PDF 原檔:報告_BofA_宏碁2353_20260715_original.pdf

圖片清單(已驗證 2026-07-17)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260715_ml_acer_004.png |

55KB | 真資料圖 | 宏碁股價(NT$,深藍線,2023/7-2026中)疊加歷次目標價(PO)沿革標註:22→26→31→34→35→31→30→29→26,含每次調整日期,底色淺藍區塊代表當期 PO 區間 |

260715_ml_acer_002.png |

36KB | 真資料圖 | Exhibit 7:宏碁歷史 P/B 走勢圖(2008/1-2026),深藍線為 P/B(x),另繪 -1SD/Mean/+1SD 三條水平線(約0.5x/0.85x/1.25x),近期在均值上緣 |

260715_ml_acer_003.png |

34KB | 真資料圖 | Exhibit 6:宏碁歷史 P/E 走勢圖(2017/1-2026),深藍線為 P/E(x),另繪 -1SD/Mean/+1SD 三條水平線(約4x/11x/19x),近期落在均值與+1SD之間 |

260715_ml_acer_001.png |

31KB | 真資料圖 | Exhibit 1:宏碁(深藍)與華碩(淺藍)季度存貨天數比較折線圖,1Q23-1Q26,1Q26 分別為 99 天/125 天 |

原始內容

Acer

Better 2Q26 sales; margin key watch point; reiterate Underperform with NT$26 PO

Reiterate Rating: UNDERPERFORM | PO: 26.00 TWD | Price: 31.05 TWD

Better 2Q26 sales driven by AI, commercial, non-PC

Acer ' s 2Q26 sales of NT$85.3bn (+18% QoQ, +28% YoY) were 23%/5% above BofAe/ consensus. We particularly highlight the better sales from AI, commercial, and non-PC businesses. According to Acer, sales from desktop, commercial products (excluding Chromebook), and non-PC grew 57.3%, 47.3%, and 48.2% YoY in 2Q26, respectively. Acer cited the strong desktop sales were mainly due to AI usage. The non-PC sales accounted for 34.3% of total in 2Q26, vs. 34.7%/29.9% in 1Q26/2Q25. Acer will report 2Q26 earnings after market close on 6 Aug and hold an analyst debriefing on 18 Aug.

Expect decent sales growth, but margins key watch point

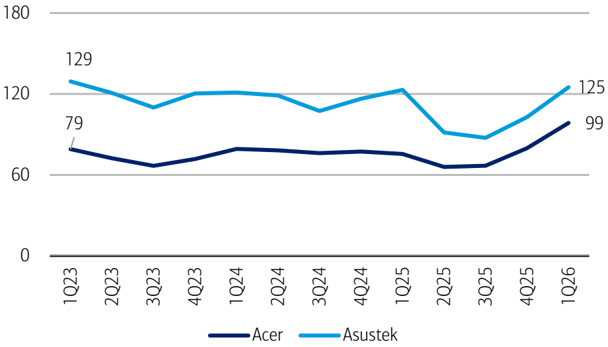

Following memory price hikes and components tightness, we believe Acer and other PC brands should be able to raise prices to reflect the higher costs. This could lead to decent sales growth in 2026 (BofAe: +19% YoY for Acer) despite soft end-market demand. We flag margins as the key watch point during the prolonged memory upcycle, given Acer ' s smaller PC market share. In 1Q26, Acer ' s PC shipment share was 5.9%, vs. top 3 names Lenovo/HP/Dell at 24.3%/17.4%/14.2%. Acer and Asustek had high inventory days at 99/125 as of 1Q26 (Exhibit 1).

Maintain PO of NT$26; reiterate Underperform

We cut our 2026-27E EPS by 6-7% (to reflect 2025/1Q26 actual data, better 2Q26 sales, and margin concerns) and introduce our 2028 estimates (Exhibit 2). We maintain our PO of NT$26 with a valuation base rollover but unchanged P/E multiple -currently based on 15x 2H26-1H27E EPS vs. 15x 4Q25-3Q26E EPS previously. We reiterate Underperform on Acer, given moderate PC demand, potential margin pressure from component price hikes, and above-peer valuation (currently trades at 18x 2027E P/E vs. the peer average of 17x; Exhibit 5).

| Estimates (Dec) (NT$) | 2023A | 2024A | 2025E | 2026E | 2027E |

|---|---|---|---|---|---|

| Net Income (Adjusted - mn) | 4,932 | 5,539 | 3,950 | 5,563 | 5,724 |

| EPS | 1.64 | 1.84 | 1.31 | 1.85 | 1.90 |

| EPS Change (YoY) | -1.4% | 12.1% | -28.7% | 40.9% | 2.9% |

| Consensus EPS (Visible Alpha) | 1.25 | 1.54 | 1.61 | ||

| Dividend / Share | 1.60 | 1.70 | 1.05 | 1.48 | 1.52 |

| Free Cash Flow / Share | 4.05 | -2.00 | 0.85 | 0.99 | 1.08 |

| Valuation (Dec) | |||||

| P/E | 18.9x | 16.9x | 23.6x | 16.8x | 16.3x |

| Dividend Yield | 5.2% | 5.5% | 3.4% | 4.8% | 4.9% |

| EV / EBITDA* | 16.4x | 13.8x | 16.2x | 12.0x | 11.7x |

| Free Cash Flow Yield* | 12.9% | -6.3% | 2.7% | 3.2% | 3.4% |

| * For full definitions of iQ method SM measures, see page 8. |

This research report provides general information only. No part of this report may be used or reproduced or quoted in any manner whatsoever in Taiwan by the press or other persons without the express written consent of BofA Securities.

>> Employed by a non-US affiliate of BofAS and is not registered/qualified as a research analyst under the FINRA rules.

Refer to "Other Important Disclosures" for information on certain BofA Securities entities that take responsibility for the information herein in particular jurisdictions.

BofA Securities does and seeks to do business with issuers covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Refer to important disclosures on page 9 to 11. Analyst Certification on page 6. Price

15 July 2026

Equity

Robert Cheng >> Research Analyst Merrill Lynch (Taiwan) +886 2 2376 3731 robert.cheng@bofa.com

Doris Kao >> Research Analyst Merrill Lynch (Taiwan) +886 2 2376 3722 doris.kao@bofa.com

Katherine Zhu >> Research Analyst Merrill Lynch (Hong Kong) +852 3508 3374

kexin.zhu@bofa.com

Stock Data

| Price | 31.05 TWD |

|---|---|

| Price Objective | 26.00 TWD |

| Date Established | 18-Nov-2025 |

| Investment Opinion | B-3-7 |

| 52-Week Range | 25.00 TWD-44.20 TWD |

| Mrkt Val / Shares Out (mn) | 2,940 USD / 3,047.9 |

| Market Value (mn) | 94,636 TWD |

| Average Daily Value (mn) | 62.28 USD |

| Free Float | 93.7% |

| BofA Ticker / Exchange | ASIYF / TAI |

| Bloomberg / Reuters | 2353 TT / 2353.TW |

| ROE (2025E) | 5.2% |

| Net Dbt to Eqty (Dec-2024A) | -33.4% |

For a full list of acronyms, see Exhibit 11

iQ profile SM Acer

| Key Income Statement Data (Dec) | 2023A | 2024A | 2025E | 2026E | 2027E |

|---|---|---|---|---|---|

| (NT$ Millions) | |||||

| Sales | 241,308 | 264,682 | 272,484 | 287,042 | 300,023 |

| Gross Profit | 25,823 | 28,006 | 29,200 | 32,281 | 34,044 |

| Sell General &Admin Expense | (19,479) | (20,864) | (22,273) | (23,401) | (24,498) |

| Operating Profit | 4,225 | 4,876 | 4,828 | 6,613 | 7,047 |

| Net Interest &Other Income | 3,573 | 4,099 | 2,587 | 2,002 | 1,791 |

| Associates | NA | NA | NA | NA | NA |

| Pretax Income | 7,799 | 8,974 | 7,416 | 8,616 | 8,838 |

| Tax (expense) / Benefit | (2,168) | (2,756) | (1,963) | (2,412) | (2,475) |

| Net Income (Adjusted) | 4,932 | 5,539 | 3,950 | 5,563 | 5,724 |

| Average Fully Diluted Shares Outstanding | 3,001 | 3,006 | 3,006 | 3,006 | 3,006 |

| Key Cash Flow Statement Data | |||||

| Net Income | 4,932 | 5,539 | 3,950 | 5,563 | 5,724 |

| Depreciation &Amortization | 1,776 | 2,272 | 1,247 | 1,568 | 1,381 |

| Change in Working Capital | (1,238) | (12,584) | (3,743) | (4,386) | (4,102) |

| Deferred Taxation Charge | NA | NA | NA | NA | NA |

| Other Adjustments, Net | 7,213 | 3,250 | 1,503 | 640 | 640 |

| Cash Flow from Operations | 12,684 | (1,523) | 2,958 | 3,386 | 3,643 |

| Capital Expenditure | (516) | (4,482) | (400) | (400) | (400) |

| (Acquisition) / Disposal of Investments | (398) | (4,310) | 0 | 0 | 0 |

| Other Cash Inflow / (Outflow) | (6,452) | (6,035) | 0 | 0 | 0 |

| Cash Flow from Investing | (7,366) | (14,828) | (400) | (400) | (400) |

| Shares Issue / (Repurchase) | 433 | 1,023 | 0 | 0 | 0 |

| Cost of Dividends Paid | (4,928) | (5,338) | (3,160) | (4,451) | (4,579) |

| Cash Flow from Financing | (4,440) | 3,871 | (3,160) | (4,451) | (4,579) |

| Free Cash Flow | 12,167 | (6,005) | 2,558 | 2,986 | 3,243 |

| Net Debt | (45,553) | (27,914) | (27,312) | (25,847) | (24,511) |

| Change in Net Debt | (525) | 17,639 | 602 | 1,465 | 1,336 |

| Key Balance Sheet Data | |||||

| Property, Plant &Equipment | 4,424 | 8,431 | 7,584 | 6,416 | 5,434 |

| Other Non-Current Assets | 46,744 | 54,346 | 54,346 | 54,346 | 54,346 |

| Trade Receivables | 52,308 | 54,627 | 55,373 | 58,331 | 60,969 |

| Cash &Equivalents | 48,134 | 37,665 | 37,063 | 35,598 | 34,262 |

| Other Current Assets | 57,124 | 64,406 | 65,164 | 68,292 | 71,418 |

| Total Assets | 208,734 | 219,476 | 219,530 | 222,983 | 226,429 |

| Long-Term Debt | 1,565 | 3,663 | 3,663 | 3,663 | 3,663 |

| Other Non-Current Liabilities | 19,617 | 22,944 | 22,944 | 22,944 | 22,944 |

| Short-Term Debt | 1,016 | 6,088 | 6,088 | 6,088 | 6,088 |

| Other Current Liabilities | 106,193 | 103,211 | 100,972 | 102,672 | 104,334 |

| Total Liabilities | 128,392 | 135,906 | 133,667 | 135,367 | 137,029 |

| Total Equity | 80,342 | 83,570 | 85,863 | 87,616 | 89,400 |

| Total Equity &Liabilities | 208,734 | 219,476 | 219,530 | 222,983 | 226,429 |

| iQ method SM - Bus Performance* | |||||

| Return On Capital Employed | 4.7% | 4.5% | 4.2% | 5.1% | 5.3% |

| Return On Equity | 6.8% | 7.4% | 5.2% | 7.1% | 7.1% |

| Operating Margin | 1.8% | 1.8% | 1.8% | 2.3% | 2.3% |

| EBITDA Margin | 2.5% | 2.7% | 2.2% | 2.9% | 2.8% |

| iQ method SM - Quality of Earnings* | |||||

| Cash Realization Ratio | 2.6x | -0.3x | 0.7x | 0.6x | 0.6x |

| Asset Replacement Ratio | 0.5x | 3.6x | 0.3x | 0.3x | 0.3x |

| Tax Rate (Reported) | 27.8% | 30.7% | 26.5% | 28.0% | 28.0% |

| Net Debt-to-Equity Ratio | -56.7% | -33.4% | -31.8% | -29.5% | -27.4% |

| Interest Cover | 14.9x | 8.7x | 6.2x | 8.4x | 8.9x |

Key Metrics

- For full definitions of iQ method SM measures, see page 8.

Company Sector

Technology Strategy

Company Description

Acer, founded in 1976 and headquartered in Taiwan, is a global top PC brand company with business involvement in tech hardware and software. After underwent several transformations, new management team redirected business strategy to margin focus from volume focus. Acer now emphasizes on gaming PC business for margin expansion and seeks future growth opportunities in non-PC areas (e.g. IoT).

Investment Rationale

We have an Underperform rating on Acer in view of unjustified valuation despite PC demand recovery. It is trading at over 0.5SD above historical P/E average. Despite Acer's leading market share in Chromebook vendor (22% shipment share in 2022, following Dell's 21%), Chromebook demand has stabilized in 2023-24 from the peak level in 2020-21.

Stock Data

Price to Book Value

1.2x

Exhibit 1: Acer/Asustek had high inventory days - 99/125 days as of 1Q26

Quarterly inventory days: Acer and Asustek, 1Q23-1Q26

Source: BofA Global Research, TEJ, company data. Quarterly inventory days = 365 / 4 / (quarterly COGS / average inventories)

BofA GLOBAL RESEARCH

Exhibit 2: We cut 2026-27E EPS by 6-7% and introduce 2028 estimates

Earnings revisions summary, 2026-28E

| NT$mn | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|

| New | Old | Diff (%) | New | Old | Diff (%) | New | |

| Sales | 327,270 | 287,042 | 14% | 333,848 | 300,023 | 11% | 339,676 |

| Gross profit | 36,774 | 32,281 | 14% | 37,632 | 34,044 | 11% | 38,656 |

| Operating profit | 6,464 | 6,613 | -2% | 7,387 | 7,047 | 5% | 7,883 |

| Pretax profit | 8,692 | 8,616 | 1% | 8,915 | 8,838 | 1% | 9,412 |

| Net income | 5,222 | 5,563 | -6% | 5,302 | 5,724 | -7% | 5,660 |

| EPS (NT$) | 1.74 | 1.85 | -6% | 1.76 | 1.90 | -7% | 1.88 |

| Margin | |||||||

| Gross margin | 11.24% | 11.25% | 11.27% | 11.35% | 11.38% | ||

| Operating margin | 1.98% | 2.30% | 2.21% | 2.35% | 2.32% | ||

| Pre-tax margin | 2.66% | 3.00% | 2.67% | 2.95% | 2.77% | ||

| Net margin | 1.60% | 1.94% | 1.59% | 1.91% | 1.67% |

Source: BofA Global Research estimates. Diff: difference

BofA GLOBAL RESEARCH

Exhibit 3: Our 2026/28E earnings are 7%/23% above consensus and 2027E earnings are 4% below consensus

BofAe vs. consensus, 2026-28E

| NT$mn | BofAe | 2026E Consensus | Diff (%) | BofAe | 2027E Consensus | Diff (%) | BofAe | 2028E Consensus | Diff (%) |

|---|---|---|---|---|---|---|---|---|---|

| Sales | 327,270 | 312,367 | 5% | 333,848 | 345,743 | -3% | 339,676 | 307,447 | 10% |

| Gross profit | 36,774 | 35,132 | 5% | 37,632 | 39,104 | -4% | 38,656 | n.a. | n.a. |

| Operating profit | 6,464 | 6,079 | 6% | 7,387 | 7,820 | -6% | 7,883 | 7,509 | 5% |

| Pretax profit | 8,692 | 9,320 | -7% | 8,915 | 10,244 | -13% | 9,412 | 8,823 | 7% |

| Net income | 5,222 | 4,862 | 7% | 5,302 | 5,496 | -4% | 5,660 | 4,608 | 23% |

| EPS (NT$) | 1.74 | 1.62 | 7% | 1.76 | 1.83 | -4% | 1.88 | 1.53 | 23% |

| Margin | |||||||||

| Gross margin | 11.24% | 11.25% | 11.27% | 11.31% | 11.38% | n.a. | |||

| Operating margin | 1.98% | 1.95% | 2.21% | 2.26% | 2.32% | 2.44% | |||

| Pre-tax margin | 2.66% | 2.98% | 2.67% | 2.96% | 2.77% | 2.87% | |||

| Net margin | 1.60% | 1.56% | 1.59% | 1.59% | 1.67% | 1.50% |

Source: BofA Global Research estimates, Bloomberg. Diff: difference

BofA GLOBAL RESEARCH

Exhibit 4: Our new 2Q26E EPS is 19% above consensus

2Q26 results review

| NT$mn | 2Q26 BofAe New | QoQ (%) | YoY (%) | 2Q26 BofAe Old | Diff (%) | 2Q26 Consensus | Diff (%) | 1Q26 | 2Q25 |

|---|---|---|---|---|---|---|---|---|---|

| Sales | 85,296 | 18% | 28% | 69,624 | 23% | 81,312 | 5% | 72,423 | 66,532 |

| Gross profit | 9,500 | 17% | 41% | 7,721 | 23% | 9,215 | 3% | 8,086 | 6,729 |

| Operating profit | 1,781 | 122% | 143% | 1,455 | 22% | 1,679 | 6% | 803 | 734 |

| Pre-tax profit | 2,208 | 25% | 23% | 1,902 | 16% | 2,495 | -12% | 1,764 | 1,799 |

| Net profit | 1,440 | 105% | 33% | 1,210 | 19% | 1,214 | 19% | 702 | 1,085 |

| EPS (NT$) | 0.48 | 105% | 33% | 0.40 | 19% | 0.40 | 19% | 0.23 | 0.36 |

| Margin | |||||||||

| Gross margin | 11.14% | 0.0 ppt | 1.0 ppt | 11.09% | 0.0 ppt | 11.33% | -0.2 ppt | 11.16% | 10.11% |

| Operating margin | 2.09% | 1.0 ppt | 1.0 ppt | 2.09% | 0.0 ppt | 2.07% | 0.0 ppt | 1.11% | 1.10% |

| Pre-tax margin | 2.59% | 0.2 ppt | -0.1 ppt | 2.73% | -0.1 ppt | 3.07% | -0.5 ppt | 2.44% | 2.70% |

| Net margin | 1.69% | 0.7 ppt | 0.1 ppt | 1.74% | 0.0 ppt | 1.49% | 0.2 ppt | 0.97% | 1.63% |

Source: BofA Global Research estimates, company data, Bloomberg. Diff: difference

Exhibit 5: Acer trades at 18x 2027E P/E vs. the peer average of 17x

Valuation comparison: Acer and global peers

| Share price | Market cap | P/E (x) | P/E (x) | P/B (x) | P/B (x) | EPS growth | EPS growth | Dividend yield (%) | Dividend yield (%) | ROE (%) | ROE (%) | EV/EBITDA (x) | EV/EBITDA (x) | Net cash (debt) to market cap | Net cash (debt) to market cap | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ticker | Company | (LC) | (US$mn) | 26E | 27E | 26E | 27E | 26E | 27E | 26E | 27E | 26E | 27E | 26E | 27E | 26E | 27E |

| 2353 TT | Acer | 31.1 | 2,938 | 17.9 | 17.6 | 1.2 | 1.2 | 38% | 2% | 4.5 | 4.5 | 6.9 | 6.8 | 17.7 | 15.4 | -11% | -10% |

| Global peers | Global peers | Global peers | Global peers | Global peers | Global peers | Global peers | Global peers | ||||||||||

| 2357 TT | Asustek | 712.0 | 16,419 | 14.5 | 14.1 | 1.9 | 1.8 | -20% | 3% | 4.7 | 4.8 | 13.5 | 13.4 | 13.3 | 13.1 | -3% | -4% |

| 2377 TT | MSI * | 148.5 | 3,895 | 12.8 | 13.1 | 2.1 | 2.0 | 70% | -2% | 4.1 | 5.8 | 16.0 | 14.4 | 7.9 | 8.1 | 24% | 23% |

| 2376 TT | Gigabyte * | 344.0 | 7,155 | 11.3 | 10.1 | 3.2 | 2.8 | 67% | 11% | 4.9 | 6.1 | 30.3 | 27.6 | 8.3 | 7.7 | -4% | -5% |

| 992 HK | Lenovo | 23.2 | 37,981 | 22.8 | 14.9 | 37.1 | 28.5 | 27% | 53% | 1.6 | 1.6 | 29.9 | 35.2 | 8.6 | 7.2 | 0% | 1% |

| HPQ US | HP | 24.6 | 22,525 | 8.3 | 8.4 | 50.3 | 9.3 | -5% | -1% | 4.9 | 4.9 | n.m. | n.m. | 6.6 | 6.7 | -22% | -15% |

| DELL US | Dell | 457.5 | 295,636 | 44.4 | 23.5 | n.m. | 45.5 | 27% | 89% | 0.5 | 0.6 | n.m. | n.m. | 29.2 | 18.4 | -6% | -2% |

| AAPL US | Apple | 314.9 | 4,624,461 | 36.5 | 31.8 | 40.4 | 27.4 | 16% | 15% | 0.3 | 0.4 | n.m. | n.m. | 25.9 | 23.6 | -1% | -1% |

| Overall peer average | Overall peer average | Overall peer average | Overall peer average | 21.5 | 16.6 | 22.5 | 16.7 | 26% | 24% | 3.0 | 3.4 | 22.4 | 22.6 | 14.3 | 12.1 | -2% | 0% |

| Overall peer median | Overall peer median | Overall peer median | Overall peer median | 14.5 | 14.1 | 20.2 | 9.3 | 27% | 11% | 4.1 | 4.8 | 23.0 | 21.0 | 8.6 | 8.1 | -3% | -2% |

Source: BofA Global Research estimates, Bloomberg. Share price and market cap as of 2026/07/15 (Asia companies) and 07/14 (US companies). ROE (return on equity) refers to average ROE. LC: local currency. n.m.: not meaningful. EV: enterprise value. EBITDA: earnings before interest, taxes, depreciation, and amortization. * Non-covered companies' forecasts based on Bloomberg consensus.

BofA GLOBAL RESEARCH

Exhibit 7: Acer's historical P/B trading average since 2008 is at 0.9x Acer's historical P/B and -1/+1 standard deviation since 2008

Source: BofA Global Research estimates, TEJ, company data, Bloomberg

BofA GLOBAL RESEARCH

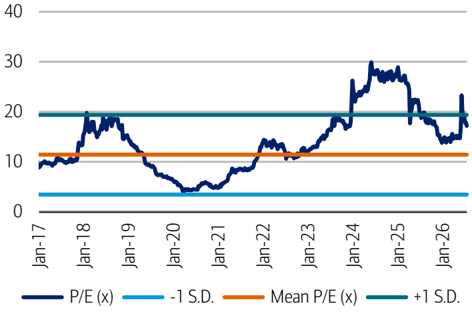

Exhibit 6: Acer's historical P/E trading average since 2006, but excluding outliers over 2010-16, is at 11x

Acer's historical P/E and -1/+1 standard deviation since 2017

Source: BofA Global Research estimates, TEJ, company data, Bloomberg

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Exhibit 8: We model Acer's 2026-28 sales/EPS CAGR at 2%/4%

Acer's quarterly earnings summary, 2025-28E

| NT$mn | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 1Q28E | 2Q28E | 3Q28E | 4Q28E | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 72,423 | 85,296 | 86,987 | 82,564 | 78,807 | 82,107 | 87,723 | 85,210 | 81,098 | 84,508 | 88,300 | 85,770 | 275,628 | 327,270 | 333,848 | 339,676 |

| Gross profit | 8,086 | 9,500 | 9,872 | 9,316 | 8,679 | 9,271 | 9,970 | 9,712 | 8,940 | 9,618 | 10,191 | 9,906 | 29,990 | 36,774 | 37,632 | 38,656 |

| Operating profit | 803 | 1,781 | 1,913 | 1,968 | 1,626 | 1,758 | 1,935 | 2,069 | 1,681 | 1,886 | 2,103 | 2,213 | 5,144 | 6,464 | 7,387 | 7,883 |

| Pretax profit | 1,764 | 2,208 | 2,368 | 2,353 | 1,914 | 2,159 | 2,380 | 2,461 | 1,976 | 2,282 | 2,548 | 2,607 | 7,651 | 8,692 | 8,915 | 9,412 |

| Net income | 702 | 1,440 | 1,545 | 1,534 | 741 | 1,395 | 1,554 | 1,612 | 785 | 1,483 | 1,674 | 1,717 | 3,780 | 5,222 | 5,302 | 5,660 |

| EPS (NT$) | 0.23 | 0.48 | 0.51 | 0.51 | 0.25 | 0.46 | 0.52 | 0.54 | 0.26 | 0.49 | 0.56 | 0.57 | 1.26 | 1.74 | 1.76 | 1.88 |

| Margin% | ||||||||||||||||

| Gross margin | 11.16% | 11.14% | 11.35% | 11.28% | 11.01% | 11.29% | 11.37% | 11.40% | 11.02% | 11.38% | 11.54% | 11.55% | 10.88% | 11.24% | 11.27% | 11.38% |

| Operating margin | 1.11% | 2.09% | 2.20% | 2.38% | 2.06% | 2.14% | 2.21% | 2.43% | 2.07% | 2.23% | 2.38% | 2.58% | 1.87% | 1.98% | 2.21% | 2.32% |

| Pretax margin | 2.44% | 2.59% | 2.72% | 2.85% | 2.43% | 2.63% | 2.71% | 2.89% | 2.44% | 2.70% | 2.89% | 3.04% | 2.78% | 2.66% | 2.67% | 2.77% |

| Net margin | 0.97% | 1.69% | 1.78% | 1.86% | 0.94% | 1.70% | 1.77% | 1.89% | 0.97% | 1.75% | 1.90% | 2.00% | 1.37% | 1.60% | 1.59% | 1.67% |

| QoQ (%) | ||||||||||||||||

| Sales | -3% | 18% | 2% | -5% | -5% | 4% | 7% | -3% | -5% | 4% | 4% | -3% | ||||

| Gross profit | -6% | 17% | 4% | -6% | -7% | 7% | 8% | -3% | -8% | 8% | 6% | -3% | ||||

| Operating profit | -57% | 122% | 7% | 3% | -17% | 8% | 10% | 7% | -19% | 12% | 12% | 5% | ||||

| Pretax profit | -19% | 25% | 7% | -1% | -19% | 13% | 10% | 3% | -20% | 15% | 12% | 2% | ||||

| Net income | -34% | 105% | 7% | -1% | -52% | 88% | 11% | 4% | -51% | 89% | 13% | 3% | ||||

| YoY (%) | ||||||||||||||||

| Sales | 18% | 28% | 19% | 11% | 9% | -4% | 1% | 3% | 3% | 3% | 1% | 1% | 4% | 19% | 2% | 2% |

| Gross profit | 25% | 41% | 21% | 8% | 7% | -2% | 1% | 4% | 3% | 4% | 2% | 2% | 7% | 23% | 2% | 3% |

| Operating profit | -23% | 143% | 27% | 5% | 102% | -1% | 1% | 5% | 3% | 7% | 9% | 7% | 5% | 26% | 14% | 7% |

| Pretax profit | 84% | 23% | -13% | 8% | 9% | -2% | 1% | 5% | 3% | 6% | 7% | 6% | -15% | 14% | 3% | 6% |

| Net income | 36% | 33% | 39% | 43% | 6% | -3% | 1% | 5% | 6% | 6% | 8% | 7% | -32% | 38% | 2% | 7% |

Source: BofA Global Research estimates, company data

Exhibit 11: Acronyms and corresponding full forms

Acronyms

| Acronym | Acronym | Acronym | |||

|---|---|---|---|---|---|

| CAGR | Compound Annual Growth Rate | OPM | Operating Margin | PO | Price Objective |

| EPS | Earnings per share | Opex | Operating Expense | ROE | Return on Equity |

| GM | Gross Margin | P/B | Price to Book Value Ratio | S.D. | Standard Deviation |

| NB | Notebook | P/E | Price to Earnings Ratio | U/P | Underperform |

| NT$ | New Taiwan Dollar | PC | Personal Computer | US$ | US Dollar |

Source:

BofA Global Research

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Price objective basis & risk

Acer (ASIYF)

Our PO of NT$26 is based on 15x 2H26-1H27E EPS, which is around 0.5SD above the company's historical trading average since 2006 but excluding outliers in 2010-16, when Acer's PC market share started recovering to 6-7%, which is similar to current level. We apply this multiple in view of PC demand recovery in 2024-25 from 2022-23 downcycle, sales/profit supported by key non-PC subsidiaries, and Acer's strong cash position.

Upside risks to our PO are (1) Acer's stronger-than-expected revenue growth from better-margin gaming PC business, (2) more stringent opex control, and (3) higher revenue/profits contribution from subsidiaries.

Downside risks to our PO are (1) increasing competition in the gaming PC market, (2) execution risks in opex control, and (3) limited revenue/profits contribution from new subsidiaries.