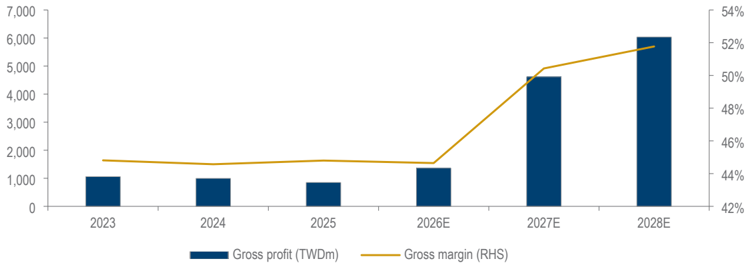

We expect Eternal's 2026-28E revenue growth to be driven primarily by rising substrate industry capex amid a widening ABF supply-demand gap, as well as increasing demand of high-end vacuum laminators. On the margin side, the growing contribution from high-end 90-tonne laminators, which carry higher ASPs than conventional products, is expected to drive a favourable product mix shift. As a result, we expect revenue to grow 60%/200%/27% YoY in 2026-28E, respectively, and gross margin to reach 52% in 2028E from 45% in 2025.

Valuation

We initiate coverage on Eternal with a Buy (1) rating and 12-month TP of TWD600, based on a target PER of 40x (vs. its historical 3-year trading range of 30-80x), applied to our 1-year forward EPS (ie, 4Q26-3Q27E). We believe the valuation is attractive with growing ABF substrate consumption, and Eternal's competitive edge. Based on our 2026-28E earnings CAGR of 126%, our target valuation implies a PEG of only 0.3x, which we view as undemanding.

Earnings revisions

Eternal currently has limited sell-side coverage, with no meaningful Bloomberg consensus available. We believe our estimates appropriately capture the ongoing substrate capex upcycle, improving order momentum, and the favourable product mix shift toward high-end equipment.

Eternal: revenue and gross margin outlook

Source: Company, Daiwa forecasts

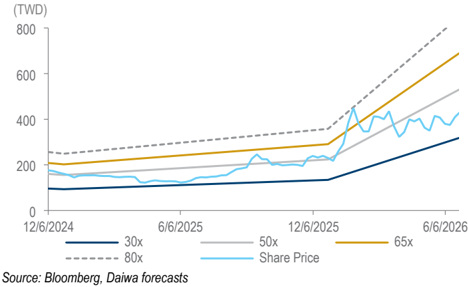

Eternal: 1-year-forward PER bands

Source: Bloomberg, Daiwa forecasts

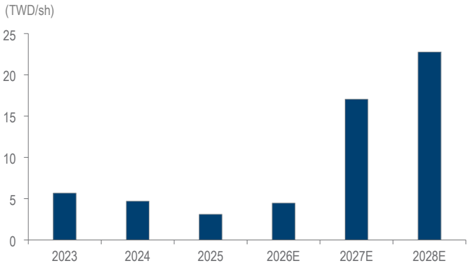

Eternal: EPS outlook

Source: Company, Daiwa forecasts

3

2

1

Eternal Precision Mechanics (7795 TT): 26 June 2026

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| JP plant avg. monthly capacity (units) | n.a. | n.a. | 18 | 18 | 18 | 19 | 24 | 26 |

| CH plant avg. monthly capacity (units) | n.a. | n.a. | 4 | 4 | 4 | 4 | 5 | 6 |

| Annual total shipment (units) | n.a. | n.a. | 150 | 134 | 99 | 160 | 321 | 366 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Low/Mid End Laminator | n.a. | n.a. | 1,074 | 833 | 609 | 972 | 1,678 | 1,734 |

| High End Laminator | n.a. | n.a. | 873 | 1,092 | 875 | 1,618 | 6,975 | 9,378 |

| Other Revenue | n.a. | n.a. | 414 | 309 | 414 | 455 | 497 | 546 |

| Total Revenue | n.a. | n.a. | 2,361 | 2,234 | 1,898 | 3,045 | 9,150 | 11,659 |

| Other income | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | n.a. | n.a. | (1,303) | (1,238) | (1,048) | (1,686) | (4,536) | (5,623) |

| SG&A | n.a. | n.a. | (478) | (408) | (423) | (677) | (1,901) | (2,421) |

| Other op.expenses | n.a. | n.a. | (31) | (12) | (18) | (33) | (96) | (116) |

| Operating profit | n.a. | n.a. | 558 | 564 | 409 | 649 | 2,617 | 3,500 |

| Net-interest inc./(exp.) | n.a. | n.a. | (15) | (10) | (9) | (10) | (13) | (20) |

| Assoc/forex/extraord./others | n.a. | n.a. | 7 | 6 | 16 | 9 | 10 | 9 |

| Pre-tax profit | n.a. | n.a. | 550 | 560 | 416 | 648 | 2,614 | 3,489 |

| Tax | n.a. | n.a. | (254) | (261) | (196) | (305) | (1,307) | (1,745) |

| Min. int./pref. div./others | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | n.a. | n.a. | 296 | 299 | 220 | 343 | 1,307 | 1,745 |

| Net profit (adjusted) | n.a. | n.a. | 296 | 299 | 220 | 343 | 1,307 | 1,745 |

| EPS (reported)(TWD) | n.a. | n.a. | 5.664 | 4.218 | 3.106 | 4.473 | 17.053 | 22.759 |

| EPS (adjusted)(TWD) | n.a. | n.a. | 5.664 | 4.218 | 3.106 | 4.473 | 17.053 | 22.759 |

| EPS (adjusted fully-diluted)(TWD) | n.a. | n.a. | 5.664 | 4.218 | 3.106 | 4.473 | 17.053 | 22.759 |

| DPS (TWD) | n.a. | n.a. | 2.500 | 3.000 | 2.150 | 3.131 | 11.937 | 15.932 |

| EBIT | n.a. | n.a. | 558 | 564 | 409 | 649 | 2,617 | 3,500 |

| EBITDA | n.a. | n.a. | 633 | 639 | 483 | 722 | 2,727 | 3,620 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | n.a. | n.a. | 550 | 560 | 416 | 648 | 2,614 | 3,489 |

| Depreciation and amortisation | n.a. | n.a. | 76 | 76 | 74 | 73 | 110 | 120 |

| Tax paid | n.a. | n.a. | (254) | (261) | (196) | (305) | (1,307) | (1,745) |

| Change in working capital | n.a. | n.a. | (2,279) | 494 | (163) | (1,023) | (1,194) | (450) |

| Other operational CF items | n.a. | n.a. | 2,536 | (286) | (224) | 99 | (20) | 0 |

| Cash flow from operations | n.a. | n.a. | 628 | 583 | (93) | (508) | 204 | 1,414 |

| Capex | n.a. | n.a. | (30) | (10) | (36) | (29) | (760) | (600) |

| Net (acquisitions)/disposals | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| Other investing CF items | n.a. | n.a. | 135 | 0 | (0) | 4 | 0 | 0 |

| Cash flow from investing | n.a. | n.a. | 105 | (10) | (36) | (25) | (760) | (600) |

| Change in debt | n.a. | n.a. | (154) | (447) | (183) | 153 | 681 | 545 |

| Net share issues/(repurchases) | n.a. | n.a. | 0 | 0 | 0 | 80 | 0 | 0 |

| Dividends paid | n.a. | n.a. | (180) | (154) | (212) | (165) | (240) | (915) |

| Other financing CF items | n.a. | n.a. | 516 | (57) | (62) | 1,457 | 184 | 0 |

| Cash flow from financing | n.a. | n.a. | 182 | (658) | (457) | 1,525 | 624 | (370) |

| Forex effect/others | n.a. | n.a. | (124) | (57) | 0 | (15) | (23) | (21) |

| Change in cash | n.a. | n.a. | 791 | (142) | (586) | 977 | 44 | 423 |

| Free cash flow | n.a. | n.a. | 598 | 573 | (129) | (538) | (556) | 814 |

Source: FactSet, Daiwa forecasts

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | n.a. | n.a. | 1,860 | 1,718 | 1,132 | 2,109 | 2,153 | 2,577 |

| Inventory | n.a. | n.a. | 1,022 | 634 | 566 | 1,768 | 2,828 | 3,185 |

| Accounts receivable | n.a. | n.a. | 446 | 452 | 460 | 1,150 | 2,001 | 2,510 |

| Other current assets | n.a. | n.a. | 146 | 76 | 110 | 92 | 92 | 92 |

| Total current assets | n.a. | n.a. | 3,474 | 2,881 | 2,268 | 5,119 | 7,074 | 8,364 |

| Fixed assets | n.a. | n.a. | 390 | 322 | 314 | 309 | 979 | 1,459 |

| Goodwill & intangibles | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current assets | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| Total assets | n.a. | n.a. | 3,863 | 3,203 | 2,582 | 5,428 | 8,053 | 9,823 |

| Short-term debt | n.a. | n.a. | 258 | 456 | 284 | 438 | 1,119 | 1,664 |

| Accounts payable | n.a. | n.a. | 221 | 146 | 148 | 1,165 | 1,882 | 2,298 |

| Other current liabilities | n.a. | n.a. | 896 | 699 | 268 | 530 | 631 | 631 |

| Total current liabilities | n.a. | n.a. | 1,376 | 1,301 | 700 | 2,134 | 3,631 | 4,592 |

| Long-term debt | n.a. | n.a. | 671 | 0 | 0 | 0 | 0 | 0 |

| Other non-current liabilities | n.a. | n.a. | 316 | 295 | 293 | 299 | 299 | 299 |

| Total liabilities | n.a. | n.a. | 2,363 | 1,596 | 993 | 2,432 | 3,930 | 4,891 |

| Share capital | n.a. | n.a. | 616 | 708 | 708 | 788 | 788 | 788 |

| Reserves/R.E./others | n.a. | n.a. | 885 | 899 | 881 | 2,207 | 3,335 | 4,143 |

| Shareholders' equity | n.a. | n.a. | 1,500 | 1,607 | 1,589 | 2,995 | 4,123 | 4,932 |

| Minority interests | n.a. | n.a. | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | n.a. | n.a. | 3,863 | 3,203 | 2,582 | 5,428 | 8,053 | 9,823 |

| EV | n.a. | n.a. | 34,370 | 34,039 | 34,452 | 33,630 | 34,266 | 34,388 |

| Net debt/(cash) | n.a. | n.a. | (931) | (1,262) | (848) | (1,671) | (1,035) | (913) |

| BVPS (TWD) | n.a. | n.a. | 24.374 | 22.690 | 22.436 | 38.000 | 52.302 | 62.561 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | n.a. | n.a. | n.a. | (5.4) | (15.0) | 60.4 | 200.5 | 27.4 |

| EBITDA (YoY) | n.a. | n.a. | n.a. | 0.9 | (24.4) | 49.5 | 277.7 | 32.7 |

| Operating profit (YoY) | n.a. | n.a. | n.a. | 1.1 | (27.5) | 58.7 | 303.4 | 33.7 |

| Net profit (YoY) | n.a. | n.a. | n.a. | 1.1 | (26.4) | 55.9 | 281.3 | 33.5 |

| Core EPS (fully-diluted) (YoY) | n.a. | n.a. | n.a. | (25.5) | (26.4) | 44.0 | 281.3 | 33.5 |

| Gross-profit margin | n.a. | n.a. | 44.8 | 44.6 | 44.8 | 44.6 | 50.4 | 51.8 |

| EBITDA margin | n.a. | n.a. | 26.8 | 28.6 | 25.5 | 23.7 | 29.8 | 31.0 |

| Operating-profit margin | n.a. | n.a. | 23.6 | 25.2 | 21.5 | 21.3 | 28.6 | 30.0 |

| Net profit margin | n.a. | n.a. | 12.5 | 13.4 | 11.6 | 11.3 | 14.3 | 15.0 |

| ROAE | n.a. | n.a. | 25.0 | 19.2 | 13.8 | 15.0 | 36.7 | 38.5 |

| ROAA | n.a. | n.a. | 8.1 | 8.5 | 7.6 | 8.6 | 19.4 | 19.5 |

| ROCE | n.a. | n.a. | 22.9 | 25.1 | 20.8 | 24.5 | 60.3 | 59.1 |

| ROIC | n.a. | n.a. | 52.6 | 65.8 | 39.9 | 33.3 | 59.3 | 49.2 |

| Net debt to equity | n.a. | n.a. | net cash | net cash | net cash | net cash | net cash | net cash |

| Effective tax rate | n.a. | n.a. | 46.3 | 46.6 | 47.1 | 47.1 | 50.0 | 50.0 |

| Accounts receivable (days) | n.a. | n.a. | n.a. | 73.4 | 87.7 | 96.5 | 62.8 | 70.6 |

| Current ratio (x) | n.a. | n.a. | 2.5 | 2.2 | 3.2 | 2.4 | 1.9 | 1.8 |

| Net interest cover (x) | n.a. | n.a. | 35.9 | 47.9 | 46.5 | 66.8 | 205.8 | 175.5 |

| Net dividend payout | n.a. | n.a. | 44.0 | 63.8 | 69.1 | 70.0 | 70.0 | 70.0 |

| Free cash flow yield | n.a. | n.a. | 1.7 | 1.6 | n.a. | n.a. | n.a. | 2.3 |

Source: FactSet, Daiwa forecasts

Company profile

Eternal was established in 2022 through the spin-off of Eternal Material's equipment division and its subsequent merger with Nikko-Materials, a wholly owned Japanese subsidiary. The company was listed in January 2026 and is the global leader in IC substrate vacuum laminators, serving all major substrate manufacturers worldwide.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Key vacuum laminator supplier to global ABF substrate makers

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Vacuum laminator market analysis

Accelerating substrate capex amid widening supplydemand gap

Eternal Precision Mechanics (Eternal) is the dominant global supplier of high-end vacuum laminators, commanding c.95% market share. Eternal supplies most of the global major ABF substrate manufacturers, including Ibiden (4062 JP, JPY24,000, Outperform [2]; covered by Daiwa analyst Takumi Sado), Shinko (private; delisted in June 2025), Unimicron (3037 TT, TWD975, Buy [1]; covered by Daiwa analyst Sheng Cheng), Kinsus (3189 TT, TWD797, Buy [1]; covered by Daiwa analyst Sheng Cheng), NYPCB (8046 TT, TWD1,125, Buy [1]; covered by Daiwa analyst Sheng Cheng), and SEMCO (009150 KS, KRW1,993,000, Buy [1]; covered by Daiwa analyst SK Kim), among others.

Vacuum laminators play a critical role in ABF substrate production, eliminating air bubbles and wrinkles generated during the lamination of ABF build-up films, ensuring complete material filling and lamination integrity. Given that ABF substrates represent the largest and most mature end-application for vacuum laminators, Eternal's revenue growth has exhibited a strong correlation with the capex growth of global substrate manufacturers.

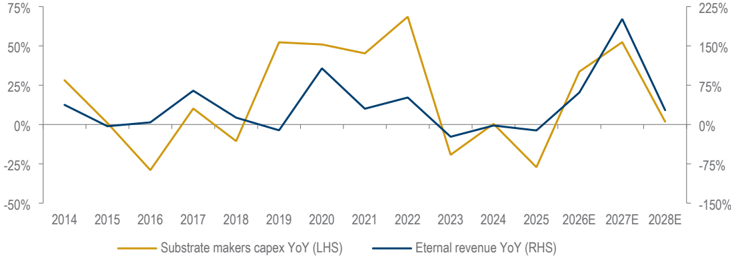

Correlation between Eternal's revenue and global substrate makers' capex growth

Source: Bloomberg, Companies, Daiwa forecasts Note: Total capex includes Unimicron, Kinsus, NYPCB, Ibiden, Shinko, Toppan, Semco, AT&S

ABF demand analysis

AI GPU & ASIC

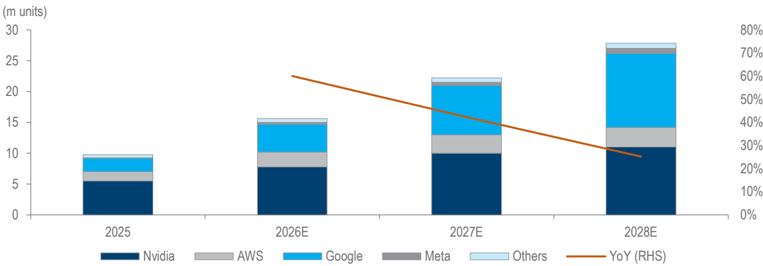

Thanks to the expansion of AI workloads and continued growth in cloud AI capex, we expect GPU and ASIC shipments to remain on an upward trajectory. We forecast AI chip shipments to increase by 42%/25% YoY in 2027-28E.

AI chip shipment forecasts

Source: Companies, Daiwa forecasts

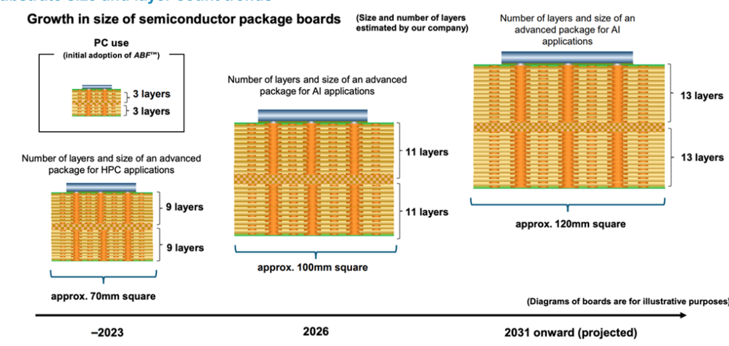

Substrate size and layer count trends

(Size and number of layers estimated by our company)

(initial adoption of ABF'™)

Number of layers and size of an advanced package for Al applications

-11 layers

Since ABF was first adopted for PC applications in 1999, with AI workloads driving increasing compute core counts and HBM integration, semiconductor package substrates have become increasingly larger. According to Ajinomoto (2802 JP, JPY5,721, Outperform [2]; covered by Daiwa Analyst Shun Igarashi), from 2031 onward, substrates are expected to further increase from their current sizes.

Substrate size and layer count trends

2026

Source: Ajinomoto

As AI and HPC (high performance computing) continue to adopt chiplet architectures and HBM (High Bandwidth Memory) integration, a single package increasingly incorporates CPUs, GPUs, I/O dies, ASIC chiplets, and multiple HBM stacks, driving larger ABF substrate sizes. At the same time, growing requirements for signal routing and power delivery are leading to higher substrate layer counts. Coupled with the rising complexity of advanced chip manufacturing and lower initial yields during ramp-up, we expect ABF substrate consumption to increase further going forward.

AI chip substrate specs

| Chip | Dimension (mm) | Layer count | |

|---|---|---|---|

| Nvidia | Hopper Blackwell Rubin Rubin Ultra | 5855 8175 9885 15377.5 | 12 14 18 18 |

| AMD | MI350 | 75.4*72 | 18 |

| Intel | Gaudi 3 | 79*71 | TBD |

| Ghostfish | ~80*80 | 16 | |

| Sunfish Zebrafish Humufish | 87.577.5 7075 TBD | 18 24 24 | |

| AWS | Trainium 2 Trainium 3 | 87.5*72.5 | 16 |

| 87.5*72.5 | |||

| 20 | |||

| Microsoft | Maia 100 | 70*70 | 18 |

Source: Companies, Daiwa

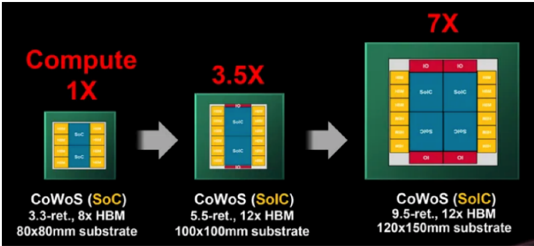

TSMC's (2330 TT, TWD2,340, Buy [1]; covered by Daiwa analyst Rick Hsu) packaging roadmap also points to a continued expansion in the silicon interposer size used in CoWoS. During its 2026 North America Technology Symposium, TSMC indicated that it is currently producing 5.5-reticle-size CoWoS and plans to introduce 14-reticle-size CoWoS by 2028. This would enable the integration of 10 compute dies and 20 HBM stacks, further increasing overall package size and driving additional ABF substrate content per package.

- 3 layers

} 3 layers

Number of layers and size of an advanced package for HPC applications

L 9 layers

9 layers approx. 70mm square

-2023

Source: Alinomoto

Increasing packaging complexity drives larger, higher-layer ABF substrates and rising consumption

Number of layers and size of an

Eternal Precision Mechanics (7795 TT): 26 June 2026

advanced package for Al

13 layers

B8240

Daiwa

16

Compute

1X

CoWoS (SoC)

3.3-ret., 8x HBM

3.5X

CoWos (SolC)

5.5-ret., 12x HBM

80x80mm substrate

100x100mm substrate

AI inference and agent applications drive sustained CPU demand growth

7X

1ю

SeiC

DIOs

DIOS

TSMC: packaging technology roadmap

9.5-ret., 12x HBM

120x150mm substrate

Source: TSMC

CPU

During the initial stages of the AI infrastructure deployment, investment was primarily concentrated on LLM training workloads, driving significant spending on AI servers and crowding out enterprise and cloud customers' budgets for general-purpose servers.

As AI agent applications have been gaining traction and AI services evolving since 2H25, the industry's focus has been shifting from training to inference and real-world deployment, resulting in a meaningful resurgence in CPU demand. While AI accelerators remain the primary compute engine, CPUs play a critical role in data inference, task orchestration, and system management, making them an indispensable component of AI infrastructure.

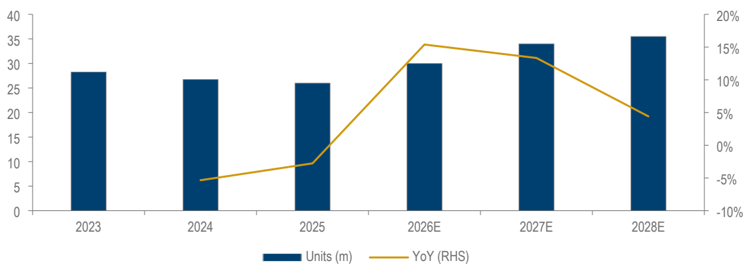

Major chip vendors have recently highlighted AI inference and agent-based applications as key drivers of future CPU demand. We forecast global server CPU shipments to grow by 13%/4% YoY in 2027-28E.

- AMD raised its server CPU TAM CAGR forecast over the next 3-5 years from previously 18% to >35%.

- Intel expects industry-wide server CPU unit shipments to deliver strong double-digit growth with momentum extending into 2027.

- NVIDIA noted that its Vera CPU platform opens up a new USD200bn market opportunity.

- Arm estimates that data centres will rise to four times today's CPU capacity, creating a server CPU market opportunity exceeding USD100bn by 2030.

Server CPU shipment forecasts

Source: IDC, Daiwa forecasts

In terms of substrate specifications, current mainstream server CPUs already utilise highend ABF substrates. Intel's Eagle Stream platform adopts a 78×57mm substrate with 22 layers, while AMD's Genoa platform uses a 75×72mm substrate with 20 layers.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

CPU substrate upgrades drive increased high-end ABF demand

Customer-funded purchases and tight supply indicates higher capex growth

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Based on CPU socket roadmaps, we expect Intel's next-generation Birch Stream to increase substrate size by c.60% versus Eagle Stream, followed by a further 24% increase in Oak Stream. On the AMD side, we expect Venice to reach a 15-20% penetration by the end of 2026, with substrate size also projected to increase by c.24% compared with the current generation.

Beyond Intel and AMD, hyperscalers are deploying in-house data centre CPUs which also adopt high-end ABF substrates with larger package sizes and higher layer counts. Overall, the trend of server CPU specification upgrades is intact, which we expect to drive substantial value growth and capacity consumption in the substrate industry.

Data centre CPU substrate specs

| Chip | Dimension (mm) | Layer count | |

|---|---|---|---|

| Nvidia | Grace Vera | 68*73 | 14 |

| AWS | Graviton 3 | 7675 7275.4 | 18 20 |

| Microsoft | Cobalt | 75*75 | 18 |

Source: Companies, Daiwa

ABF supply analysis

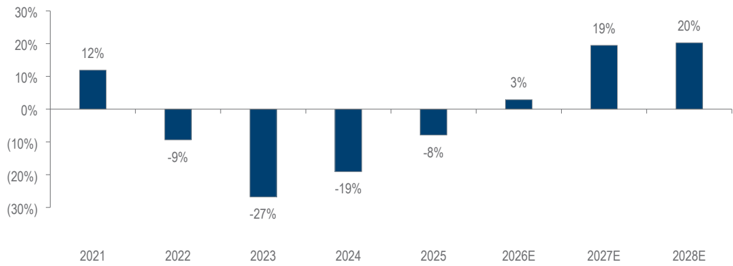

Global substrate manufacturers have accelerated capex this year, marking a transition from the industry's previous oversupply environment into a new capacity expansion cycle. We forecast global substrate industry capacity to increase by 17-18% YoY in 2026-28E. However, driven by the strong growth in AI chip shipments and ongoing substrate specification upgrades, we forecast ABF substrate demand to increase by 30%/37%/19% in 2026-28E, implying demand to outpace supply by 3%/19%/20%.

ABF substrate supply-demand gap

Source: Daiwa estimates and forecasts

Notes: Positive values indicate demand exceeds supply (shortage); negative values indicate supply exceeds demand (oversupply)

Industry leader Ibiden has also highlighted demand for AI server IC substrates continues to exceed existing capacity and expects overall SAP (semi-additive process) demand to exceed industry supply as substrate sizes and layer counts continue to increase.

In addition, compared with the previous ABF upcycle, where customers primarily secured capacity through LTAs (long-term agreements) and prepayments, some customers are now funding equipment purchases. This model not only reduces substrate makers' capital requirements and depreciation burden, but also lowers the risk of idle capacity should future demand fall short of expectations. As a result, it enhances substrate suppliers' willingness to expand capacity and accelerates the output of high-end ABF substrate.

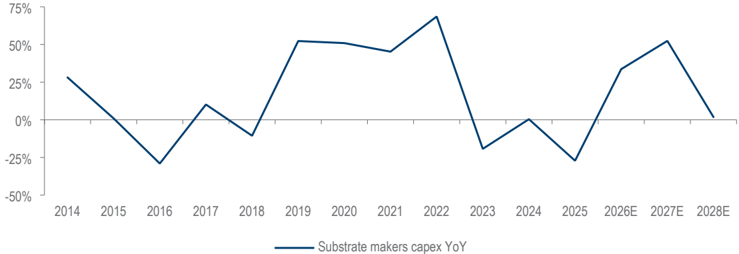

According to Bloomberg estimates, the global substrate makers' capex is expected to grow 34%/52%/2% in 2026-28E. We believe actual investment growth could be even higher after incorporating customer-funded equipment purchases, which are not reflected in the chart below. With no meaningful narrowing of the supply-demand gap, substrate manufacturers are likely to maintain an aggressive expansion strategy over our forecast horizon, creating room for further upside to capex revisions.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Global: substrate makers' capex growth

Source: Companies, Bloomberg

Note: Total capex includes Unimicron, Kinsus, NYPCB, Ibiden, Shinko, Toppan, Semco, and AT&S. Customer-funded equipment purchases are not included.

As the dominant supplier of high-end vacuum laminators, Eternal stands as one of the most direct beneficiaries of the capex megatrend, supported by strengthening equipment shipment momentum, improving order visibility, and sustained long-term growth prospects.

Daiwa

tion and planarisation and planarisation

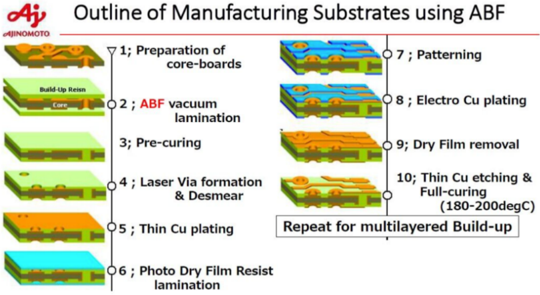

Aj

AJINOMOTO

Build-Up Reisn

Core

‹ko-materials core-boards

02; ABF vacuum lamination

3; Pre-curing

04; Laser Via formation

& Desmear

95; Thin Cu plating

06; Photo Dry Film Resist

Vacuum laminators are critical equipment for high-precision ABF substrate lamination

0 7; Patterning

0 8; Electro Cu plating

Chip complexity drives high-end equipment demand

ABF lamination process

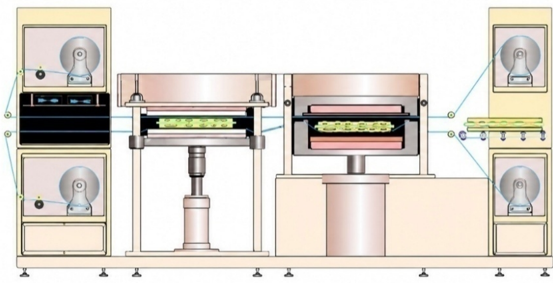

The vacuum laminator utilises a vacuum environment together with precise pressure and temperature control to laminate thin-film materials onto substrates with high accuracy. The process consists of four key steps:

- Pre-lamination: The film is positioned on both sides of the substrate without pressure.

- Vacuum lamination: Air is evacuated from the vacuum chamber before the heated platen rises to form a sealed environment. Pressure and heat are then applied through a diaphragm system, enabling intimate bonding between the film and substrate while preventing void formation.

- Micron-level planarisation: The substrate subsequently enters the planarisation stage, where higher pressure is applied to achieve superior flatness. Vertical positioning is precisely controlled by servo motors to suppress resin bleed-out and ensure thickness uniformity.

- Cooling and curing: The laminated substrate is cooled through a dedicated cooling system, allowing the film-to-substrate interface to cure and stabilise.

Lamination and planarisation

Source: Nikko-materials

Vacuum lamination is primarily used at the initial stage of the build-up process, where ABF build-up films are laminated onto the surface of the core board. Subsequent processes include laser drilling, copper plating, and circuit pattern formation. As ABF substrates require multiple build-up cycles to achieve high-layer-count structures, the vacuum lamination process must be repeated numerous times throughout production. As a result, lamination quality and yield control are critical determinants of overall substrate manufacturing performance.

Lamination and planarisation

Source: Ajinomoto

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

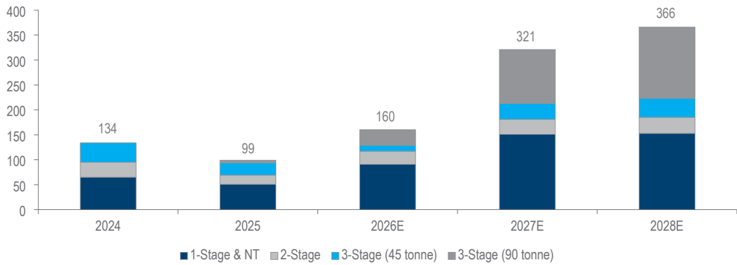

90-tonne laminators to overtake 45-ton in 2026 shipments and revenue mix

Laminator types

Vacuum laminator accounts c.90% of Eternal's revenue. Based on technical specifications, vacuum capabilities, and the substrate layer counts they support, the company's products can be categorised as follows:

- Single-stage laminators: Primarily used in PCB and LED applications without vacuum technology. Single-stage laminators are mainly applied in dry-film photoresist, solder mask dry-film, and protective film attachment processes.

- Two-stage laminators: Targeted at low- to mid-end ABF substrates with 4-8 layers. Two-stage laminators incorporate vacuum lamination technology to eliminate air bubbles and improve production yields.

3. Three-stage laminators:

Tonnage refers to the maximum lamination pressure applied by the laminator during the vacuum lamination process.

- 45-tonne models: Essential to produce ABF substrates with 10-20+ layers, featuring micron-level planarization capabilities, enabling precise control of resin bleed-out and substrate flatness.

- 90-ton tonne: Developed specifically for Ajinomoto's next-generation build-up film material, GL107, and primarily used in high-end AI chips. Due to the material's lower flowability, controlling void formation during lamination becomes significantly more challenging. As a result, lamination pressure must be increased to 90 tonnes to maintain high post-lamination flatness while avoiding excessive heating that could degrade material properties.

With server CPU and AI substrates now requiring 16-20+ layers, production increasingly relies on three-stage vacuum laminators. We forecast Eternal's shipments of three-stage laminators to grow by 43%/226%/29% YoY in 2026-28E. Meanwhile, we expect demand for mid-end equipment to be supported by capacity expansion among Chinese PCB manufacturers, with shipment YoY growth of 44%/15%/7% in 2026-28E.

Within the three-stage product portfolio, Eternal offers two models. In 2022, the company began developing a 90-tonne three-stage vacuum laminator specifically designed for Ajinomoto's next-generation low-Dk, low-CTE build-up film materials. Initial shipments commenced in 2H25 to leading substrate manufacturers for installation and qualification, with related revenue recognised in 4Q25.

As tier-one customers continue to increase orders and tier-two customers actively ramp procurement, we expect 90-tonne laminators to surpass 45-tonne models in both shipment volume and revenue contribution in 2026E. In addition, emerging packaging technologies such as embedded substrates, panel-level packaging (PLP), and glass core substrates (GCS) are increasing manufacturing complexity, further driving demand for high-end equipment. As a result, we forecast 90-tonne laminator shipments to grow by 248%/32% YoY in 2027-28E, respectively.

Eternal: shipment trends (units)

Source: Company, Daiwa forecasts

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Complexity, material upgrades, and higher layer counts are driving a shift to high-end laminators

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

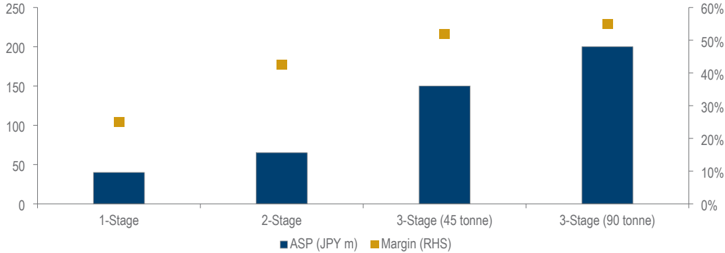

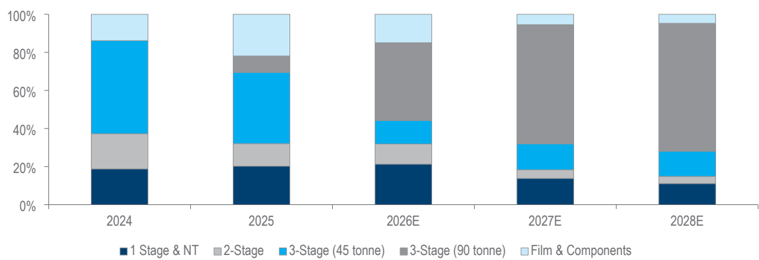

The ASP of a three-stage 90-tonne laminator is c.5 times that of a single-stage laminator. From a profitability perspective, gross margins for single-stage laminators are generally below 30%, compared with 50-55% for three-stage laminators. Supported by 1) rising substrate layer counts for advanced semiconductors, 2) increasing adoption of nextgeneration materials requiring higher lamination pressure, and 3) growing packaging complexity, Eternal's product mix is expected to continue shifting toward high-end laminators. Three-stage equipment accounted for c.45% of revenue in 2025, and we expect this contribution to increase steadily, reaching 80% by 2028E.

Eternal: ASP and gross margin comparison

Source: Company, Daiwa forecasts

Eternal: product mix trend

Source: Company, Daiwa forecasts

Deep ABF expertise via Ajinomoto partnership underpins c.95% laminator market dominance

Eternal Precision Mechanics (7795 TT): 26 June 2026

Competitive landscape

Competitive advantages underpin market leadership

Through its long-standing collaboration with Ajinomoto in developing ABF lamination equipment, Eternal has established the industry's deepest understanding of build-up film materials, securing c.95% global market share in the high-end vacuum laminator segment.

Ajinomoto partnership

Eternal holds a c.95% global market share in the mid- to high-end vacuum laminator market, attributable to its long-standing relationship with Ajinomoto. In 1997, Ajinomoto partnered with Nichigo Morton, Eternal's predecessor, to jointly develop the first vacuum laminator designed for ABF substrate production.

Ajinomoto's build-up film holds c.95% global share in the ABF substrate industry and accounts for c.100% of high-end AI GPU and ASIC applications per our supply chain check. Through decades of accumulated material know-how, extensive patent protection, and deep customer qualification relationships, Ajinomoto has established a highly defensible competitive position.

Given the close linkage between ABF material characteristics and vacuum laminator design parameters, Eternal has benefited from its first-mover advantage as a codevelopment partner and more than two decades of collaboration with Ajinomoto. As long as Ajinomoto maintains its dominant position in the ABF market, we believe Eternal will continue to preserve its leadership in the mid- to high-end vacuum laminator segment.

Industry-leading yields

ABF substrates require multiple build-up cycles to achieve high-layer-count structures, making vacuum lamination a repeatedly executed process throughout production. According to the company, Eternal's equipment delivers a single-pass lamination yield of up to 98.5%, allowing overall yields to remain above 86% even after multiple lamination cycles, outperforming industry averages.

The superior yield performance is primarily attributable to 1) Eternal having decades of expertise and proprietary databases covering material characteristics, temperature profiles, and pressure parameters; and 2) each laminator consisting of c.2,000 components, with many critical parts manufactured in-house at its Japanese plant. This vertical integration provides tighter quality control, faster customisation, and deeper process know-how.

Pure-play vacuum laminator supplier

Japanese peers

Eternal's primary competitor in the high-end vacuum laminator market is Meiki Plant, which became part of Japan Steel Works (JSW) (5631 JP, not rated) following its integration in 2020. As a Japanese supplier, JSW enjoys advantages in serving domestic substrate manufacturers. However, given the time and resources required for equipment qualification, customers tend to remain cautious when introducing alternative suppliers. In our view, Eternal maintains competitive advantages in both production capacity and technical expertise within the vacuum lamination niche.

Taiwanese peers

Both C Sun (2467 TT, not rated) and Group Up (6664 TT, not rated) offer vacuum laminator products, primarily targeting lower-end applications in the PCB and display industries. These companies mainly compete with Eternal in China's low- to mid-end market. However, given their broader product portfolios spanning lamination, film attachment, film stripping, baking, and coating equipment, neither company possesses the same degree of specialisation in vacuum lamination technology.

Daiwa

Short-term leases and long-term expansion underpin sustained capacity growth

Eternal Precision Mechanics (7795 TT): 26 June 2026

Capacity expansion and price hikes

As global substrate manufacturers enter a new capacity expansion cycle, Eternal is expanding its own production capacity as well and implementing price increases to offset higher costs. Combined with its order visibility extending into 2028, we believe Eternal is entering a new growth cycle, with the benefits expected to gradually materialise in revenue and earnings beginning in 3Q26.

Capacity expansion

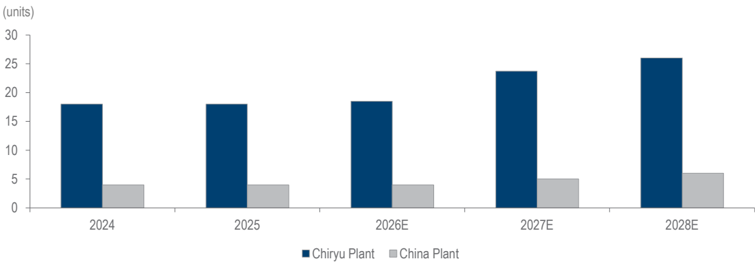

Eternal's manufacturing plants are located in Japan and China, while its Kaohsiung facility in Taiwan is mainly operates in equipment servicing, sales, and installation.

- Japan (Chiryu Plant): Serves as the company's R&D centre and production base for high-end equipment. Current monthly capacity is c.18-19 units.

- China (Guangzhou Plant): Focuses on the assembly of lower-end equipment and serves the domestic Chinese market. Current monthly capacity is c.4 unit.

As global substrate manufacturers continue to increase capex, Eternal's order visibility has already extended through 2028 and even further. The company is currently operating under tight capacity conditions, with normal equipment lead times of 5-6 months having extended to more than 12 months.

To meet strong customer demand, Eternal has leased additional land near its Chiryu plant with expected monthly production capacity in Japan to increase to 20 units in 2H26, per the company. As demand continues to grow, it plans to lease more land for further capacity, which we estimate will lead to annual shipments from Japan to reach 300 units in 2027.

Eternal also plans to establish a new manufacturing facility in Toyota City as a long-term expansion strategy. The company expects the new plant to be 2-3x larger than the existing Chiryu plant and is targeted for completion by the end of 2028, providing substantial room for future capacity expansion.

Eternal: capacity trend

Source: Company, Daiwa forecasts

Daiwa

Price hikes likely to exceed 30% in high-end laminators amid cost pressures, with customers prioritising supply assurance

Revenue lags orders by 6-8 months; growth visibility to improve from 3Q26

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

On the China side, customer demand is growing rapidly, with 2026 shipments expected to be at least double 2025 levels, per the company. Should capacity remain constrained, the company retains flexibility to utilise manufacturing space from its parent company, Eternal Materials, allowing for relatively efficient capacity expansion. In addition, management plans to relocate part of its two-stage laminator assembly operations from Japan to China while outsourcing production of single-stage laminators, further optimising manufacturing efficiency and overall profitability.

Pricing power

Beyond capacity expansion, the company is also implementing price increases to offset rising raw material, labour, and rental costs. Management raised all types of laminator prices in May and expects to implement another round of increases in the near term, with cumulative price hikes likely to exceed 30% in high-end laminators. We believe customers remain receptive to higher pricing for three reasons: 1) rising costs across key inputs and labour expenses; 2) extended lead times, which have increased customers' focus on equipment availability; and 3) delivery schedules rather than pricing alone.

Revenue inflection

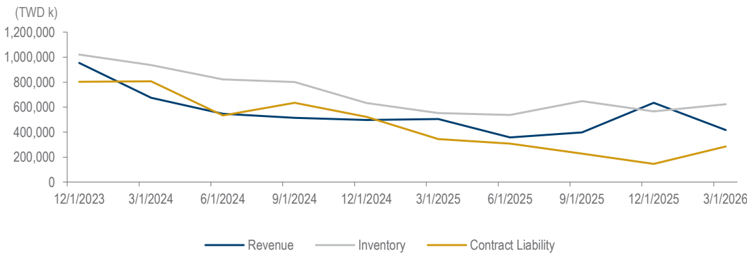

Since the beginning of 2026, major substrate manufacturers have announced new capacity expansion plans and raised capex budgets, driving a gradual improvement in Eternal's order momentum. This recovery is also reflected in the rebound of inventories and contract liabilities in 1Q26.

However, revenue recognition occurs only after equipment is delivered to customer facilities, installed, and formally accepted, at which point 100% of the contract value is recognised. As a result, there is typically a 5-6-month lead time from order placement through material procurement, assembly, and shipment, followed by an additional 1-2 months for installation and customer acceptance. Consequently, revenue realisation generally lags order intake by 6-8 months.

Given the strengthening order momentum in recent months, we expect revenue growth to become more visible from 3Q26 onward, providing a near-term earnings catalyst.

Eternal: inventory and contract liabilities inflected upward in 1Q26

Source: Company

afer-level packaging (WLP) and PLP comparison

Size does matter!

~10% cost decrease

Future opportunities

As semiconductor packaging technologies continue to evolve, advanced packaging applications are placing increasingly stringent requirements on material lamination accuracy, surface flatness, and process yields. As a result, the application scope of vacuum lamination technology is gradually expanding beyond traditional substrate manufacturing into next-generation packaging technologies.

64 interposers

Leveraging its expertise in vacuum process control, pressure uniformity, and large-area lamination, Eternal is well positioned to penetrate these emerging applications. This not only provides additional long-term growth opportunities, but also helps reduce the company's reliance on the substrate industry as its sole growth driver.

From wafer to panel, from liquid to dry films

Why panel-level packaging?

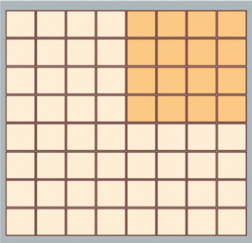

The rapid expansion of package size is exposing the limitations of traditional wafer-level packaging, particularly in terms of wafer utilisation and manufacturing efficiency.

To overcome the size limitations of a single wafer, PLP is emerging as an industry trend. Compared with a 300mm wafer, which can accommodate only 7 interposers with 5.5 reticle size with an area utilisation rate of c.45%, a 300×300mm² panel can accommodate 16 interposers while increasing utilisation to c.81%. Moving to a 600×600mm² panel further increases capacity to 64 interposers per processing cycle. Beyond improved manufacturing efficiency, PLP also offers advantages including greater I/O density, smaller form factors, higher performance, and lower power consumption.

Wafer-level packaging (WLP) and PLP comparison

urce: Yole

Expansion into advanced packaging broadens growth and reduces substrate dependence

7 interposers

Area efficiency ~45%

Source: Yole

In addition, PLP can leverage the existing equipment base and manufacturing infrastructure of the PCB, IC substrate, and LCD industries, significantly lowering adoption barriers and capital investment requirements. According to Yole, compared with conventional 300mm wafer-based processes, a 300×300mm² panel can reduce manufacturing costs by c.10%, while larger 600×600mm² panels can deliver cost savings of c.20%. Driven by growing demand for AI, high-performance computing, and large-scale chiplet integration, we expect PLP to emerge as a key technology platform for nextgeneration advanced packaging from 2027-28 onward.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

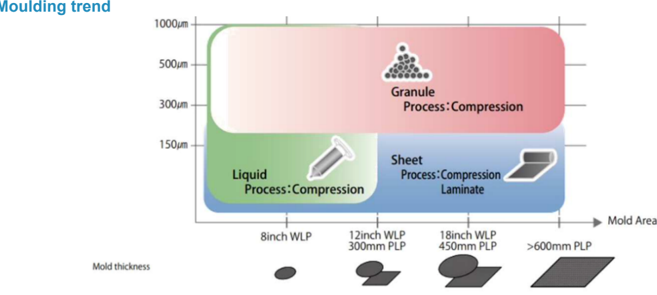

ng trend ternal

1000,m -

500m

300um -

150um

1

Liquid

Process: Compression

Moulding sheets and vacuum lamination mitigate warpage, improving advanced packaging yields

Granule

Process: Compression

Sheet

Vacuum lamination expands into PLP

As advanced packaging continue to migrate toward larger form factors, package warpage has become a critical challenge affecting yields and back-end manufacturing processes. Moulding sheets combined with vacuum lamination can help reduce package stress and improve warpage control.

- Higher manufacturing efficiency and lower cost: Compared with conventional liquid moulding compounds, moulding sheets utilise a dry-film format in combination with vacuum lamination, improving production throughput by 4-5x. In addition, the process eliminates several manufacturing steps, including edge trimming, cleaning, and pre-baking, helping reduce material waste and overall production costs.

- Superior suitability for large-format packaging: As package sizes continue to increase, liquid and powder-based materials are more susceptible to coating nonuniformity, flow marks, and particle contamination. In contrast, moulding sheets provide a fixed material thickness and do not rely on long-distance material flow, enabling better thickness uniformity and material distribution control.

- Improved yield and reliability: Vacuum lamination effectively eliminates voids and wrinkles, achieving c.100% coverage while reducing the risk of damage to highprecision structures such as copper pillars and fine-pitch interconnects.

Together with their advantages in manufacturing efficiency, cost structure, and large-area lamination capability, we believe moulding sheets will become an increasingly important solution for next-generation advanced packaging applications.

Source: Eternal

In addition, with the transitions toward PLP with rectangular panel carriers, manufacturing processes are increasingly converging with those used in PCB and substrate industries, which follow panel-format production. As a result, dry-film materials widely adopted in PCB manufacturing are gradually being introduced into PLP applications. Potential opportunities include temporary carrier bonding films, PID (photo-imageable dielectric) dry films, and dry-film materials used in RDL (Redistribution Layer) photoresist processes.

Eternal's PLP equipment is currently undergoing customer qualification. The company is collaborating with panel manufacturers and OSAT (outsourced semiconductor assembly and test) providers while conducting material evaluations across various panel sizes.

Although PLP still faces technical challenges, current adoption has primarily been concentrated in power management Integrated Circuits (ICs), Radio-Frequency Integrated Circuits (RF ICs), and mobile processors. We expect that continued yield improvements and rapidly increasing package sizes for advanced semiconductors will accelerate adoption in high-performance computing applications.

In line with customers' development roadmaps, we expect Eternal's PLP-related products to begin contributing revenue in the next 2-3 years.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Intel GCS with EMIB nears mass production, validating glass substrate readiness

Eternal Precision Mechanics (7795 TT): 26 June 2026

From organic to glass

Why glass core substrate?

Panel-based packaging is not merely the use of glass panels as temporary carriers for RDL formation and die placement, but the adoption of glass as the substrate core material itself. As conventional organic substrates gradually approach their physical limits, continued increases in package size are exacerbating warpage caused by thermal expansion mismatch, negatively impacting yields, and constraining further scaling of line width and line spacing.

GCS offer three key advantages: 1) enabling finer line width and line spacing to support increasingly demanding high-density interconnect requirements; 2) can accommodate larger package sizes; 3) well suited for advanced packaging and heterogeneous integration, supporting the high bandwidth, high I/O density, and system-level integration requirements of chiplet-based architectures. A comparison between glass core and conventional organic substrates is shown in the table below.

Organic core and glass core substrate comparison

| Organic Core Substrate | Glass Core Substrate | |

|---|---|---|

| Flatness & Warpage | Prone to warpage and dimensional instability, especially at large package sizes | Superior flatness and geometric stability with minimal warpage |

| Interconnect Density | Yield challenges below 2μm L/S for multi-layer RDL | Enables fine L/S, fine pitch, and higher wiring density |

| Form Factor | Package size scaling constrained by warpage | Supports larger body sizes and panel-scale manufacturing |

| Electrical Performance | Higher insertion loss and signal degradation | Lower electrical loss and improved signal integrity |

| Mechanical Properties | Lower stiffness and greater deformation during processing | Higher modulus and stiffness, improving process stability and yield |

Source: Impact 2025, Daiwa

Vacuum lamination extends into GCS

Glass inherently exhibits brittle mechanical properties, and as glass substrates become thinner to support advanced packaging applications, fracture mechanics and edge strength become increasingly critical considerations. In addition, GCS relies on TGVs (throughglass vias) to achieve vertical interconnects, requiring complex manufacturing processes including laser drilling, etching, and metallisation.

As a result, the number of companies capable of providing the required equipment and high-volume manufacturing capabilities remains limited. Compared with organic substrates, GCS currently carries a cost premium of c.2-3x and still faces yield improvement challenges, which remain the primary barriers to large-scale commercialisation.

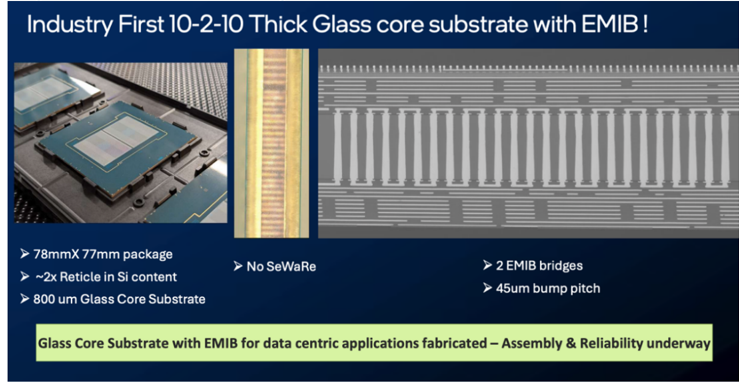

Following its initial announcement in September 2023, Intel reaffirmed its commitment in September 2025 and showcased a GCS package integrated with EMIB (Embedded Multidie Interconnect Bridge) technology at NEPCON Japan in January 2026. The company also highlighted its achievement of "No SeWaRe" (glass cracking) during testing, suggesting that GCS is moving closer to mass production readiness.

TSMC also showcased its latest GCS technology at the JPCA Show 2026. The build-up layers primarily adopt Ajinomoto's GL107 together with the newly developed ABF-GCP (Glass-Cloth Primer), a glass-cloth reinforced dielectric material designed to improve mechanical strength, suppress warpage, and enhance package reliability. Compared with conventional ABF films, ABF-GCP exhibits higher rigidity and lower material flowability, requiring higher lamination pressure to achieve sufficient resin filling and substrate flatness. We believe this material evolution will further increase demand for high-tonnage vacuum laminators, particularly for next-generation AI packaging applications.

Daiwa

Intel: glass core substrate breakthrough

> 78mmX 77mm package

> ~2x Reticle in Si content

> 800 um Glass Core Substrate

Glass Core Substrate with EMIB for data centric applications fabricated - Assembly & Reliability underway

Source Intel

> No SeWaRe

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Other industry leaders including Rapidus (not listed), SK Inc (034730 KS, not rated), major substrate manufacturers such as SEMCO, LG Innotek (011070 KS, KRW931,000, Outperform [2]; covered by Daiwa analyst SK Kim), Unimicron together with their broader supply chains, are actively investing in GCS development.

> 2 EMIB bridges

Intel: glass core substrate breakthrough

Source: Intel

We expect GCS to gradually enter the commercialisation phase after 2028. Eternal delivered its first glass lamination laminator to Intel in 2023, and initial testing results have reportedly been encouraging. As the broader ecosystem, including materials and other supply chain components, continues to mature and yields reach mass-production levels, GCS could become an important long-term growth driver for the company.

Eternal is also working closely with customers to develop and validate wafer-level vacuum laminators. Unlike the company's traditional panel-based products, these laminators require a fundamentally different circular platform architecture, necessitating additional engineering resources and design capabilities. We will continue to monitor the company's development progress in this area.

Semiconductor-grade equipment is expected to command ASPs several times higher than those of substrate equipment, while also offering gross margins above the company's corporate average. Given the flexibility of Eternal's vacuum lamination technology, which can be customised for different materials and process requirements, we believe the company is well positioned to expand beyond its role as a pure substrate equipment supplier and gradually evolve into an advanced packaging equipment provider.

AI-driven capex, improving product mix, and capacity expansion support strong growth through 2028 and beyond

Eternal Precision Mechanics (7795 TT): 26 June 2026

Financial analysis

Revenue CAGR of 96% over 2026-28E

We expect Eternal's revenue to deliver strong growth over 2026-28E, primarily driven by 1) continued increases in substrate industry capex amid a widening ABF supply-demand gap; 2) increasing AI chip complexity driving demand for high-end vacuum laminators; 3) Eternal's ongoing capacity expansion to support rising customer demand; and 4) price increases to reflect higher costs.

Looking beyond 2028, we remain positive on Eternal's long-term growth prospects as its next-generation packaging initiatives gradually begin to contribute to revenue. Successful penetration into semiconductor-related applications would not only provide an additional growth engine, but also further enhance its product mix.

Eternal: revenue trend and forecasts

Source: Company, Daiwa forecasts

Eternal: quarterly and annual P&L statements

| 2026E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2027E | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWD m) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | 2025 | 2026E | 2027E | 2028E |

| Net sales | 418 | 494 | 693 | 1,440 | 1,932 | 2,226 | 2,485 | 2,507 | 1,898 | 3,045 | 9,150 | 11,659 |

| Gross profit | 165 | 200 | 318 | 677 | 950 | 1,121 | 1,270 | 1,274 | 850 | 1,359 | 4,614 | 6,036 |

| Operating costs | 119 | 118 | 156 | 317 | 423 | 486 | 542 | 546 | 441 | 711 | 1,997 | 2,536 |

| Operating profit | 46 | 81 | 161 | 360 | 527 | 635 | 728 | 728 | 409 | 649 | 2,617 | 3,500 |

| Pretax profit | 46 | 79 | 161 | 360 | 527 | 635 | 728 | 725 | 416 | 648 | 2,614 | 3,489 |

| Net profit | 16 | 40 | 89 | 198 | 263 | 317 | 364 | 363 | 220 | 343 | 1,307 | 1,745 |

| EPS (TWD) | 0.21 | 0.52 | 1.16 | 2.59 | 3.44 | 4.14 | 4.75 | 4.73 | 3.11 | 4.47 | 17.05 | 22.76 |

| Operating ratios | ||||||||||||

| Gross margin | 39.4% | 40.5% | 45.8% | 47.0% | 49.1% | 50.4% | 51.1% | 50.8% | 44.8% | 44.6% | 50.4% | 51.8% |

| Operating margin | 11.0% | 16.5% | 23.3% | 25.0% | 27.3% | 28.5% | 29.3% | 29.0% | 21.5% | 21.3% | 28.6% | 30.0% |

| Pre-tax margin | 11.1% | 16.1% | 23.3% | 25.0% | 27.3% | 28.5% | 29.3% | 28.9% | 21.9% | 21.3% | 28.6% | 29.9% |

| Net margin | 3.9% | 8.1% | 12.8% | 13.8% | 13.6% | 14.3% | 14.6% | 14.5% | 11.6% | 11.3% | 14.3% | 15.0% |

| YoY growth | ||||||||||||

| Net revenue | -17% | 38% | 74% | 127% | 363% | 351% | 258% | 74% | -15% | 60% | 200% | 27% |

| Gross profit | -24% | 16% | 97% | 125% | 477% | 461% | 300% | 88% | -15% | 60% | 239% | 31% |

| Operating income | -61% | -7% | 168% | 152% | 1047% | 680% | 351% | 102% | -27% | 59% | 303% | 34% |

| Net income | -74% | -18% | 194% | 152% | 1536% | 699% | 310% | 83% | -26% | 56% | 281% | 33% |

| QoQ growth | ||||||||||||

| Net revenue | -34% | 18% | 40% | 108% | 34% | 15% | 12% | 1% | ||||

| Gross profit | -45% | 21% | 59% | 113% | 40% | 18% | 13% | 0% | ||||

| Operating income | -68% | 77% | 98% | 123% | 46% | 21% | 15% | 0% | ||||

| Net income | -80% | 147% | 123% | 123% | 33% | 21% | 15% | 0% |

Source: Company, Daiwa forecasts

Daiwa

Product mix shift towards high-margin 90-tonne laminators drives gross margin expansion

Eternal Precision Mechanics (7795 TT): 26 June 2026

Margin expansion underway

We expect Eternal's gross margin to improve over 2026-28E, supported by: 1) product mix improvements given that the margin of a 90-tonne laminator is more than 10pp higher than that of a two-stage laminator, and we expect the growing contribution from 90-tonne products to be a key driver of margin expansion; 2) the company implements price increases to pass through higher costs; 3) utilisation rates will likely remain tight as industry demand continues to strengthen.

In addition, the Guangzhou plant, which mainly produces lower-margin single-stage laminators, has historically operated at low utilisation, and generated limited profitability. With order momentum improving meaningfully, we expect the plant to move toward breakeven this year, providing further support for consolidated gross margin expansion.

Eternal: gross margin trend and forecast

Source: Company, Daiwa forecasts

Balance sheet and cash flow

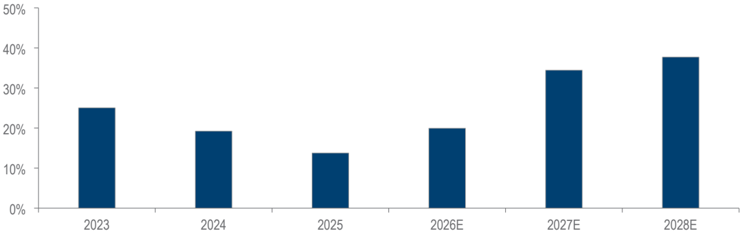

Eternal's ROE declined from 25% in 2023 to 14% in 2025, primarily due to the oversupply conditions in the ABF substrate market, which led substrate manufacturers to adopt a more cautious stance toward capacity expansion and resulted in weak equipment demand. Looking ahead, we expect ROE to recover to 15-39% over 2026-28E, driven by both higher profitability and improved asset turnover.

Eternal: ROE trend and forecasts

Source: Company, Daiwa forecasts

The company completed an equity raise in 1Q26, providing additional funding for future expansion. Looking ahead to 2027-28E, we expect operating cash flow to recover alongside earnings growth, while additional borrowings are likely to be utilised to support the new Toyota plant. We believe with equity proceeds, improving cash generation, and bank financing will provide sufficient funding flexibility to support the company's expansion plans while maintaining a stable dividend payout ratio of c.70% throughout our forecast period.

Daiwa

We initiate coverage of Eternal with a Buy (1) rating, given substrate makers' strong expansion plans and Eternal's dominant position

Eternal Precision Mechanics (7795 TT): 26 June 2026

Valuation and risks

Initiating with a Buy (1) rating and a 12M TP of TWD600

We are positive on Eternal's growth outlook, driven by: 1) Eternal is a key beneficiary of rising substrate industry capex supported by its c.95% market share in the high-end vacuum laminator market; 2) increasing AI chip complexity is driving demand for higherend equipment, supporting a favourable product mix; and 3) capacity expansion to capture order momentum and price increases to pass through higher costs. Following a meaningful improvement in order momentum in recent months, we expect revenue growth to become more visible from 3Q26 onward.

In the long term, the application scope of vacuum lamination technology will likely expand beyond traditional substrate manufacturing into next-generation packaging technologies. Eternal's expansion into semiconductor applications not only provides additional long-term growth opportunities but also reduces its reliance on the substrate industry as the sole driver of growth.

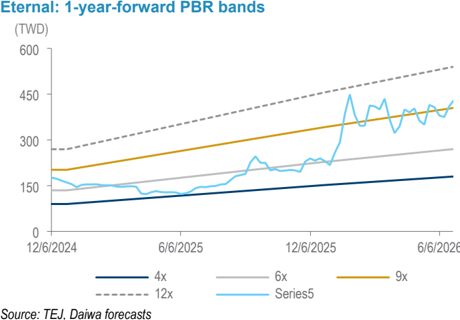

We initiate coverage on Eternal with a Buy (1) rating and a 12-month target price of TWD600, based on a target PER of 40x (vs. its historical 3-year trading range of 30-80x) applied to our 1-year forward EPS forecast (ie, 4Q26-3Q27E). We believe the valuation is justified by the sustained increase in ABF substrate consumption, together with Eternal's unique competitive advantages and favourable industry positioning. Moreover, as we forecast an earnings CAGR of 126% over 2026-28E, our target valuation implies a PEG of only 0.3x, which we view as undemanding given the company's growth prospects.

Eternal: 1-year-forward PER bands

Source: TEJ, Daiwa forecasts

Peer valuation

| Share price | Mkt cap | Daily turnover | EPS CAGR | PER (x) | PER (x) | PER (x) | PBR (x) | PBR (x) | PBR (x) | ROE (%) | ROE (%) | ROE (%) | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Companies | Ticker | Rating | (LC) | (USDm) | (USDm) | 2025-27E | 2025 | 2026E | 2027E | 2025 | 2026E | 2027E | 2025 | 2026E | 2027E |

| Eternal* | 7795 TT | Buy (1) | 460.5 | 1,138 | 7.5 | 134% | 148.3 | 103.0 | 27.0 | 20.5 | 12.1 | 8.8 | 13.8 | 15.0 | 36.7 |

| Group Up | 6664 TT | Not rated | 368.0 | 702 | 24.4 | 17% | 24.4 | 21.6 | 17.8 | 5.3 | n.a. | n.a. | 22.5 | 24.0 | 25.4 |

| C Sun | 2467 TT | Not rated | 560.0 | 2,752 | 51.6 | 77% | 101.8 | 45.2 | 32.6 | 13 | 12.4 | 10.4 | 14.6 | 27.2 | 30.9 |

| Average | 91.5 | 56.6 | 25.8 | 20.5 | 12.2 | 9.6 | 16.9 | 22.0 | 31.0 |

Source: Companies, Bloomberg, *Daiwa forecasts

Note: Share prices as of 26 June 2026

Source: TEJ, Daiwa forecasts

Daiwa

Risks to our call

- Slower-than-expected substrate capex growth. If AI infrastructure investments slow, end-customer demand weakens, or substrate makers delay capacity additions, equipment procurement could be postponed, leading to lower order intake and revenue growth for Eternal. This would be the key downside risk to our call.

- Market share loss to competitors. Eternal's dominant position in high-end vacuum laminators is closely tied to Ajinomoto's leading market share in ABF film. If competing substrate materials gain qualification at major substrate makers, Ajinomoto's market position could weaken. In addition, if competitors narrow the technology gap and gain customer qualifications for high-end vacuum laminators, Eternal's market share could be affected. This would represent a secondary downside risk to our call.

- Slower commercialisation of PLP and GCS applications. We view PLP and GCS as potential long-term growth drivers for Eternal's vacuum lamination technology. However, commercialisation timelines remain uncertain due to technical challenges, customer qualification requirements, and ecosystem readiness. Delays in adoption or lower-than-expected industry penetration could reduce the company's exposure to these emerging opportunities.

- Limited free float and liquidity. With a free float of c.27%, the stock may be less attractive to certain institutional investors with liquidity requirements. Any future increase in free float could help enhance market liquidity and expand investor participation.

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Eternal Precision Mechanics (7795 TT): 26 June 2026

Company profile

Company background

Eternal traces its roots to Nichigo Morton, which began collaborating with Ajinomoto in 1997 to develop the industry's first vacuum laminator for ABF substrate production. Following the acquisition by Eternal Materials, the equipment division was spun off and merged with a Japanese subsidiary to formally establish Eternal. Notably, Kazutoshi Iwata, who led the original ABF equipment development project, currently serves as the company's General Manager.

The company specialises in vacuum laminators used in ABF substrates, PCB, and nextgeneration packaging applications. Benefiting from its long-standing partnership with Ajinomoto and deep understanding of ABF material characteristics, Eternal has established a c.95% market share in the high-end vacuum laminator.

Eternal: three-stage vacuum laminator

Source: Eternal

Eternal operates manufacturing facilities in Japan and China, with the Chiryu plant serving as its primary R&D and high-end equipment production centre. To meet growing demand from substrate makers, the company is expanding capacity through a new facility in Toyota City. Looking ahead, management is also developing vacuum lamination solutions for emerging applications such as PLP and GCS, creating additional long-term growth opportunities beyond traditional ABF substrates.

Shareholder structure

Eternal's shareholder base is relatively concentrated, with Eternal Materials, its parent company, holding a 61.7% stake. Other major shareholders include strategic investors such as All Ring, and several financial institutions. The company currently has a free float of c.27%, while we believe the shareholder base demonstrates strong strategic alignment, with several investors maintaining long-term business relationships with the company.

Eternal: shareholder structure (as of 26 June 2026)

| Holder | Share (%) |

|---|---|

| Eternal Materials Co Ltd | 61.7 |

| Kwang Yang Motor Co Ltd | 2.62 |

| LI CHIA-JUNG | 1.32 |

| Hua Yang Corp | 1.31 |

| All Ring Tech Co Ltd | 1.17 |

| CHUN CHUANG DEV ERH VEN CAP LP | 1.02 |

| Kwang Hsing Industrial Co Ltd | 0.86 |

| Kao Kuo-Lun | 0.84 |

| Gains Investment Corp | 0.79 |

| Yuanta Financial Holding Co Ltd | 0.76 |

Source: Bloomberg, Company

Daiwa

Eternal Precision Mechanics (7795 TT): 26 June 2026

Glossary of terms

· Ajinomoto Build-up Film (ABF)

A high-performance insulating film developed by Ajinomoto and widely used in FC-BGA substrates. ABF enables fine-line routing, high layer counts, and low signal loss for advanced semiconductor packages.

· Panel-Level Packaging (PLP)

An advanced packaging technology that replaces circular wafers with large rectangular panels, improving area utilization, throughput, and manufacturing efficiency for highvolume semiconductor packaging.

· Glass Core Substrate (GCS)

A next-generation substrate technology that uses glass as the core material. GCS offers superior flatness, dimensional stability, and fine-line capability for advanced AI and HPC packages.

· High Bandwidth Memory (HBM)

A stacked DRAM technology that vertically integrates multiple memory dies using TSVs, delivering significantly higher bandwidth and lower power consumption than conventional memory solutions.

· Photo-Imageable Dielectric (PID)

A dielectric material that can be directly patterned using photolithography. PID enables fine-feature redistribution layers and high-density interconnects in advanced packaging applications.

· Redistribution Layer (RDL)

A metal interconnect layer used to reroute electrical signals between semiconductor dies, package substrates, and external connections, enabling higher I/O density and heterogeneous integration.

· Outsourced Semiconductor Assembly and Test (OSAT)

Companies that provide semiconductor packaging and testing services for fabless and integrated device manufacturers, including advanced packaging technologies and final product qualification.

· Through-Glass Vias (TGVs)

Vertical conductive pathways formed through glass substrates, enabling electrical connections between different package layers while supporting high-density interconnect and advanced packaging architectures.

· Embedded Multi-die Interconnect Bridge (EMIB)

Intel's advanced packaging technology that embeds a small silicon bridge within the substrate to connect multiple dies, providing high-bandwidth communication without a full silicon interposer.

Daiwa

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| G | Executive/board quality | 1 | Eternal demonstrates a solid corporate governance structure supported by a balanced and diversified board composition. The company's board consists of 7 members, including 3 independent directors, with backgrounds spanning industry operations, finance, accounting, legal, and academia, enabling comprehensive oversight across business and governance functions. |

| Capital management | 2 | Eternal adopts a prudent capital management strategy, supported by a stable shareholder structure and disciplined financial policy. The company is majority-owned by Eternal Materials (over 60% stake), providing long-term strategic backing and financial stability. | |

| S | Related party & transaction | 1 | Eternal discloses related-party transactions transparently and enforces strict governance procedures to manage potential conflicts of interest. Board members are required to recuse themselves from discussions and voting on matters involving personal or affiliated interests, such as asset acquisitions, patent licensing, and remuneration decisions. |

| Product quality & safety | 1 | Eternal maintains strict product quality control, covering design, manufacturing, and delivery processes. The company emphasizes equipment reliability and performance stability, supported by long-term client relationships and low defect risks, ensuring high customer satisfaction and consistent product safety standards. | |

| E | Product design & lifecycle management | 2 | Eternal focuses on enhancing product durability and energy efficiency through continuous R&D innovation. Its equipment design emphasizes precision, extended lifecycle and reduced material waste, aligning product development with resource efficiency and long-term environmental sustainability goals. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 26 Jun 2026

Source: Daiwa, Company

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa

Eternal Precision Mechanics (7795 TT): 26 June 2026

Daiwa's Asia Pacific Research Directory

| HONG KONG | ||

|---|---|---|

| Hiroyuki GOTO | (852) 2773 8870 | hiroyuki.goto@hk.daiwacm.com |

| John HETHERINGTON (852) 8787 | 2773 Research and Head | john.hetherington@hk.daiwacm.com of Research Publications |

| Co-Head of Asia Pacific | ||

| Li XIONG | (852) 2773 8878 | li.xiong@hk.daiwacm.com |

| Strategy (Hong Kong/China) | ||

| Yue TAN | (852) 2848 4947 | yue.tan@hk.daiwacm.com |

| Strategy (Greater China) and Macro Economics (China) | ||

| Kelvin LAU | (852) 2848 4467 | kelvin.lau@hk.daiwacm.com |

| Regional Head of Automobiles, Industrials and Transportation | ||

| Evelyn ZHANG | (852) 2848 4970 | evelyn.zhang@hk.daiwacm.com |

| Frank YIP | (852) 2773 8842 | frank.yip@hk.daiwacm.com |

| Industrials and Transportation (Hong Kong/China) | ||

| Carol XIA | (852) 2532 4349 | carol.xia@hk.daiwacm.com |

| Head of China Consumer; Consumer (Hong Kong/China) | ||

| Steven NIE | (852) 2848 4464 | steven.nie@hk.daiwacm.com |

| Consumer (Hong Kong/China); Global Cryptocurrency | ||

| Siman CHEN | (852) 2532 4350 | siman.chen@hk.daiwacm.com |

| (Hong Kong/China) | ||

| Consumer Jing YANG | (852) 2532 4308 | jing.yang@hk.daiwacm.com |

| Head of China Healthcare | ||

| John CHOI | (852) 2773 8730 | john.choi@hk.daiwacm.com |

| Head of China Internet; Regional Head of Emerging Opportunities | ||

| Dennis IP 4068 Head of Asia US Power Equipment Wind, | (852) 2848 ex-Japan Power, Utilities, (Gas, Nuclear, Solar, | dennis.ip@hk.daiwacm.com Renewables & ESG (PURE) Research Grid, ESS & Battery Materials) |

| Derek ZHANG | (852) 2532 4341 | derek.zhang@hk.daiwacm.com |

| Power, Utilities, Renewables and ESS (PURE) - Gas, Wind and Grid (China), Utilities | ||

| (852) 2848 | ||

| Tina YU | (852) 2532 | tina.yu@hk.daiwacm.com |

| ESG (Asia ex-Japan) | ||

| 4106 | ||

| Power, Utilities, Renewables and ESS (PURE) - Power Equipment (US) | ||

| Marco ZENG | ||

| 4430 | ||

| marco.zeng@hk.daiwacm.com | ||

| (Hong Kong) |

Daiwa

| CHINA | CHINA | CHINA |

|---|---|---|

| Louis LUO | (86) 21 6841 3282 | louis.luo@daiwacm.cn |

| Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) |

| Mavis MA | (86) 21 6841 3288 | mavis.ma@daiwacm.cn |

| Leo LU Power, Utilities, Renewables Infrastructure (China) | (86) 21 6841 3286 and ESS | leo.lu@daiwacm.cn (PURE) - Solar, ESS, Lithium, AIDC Power & |

| Skye LIANG Power, Utilities, Renewables | (86) 21 6841 3207 and ESS (PURE) | skye.liang@daiwacm.cn Wind and Grid (China) |

| William WU Property (China/Hong | (86) 21 6841 3200 Kong) | william.wu@daiwacm.cn |

| Bintuo NI Tech Hardware and | (86) 21 6841 3228 Semiconductors (China) | bintuo.ni@daiwacm.cn |

| SOUTH KOREA | ||

|---|---|---|

| Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare |

| Mike OH | (82) 2 787 9179 | mike.oh@kr.daiwacm.com |

| Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities |

| Youngho JANG Consumer, Healthcare | (82) 2 787 9838 | youngho.jang@kr.daiwacm.com |

| Henny JUNG EV Batteries and Battery Components | (82) 2 787 9182 Materials, IT/Electronics | henny.jung@kr.daiwacm.com (Small/Mid Cap), Automobiles |

| Daeho SON Industrials - Robotics | (82) 2 787 9176 | dh.son@kr.daiwacm.com |

| Joon LEE Media | (82) 2 787 9151 | hj.lee@kr.daiwacm.com |

| Thomas Y KWON | (82) 2 787 9181 | yskwon@kr.daiwacm.com |

| Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games |

| SK KIM | (82) 2 787 9173 | sk.kim@kr.daiwacm.com |

| TAIWAN | TAIWAN |

|---|---|

| Rick HSU | (886) 2 8758 6261 rick.hsu@daiwacm-cathay.com.tw |

| Head of Regional Technology; Head of Taiwan Research; Semiconductors (Regional) | Head of Regional Technology; Head of Taiwan Research; Semiconductors (Regional) |

| Sheng CHENG | (886) 2 8758 6253 sheng.cheng@daiwacm-cathay.com.tw |

| IT/Technology Hardware (Automation, Datacentre Components and PCB/CCL) (Greater | IT/Technology Hardware (Automation, Datacentre Components and PCB/CCL) (Greater |

| Allan WANG | (886) 2 8758 6249 allan.wang@daiwacm-cathay.com.tw |

| IT/Technology Hardware (Automation, Datacentre Components and PCB/CCL) (Greater China) | IT/Technology Hardware (Automation, Datacentre Components and PCB/CCL) (Greater China) |

| Stacy LIN | (886) 2 8758 6252 stacy.lin@daiwacm-cathay.com.tw |

| IT/Technology - Semiconductors Supply Chain (Taiwan) | IT/Technology - Semiconductors Supply Chain (Taiwan) |

| Helen CHIEN | (886) 2 8758 6254 helen.chien@daiwacm-cathay.com.tw |

Daiwa's Offices

| Office / Branch / Affiliate | Address | Tel | Fax |

|---|---|---|---|

| DAIWA SECURITIES GROUP INC | |||

| HEAD OFFICE | Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 | (81) 3 5555 3111 | (81) 3 5555 0661 |

| Daiwa Securities Trust Company | One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. | (1) 201 333 7300 | (1) 201 333 7726 |

| Daiwa Securities Trust and Banking (Europe) PLC (Head Office) | 5 King William Street, London EC4N 7JB, United Kingdom | (44) 207 320 8000 | (44) 207 410 0129 |

| Daiwa Europe Trustees (Ireland) Ltd | Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland | (353) 1 603 9900 | (353) 1 478 3469 |

| Daiwa Capital Markets America Inc. New York Head Office | 1251 Avenue of the Americas, 49th Floor, New York, NY 10020 | (1) 212 612 7000 | (1) 212 612 7100 |

| Daiwa Capital Markets America Inc. San Francisco Branch | 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. | (1) 415 955 8100 | (1) 415 956 1935 |

| Daiwa Capital Markets Europe Limited, London Head Office | 5 King William Street, London EC4N 7AX, United Kingdom | (44) 20 7597 8000 | (44) 20 7597 8600 |

| Daiwa Capital Markets Deutschland GmbH | Friedrich-Ebert-Anlage 35-37, 60327 Frankfurt am Main, Germany | (49) 69 27139 8100 | (49) 69 27139 8190 |

| Daiwa Capital Markets Europe Limited, Paris Representative Office | 17, rue de Surène 75008 Paris, France | (33) 1 56 262 200 | (33) 1 47 550 808 |

| Daiwa Capital Markets Europe Limited, Moscow Representative Office | Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation | (7) 495 641 3416 | (7) 495 775 6238 |

| Daiwa Capital Markets Europe Limited, Bahrain Branch | 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain | (973) 17 534 452 | (973) 17 535 113 |

| Daiwa Capital Markets Hong Kong Limited | Level 28, One Pacific Place, 88 Queensway, Hong Kong | (852) 2525 0121 | (852) 2845 1621 |

| Daiwa Capital Markets Singapore Limited | 7 Straits View, Marina One East Tower, #16-05 & #16-06, Singapore 018936, Republic of Singapore | (65) 6387 8888 | (65) 6282 8030 |