PDF 原檔:報告_Daiwa_貿聯_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_daiwa_Bizlink_001.png |

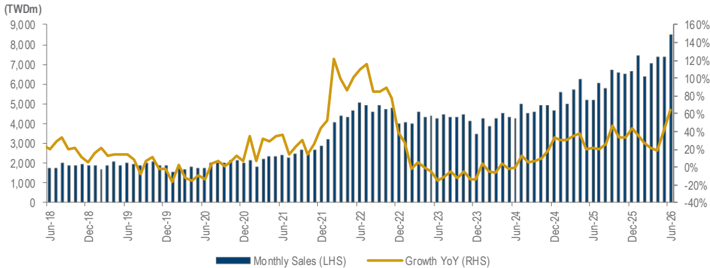

59KB | 真資料圖 | 月營收長條圖(TWDm,Jun-18 至 Jun-26),右軸 YoY 成長率折線;Jun-26 月營收創歷史新高 |

原始內容

Bizlink Holding (3665 TT)

Share price (6 Jul): TWD1,945.00

12-mth rating: Buy (1)

6 July 2026

Industrials: Taiwan

Record-high 2Q26 revenue slightly beat our and consensus estimates

Helen Chien

(886) 2 8758 6254

helen.chien@daiwacm-cathay.com.tw

Neil Teng

(886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Summary: Bizlink reported June 2026 revenue of TWD8,518m (+15.9% MoM and +63.8% YoY [+53.8% YoY in USD terms]; +34.0% YoY for 6M26 [+35.0% YoY in USD terms]) after market hours on 6 July 2026. Its 2Q26 revenue accounted for 101.2% and 101.8% of our and the Bloomberg consensus estimates for 2Q26 revenue, respectively.

We have a Buy (1) call, with a 12-month TP of TWD3,053, based on a PER of 30x on our 1-year-forward EPS forecast. For more information on the company, please refer to our latest memo , Announced capital-raising via GDR and ECB , on 3 July 2026.

What's the impact

- Record-high 2Q26 revenue slightly beat our and consensus estimates. Bizlink posted June 2026 revenue of TWD8,518m (+15.9% MoM and +63.8% YoY [+53.8% YoY in USD terms]; +34.0% YoY for 6M26 [+35.0% YoY in USD terms]), a record-high level. Its 2Q26 revenue (TWD23,253m, +15.9% QoQ and +63.8% YoY), also a record-high level, accounted for 101.2% and 101.8% of our (TWD22,989m, +10.2% QoQ and +35.8% YoY) and the Bloomberg consensus estimates for 2Q26 revenue, respectively. We attribute the upbeat revenue to the increase in HPC demand.

Bizlink: consolidated monthly sales

Source: Company

- Strong growth trend continues, driven by HPC and capital equipment demand. As integration increases, Bizlink will hit higher levels of optical adoption gradually by expanding its interconnect capabilities across both electrical and optical domains as the convergence of electrical and optical interconnect technologies addresses different system constraints and these technologies are also expected to coexist for an extended period as architectures evolve. According to Bizlink, the merger between the company and Interplex Datacom is expected to take place in 2H26.

What we recommend

We have a Buy (1) call, with a 12-month TP of TWD3,053, based on a PER of 30x on our 1-year-forward EPS forecast. Based on our 2026/27 EPS estimates, the stock is currently trading at PERs of 28.3x/17.7x, vs. its past-3-year trading range of 7-35x. Key risks: weaker-than-expected orders from secular growth drivers and gross margin expansion .

In the interests of timeliness, this document has not been edited.