PDF 原檔:報告_Daiwa_大量3167_20260525_original.pdf

原始內容

Taiwan

Ta Liang Technology (3167 TT)

Target price:

n.a.

Share price (22 May): TWD831.00 | Up/downside: -

High-precision moat in PCB machines

- Sole Chinese PCB machine maker with an in-house CCD controller

- Capacity fully booked through 2026

- TM machine bundles drive deeper wallet share from customers

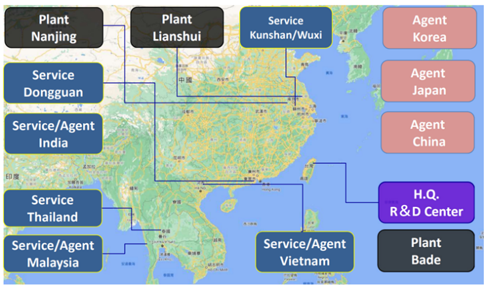

Background: Ta Liang Technology is a PCB routing and drilling machine maker serving PCB manufacturers, with high-end Charge-Coupled Devices (CCDs) commanding more than 2x the ASP of regular machines. The company operates production facilities in Taoyuan, Lianshui, and Nanjing, with a combined monthly capacity of c.300 units. CCDs are primarily adopted for back-drilling, though through-hole precision demand is increasingly emerging as an incremental growth driver. Ta Liang is also launching a patent-protected PCB inner layer thickness metrology (TM) machine to complement CCDs at an ideal TM:CCD ratio of 1:8, while additionally serving the semiconductor industry with metrology, AOI, and automation solutions.

Highlights: Ta Liang and Schmoll (not listed, Germany) are the only machine makers globally owning in-house controllers, creating a strong technology moat in the CCD market. Ta Liang continues to gain share from Schmoll through competitive pricing, solid brand recognition among PCB makers, and favourable domestic policy tailwinds supporting China-made equipment. In standard drilling and routing, Chinese competitors Vega CNC (not listed) and Hans Laser (002008 CH, NR) hold significantly larger capacity, though the competitive landscape in this segment has remained relatively stable. The patent-protected TM machine, which bundles naturally with CCDs, provides an additional lever to deepen customer relationships and reinforce share gains in the high-end segment.

Looking ahead, we see multiple growth catalysts supporting Ta Liang's growth trajectory. Demand for CCDs is expanding beyond back-drilling into through-hole processes where precision requirements are increasing, while the TM machine serves as a natural bundle driver to further accelerate CCD adoption and deepen wallet share per customer. CCDs carry high ASPs and deliver more than double the margins of regular machines, driving a favourable product mix shift alongside steady growth in regular machine demand underpinned by PCB makers' expanding capex cycle. Reflecting strong commercial momentum, Ta Liang has secured orders at full capacity through 2026, with near-term upside from outsourced capacity additions of c.50 incremental units for regular machines and a potential expansion from the current single working shift to a maximum of three shifts in Nan Jing Plant.

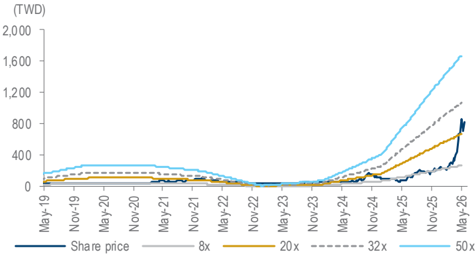

Valuation: The stock is trading at 108x PER and 23x PBR for 2025 (vs. its PBR range of 1-10x prior to 2026), reflecting the market's recognition of Ta Liang's high-end product transition and earnings upside potential from CCDs and TM machine.

25 May 2026

5

Daiwa

4

2

Sheng Cheng

Sheng Cheng (886) 2 8758 6253

sheng.cheng@daiwacm-cathay.com.tw

Allan Wang (886) 2 8758 6249

allan.wang@daiwacm-cathay.com.tw

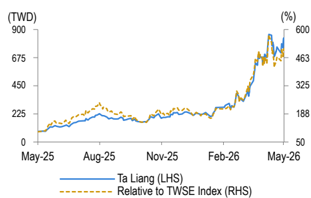

Share price performance

| 12-month range | 85.50-861.00 |

|---|---|

| Market cap (USDbn) | 2.34 |

| 3m avg daily turnover (USDm) | 48.8 |

Source: FactSet, Daiwa forecasts

Ta Liang: product portfolio

Ta Liang: production and service sites

Plant

Plant

Nanjing

Prilling Machine

Service

Dongguan

Service/Agent

India

PCB Router

Agent

Korea

PCB Inner layer solution

Agent

Japan

Agent

China

Ta Liang: quarterly and annual P&L statement

| 2024 | 2024 | 2024 | 2024 | 2025 | 2022 | 2023 | 2024 | 2025 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | ||||

| Net revenue | 399 | 490 | 721 | 989 | 844 | 1,271 | 1,415 | 1,549 | 2,370 | 1,292 | 2,599 | 5,078 |

| COGS | -332 | -350 | -496 | -670 | -555 | -777 | -861 | -897 | -1,774 | -965 | -1,849 | -3,089 |

| Gross profit | 67 | 140 | 225 | 319 | 289 | 494 | 554 | 652 | 596 | 327 | 751 | 1,989 |

| Operating expenses | -124 | -131 | -178 | -246 | -193 | -247 | -263 | -370 | -489 | -373 | -679 | -1,073 |

| Operating profit | -57 | 9 | 47 | 74 | 96 | 247 | 291 | 282 | 107 | -46 | 72 | 916 |

| Non-operating profit | 36 | 14 | 5 | 21 | 22 | -4 | 5 | 31 | 257 | 64 | 77 | 54 |

| Pre-tax profit | -21 | 23 | 52 | 94 | 119 | 243 | 296 | 313 | 363 | 18 | 149 | 971 |

| Income taxes | 5 | 3 | -9 | -23 | -29 | -68 | -81 | -77 | -50 | -5 | -24 | -255 |

| Net profit | -16 | 26 | 43 | 72 | 90 | 175 | 215 | 236 | 313 | 13 | 124 | 716 |

| Net EPS (TWD) | -0.19 | 0.31 | 0.52 | 0.81 | 1.02 | 1.98 | 2.43 | 2.67 | 3.91 | 0.16 | 1.41 | 8.11 |

| Operating Ratios | ||||||||||||

| Gross margin | 16.8% | 28.5% | 31.2% | 32.3% | 34.3% | 38.9% | 39.1% | 42.1% | 25.1% | 25.3% | 28.9% | 39.2% |

| Operating margin | -14.4% | 1.7% | 6.6% | 7.4% | 11.4% | 19.4% | 20.6% | 18.2% | 4.5% | -3.6% | 2.8% | 18.0% |

| Pre-tax margin | -5.3% | 4.7% | 7.3% | 9.5% | 14.1% | 19.1% | 20.9% | 20.2% | 15.3% | 1.4% | 5.7% | 19.1% |

| Net margin | -4.0% | 5.2% | 6.0% | 7.2% | 10.7% | 13.8% | 15.2% | 15.2% | 13.2% | 1.0% | 4.8% | 14.1% |

| YoY (%) | ||||||||||||

| Net revenue | 55% | 91% | 134% | 110% | 112% | 159% | 96% | 57% | -47% | -45% | 101% | 95% |

| Gross profit | 106% | 117% | 186% | 110% | 333% | 253% | 146% | 104% | -48% | -45% | 129% | 165% |

| Operating profit | 68% | -143% | -352% | 177% | - | 2789% | 513% | 284% | -81% | -143% | -256% | 1171% |

| Pre-tax profit | -24% | 84% | 726% | 248% | - | 956% | 464% | 232% | -36% | -95% | 726% | 553% |

| Net profit | -30% | 337% | 367% | 245% | - | 585% | 396% | 230% | -29% | -96% | 870% | 476% |

| QoQ (%) | ||||||||||||

| Net revenue | -15% | 23% | 47% | 37% | -15% | 51% | 11% | 9% | ||||

| Gross profit | -56% | 109% | 61% | 42% | -9% | 71% | 12% | 18% | ||||

| Operating profit | - | - | 455% | 55% | 31% | 156% | 18% | -3% | ||||

| Pre-tax profit | - | - | 128% | 80% | 26% | 105% | 22% | 6% | ||||

| Net profit | - | - | 69% | 65% | 26% | 95% | 23% | 10% |

Source: Company

Ta Liang: 1-year forward PER

Source: TEJ, Bloomberg

Ta Liang: product portfolio

Source: Company

Lianshui standard

Service

Kunshan/Wuxi

CCD series

Ta Liang Technology (3167 TT): 25 May 2026

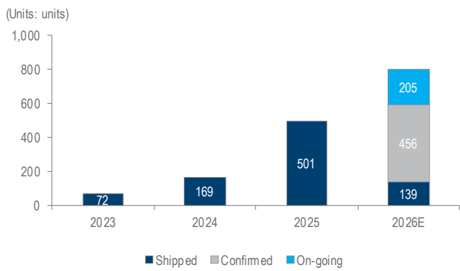

Ta Liang: 2023-2023 CCD shipments and orders

Source: Company

Ta Liang: production and service sites

Source: Company

Daiwa

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_大量3167_20260525_003.png |

88KB | 真資料圖 | 「Da Liang: product portfolio」產品線圖,含 Drilling Machine(standard/CCD series/PCB Inner layer solution)、PCB Router(standard/CCD series/depth control)、Edge Coater(1 station/multi stations)各型設備照片 |

報告_Daiwa_大量3167_20260525_004.png |

18KB | 真資料圖 | 堆疊長條圖(單位:units),2023-2026E 出貨量按 Shipped/Confirmed/On-going 分層:2023=72、2024=169、2025=501、2026E=139+456+205(共約800) |