PDF 原檔:報告_Daiwa_台光電_20260703_original.pdf

圖片清單(已驗證 2026-07-06)

嵌圖只從此清單挑分類為「真資料圖」者,圖說照抄「親眼所見內容」。<40KB 未 Read(預設 logo)。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

2026-07-03 260703_daiwa_EMC_001.png |

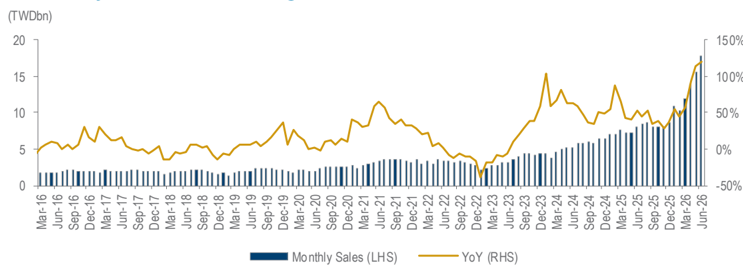

68KB | 真資料圖 | 台光電月營收柱狀圖(TWDbn)與 YoY 成長率折線圖(Mar-16 至 Jun-26) |

原始內容

Elite Material (2383 TT)

Share price (3 Jul): TWD6,080.00

12-mth rating: Buy (1)

June update: record-high monthly sales

Sheng Cheng

(886) 2 8758 6253

sheng.cheng@daiwacm-cathay.com.tw

Allan Wang

(886) 2 8758 6249

allan.wang@daiwacm-cathay.com.tw

Summary: EMC announced its June revenue of TWD17.7bn (up 14% MoM and 121% YoY), which makes its 2Q sales of TWD47.3bn (up 43% QoQ and 110% YoY) and achieves 112% of our 2Q26 revenue forecast (TWD42.2bn; up 28% QoQ and 88% YoY) and 114% of Bloomberg consensus (TWD41.5bn). The actual results were higher than market expectations of 15-20% QoQ growth, while the better-than-expected price hike effect contributed around two-thirds of QoQ growth magnitude (ie.28% QoQ), with the remainder driven by an improved revenue mix (lower contribution from handset and automotive). We believe c.28% price hike should already factor in most of the cost increases from raw material since 2H25 to 1Q26. However, management doesn't rule out the possibility of further raising prices in 2H26 given the on-going price increase in raw materials from 2Q26. We see EMC as the leader in CCL market and expect it to continue benefitting from ASP increases (at least 30% every generation) due to the high speed transmission requirements driven by AI mega trend. As such, we remain positive on EMC, with a Buy (1) on the name. Key downside risk: weaker-than-expected AI server demand.

EMC: Jun-26 monthly sales (TWDbn)

| Company | Ticker | Price | Rating Jun | Sales | MoM YoY | Sales QoQ | YoY | Achieved% | PER 2026E 2027E | 3-Yr Range | Release Date | Consensus | Consensus Achieved% |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Datacentre EMC | 2383 TT 5,655.0 | Buy | 17.7 | 14% | 121% | 47.3 43% | 110% | 112% | 63.6 34.4 | 6-30x | 3-Jul | 41.5 | 114% |

Source: Company, Daiwa forecasts

EMC: monthly revenue trend and YoY growth

Source: Company

What's new:

EMC announced its June revenue of TWD17.7bn (up 14% MoM and 121%YoY), which makes its 2Q sales of TWD47.3bn (up 43% QoQ and 110% YoY) and achieves 112% of our 2Q26 revenue forecast (TWD42.2bn; up 28% QoQ and 88% YoY) and 114% of the Bloomberg consensus (TWD41.5bn). The actual results were higher than market expectations of 15-20% QoQ growth, while the better-than-expected price hike effect contributed around two-thirds of QoQ growth magnitude (ie.28% QoQ), with the remainder driven by an improved revenue mix (lower contribution from handset and automotive). Although EMC raised its prices to pass through the additional material costs (eg. copper, glass fibre, etc) at a slightly lower pace, which weighed on gross margin in 1Q26, we believe the c.30% price hike in 2Q26 should already cover most of cost inflation from 2H25 to 1Q26.

3 July 2026

Information Technology: Taiwan

Looking ahead, management doesn't rule out the possibility of further price hikes as some raw material costs rise again (eg. low dk and low dk2 glass fibre, copper foil, etc). However, the magnitude (if any) would be lower than that in 2Q26. We expect EMC to continue acting as the global CCL leader and to benefit from continued ASP increases due to spec upgrade trend. Based on our understanding, Nvidia would migrate to M8+ or M9Q from Rubin and to M9, M9Q, M10, or PTFE from Rubin Ultra. As for the ASIC camp, it would migrate to M9 or M9Q starting next year from the current M8+.

While EMC already has a higher revenue mix from high end CCL grades (eg. 70% in 2026E) and key handset clients, we expect the room for EMC to further optimize product mix to be smaller than that of peers. As such, the new capacity will have to wait until 4Q26 from EMC's Guanyin plant.

What we recommend:

We have a Buy (1) rating on EMC with a 12M TP of TWD6,022, based on a target PER of 48x applied to our 1-year-forward EPS forecast. Key downside risk: weaker-than-expected AI server demand.

In the interests of timeliness, this document has not been edited.