PDF 原檔:報告_Nomura_環球晶6488_20260711_original.pdf

圖片清單(已驗證 2026-07-13)

報告_Nomura_環球晶6488_20260711_001.png(35KB)未 Read,<40KB 預設 logo,免列。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Nomura_環球晶6488_20260711_002.png |

44KB | 真資料圖 | GWC P/E 歷史走勢圖(紅線),橫軸 10/28/2014-10/28/2025,本益比約 5-40x 間循環 |

報告_Nomura_環球晶6488_20260711_003.png |

54KB | 真資料圖 | GWC P/B(紅線,左軸)與 ROE%(灰線,右軸)雙軸走勢圖,橫軸 10/28/2014-10/28/2025 |

報告_Nomura_環球晶6488_20260711_004.png |

119KB | 真資料圖 | GWC 三年評等與目標價變動歷史圖(股價線圖 + 目標價調整▲/評等變動●標記),右側附表列出 2023-07-24~2026-06-30 各次評等與目標價變動明細(含收盤價對照) |

原始內容

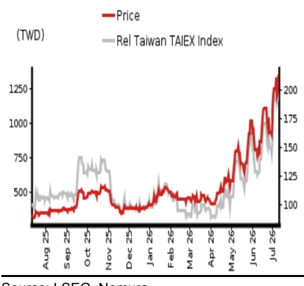

Relative performance chart

EQUITY: TECHNOLOGY

Price

(TWD)

1250-

1000-

7501

500-

-200

-175

-150

- 125.

GlobalWafers 6488.TWO 6488 TT

EQUITY: TECHNOLOGY

Courca. I CEC Namura

New LTA arrived earlier than anticipated

GWC's new 10-year LTA with Micron could cause semi wafer prices to potentially grow meaningfully

Maintain Buy on GWC with a new TP of TWD1,800; LTA implies upcycle is underway

On 9 July, Micron (MU US, Not rated) and GlobalWafers (GWC) announced that Micron would provide GWC with a USD500mn prepayment to secure the supply of 12″ semi wafers under a 10-year agreement (LTA). This LTA announcement came sooner than we anticipated, which in our view implies that: 1) memory companies have ample cash to secure upstream supply early; and 2) supply-demand dynamics could turn more favorable. As a result, we raise our 2026-28F earnings forecasts for GWC by 7-99%, and increase our TP to TWD1,800 (from TWD1,200), based on 6x 2028F BVPS of TWD300 (vs 4.8x 2028F BVPS of TWD252 previously). The stock is trading at 2.6x 2028F BVPS of TWD300. Historically, taking the 2H16-1H18 semi wafer upcycle as an example, LTAs were first negotiated from 1H27, implying the upcycle was underway, and the upcycle would not end until end demand weakened.

LTA pricing for semi wafers with memory customers could potentially double

We believe that LTA pricing for semi wafers supplied to memory customers could potentially double, as memory wafer price can reach tens of thousands of USD per piece, with semi wafers now only accounting for less than 1% of the memory wafer price vs 35% two years ago. However, in the case of the 10-year GWC-Micron LTA, considering the long contract period, we believe there is room for pricing and product spec mix to be adjusted over time. That said, if price hikes are implemented quickly/gradually over the contract period, GWC's earnings could recover sharply/steadily in the coming years.

Semi inflation is accelerating; GWC's customer base is optimizing

We believe this move of Micron could encourage other leading semi manufacturers with ample cash and strong demand from end customers to secure future strategic resources as capacity expansion is becoming increasingly critical - the earlier the spending, the lower the cost. As a result, this semi inflation trend is likely occurring across the entire semi supply chain. For GWC, this 10-year LTA has broken its previous 8-year LTA record and could help strengthen its customer base, as GWC's major memory customer has historically been Samsung (005930 KS, Buy), but Micron's engagement is likely also increasing. Possibly, other US semi companies such as Intel (INTC US, Not rated), TI (TXN US, Not rated), and GlobalFoundries (GFS US, Not rated) could engage more closely with GWC.

| Year-end 31 Dec Currency (TWD) | FY25 Actual | Old | FY26F New | Old | FY27F New | Old | FY28F New |

|---|---|---|---|---|---|---|---|

| Revenue (mn) | 60,598 | 61,726 | 62,931 | 73,535 | 83,063 | 88,666 | 113,936 |

| Reported net profit (mn) | 7,311 | 11,633 | 12,485 | 12,082 | 18,986 | 19,163 | 38,064 |

| Normalised net profit (mn) | 7,311 | 11,633 | 12,485 | 12,082 | 18,986 | 19,163 | 38,064 |

| FD normalised EPS | 15.36 | 24.33 | 26.11 | 25.27 | 39.71 | 40.08 | 79.61 |

| FD norm. EPS growth (%) | -29.8 | 58.4 | 70.0 | 3.9 | 52.1 | 58.6 | 100.5 |

| FD normalised P/E (x) | 87.9 | - | 51.7 | - | 34.0 | - | 17.0 |

| EV/EBITDA (x) | 47.0 | - | 46.3 | - | 23.6 | - | 12.2 |

| Price/book (x) | 6.9 | - | 6.4 | - | 5.7 | - | 4.5 |

| Dividend yield (%) | 0.5 | - | 0.9 | - | 1.3 | - | 1.7 |

| ROE (%) | 7.9 | 12.0 | 12.9 | 11.7 | 17.7 | 16.9 | 29.6 |

| Net debt/equity (%) | 7.1 | net cash | net cash | net cash | net cash | net cash | net cash |

Source: Company data, Nomura estimates

Global Markets Research 11 July 2026

| Rating Remains | Buy |

|---|---|

| Target price Increased from TWD 1,200.00 | TWD 1,800.00 |

| Closing price 9 July 2026 | TWD 1,350.00 |

| Implied upside | +33.3% |

| Market Cap (USD mn) | 20,085.7 |

| ADT (USD mn) | 193.3 |

Relative performance chart

Source: LSEG, Nomura

Research Analysts

Semiconductor

Donnie Teng - NIHK donnie.teng@nomura.com +852 2252 1439

Aaron Jeng, CFA - NITB

aaron.jeng@nomura.com +886(2) 21769962

Production Complete: 2026-07-11 18:32 UTC

Key data on GlobalWafers

Performance

| (%) | 1M | 3M | 12M | ||

|---|---|---|---|---|---|

| Absolute (TWD) | 68.1 | 201.7 | 339 | M cap (USDmn) | 20,085.7 |

| Absolute (USD) | 64.8 | 198.4 | 297.7 | Free float (%) | 27.5 |

| Rel to Taiwan TAIEX Index | 66.7 | 171.6 | 237.7 | 3-mth ADT (USDmn) | 193.3 |

Income statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

|---|---|---|---|---|---|

| Revenue | 62,626 | 60,598 | 62,931 | 83,063 | 113,936 |

| Cost of goods sold | -42,823 | -45,974 | -48,565 | -54,686 | -60,324 |

| Gross profit | 19,804 | 14,624 | 14,366 | 28,377 | 53,612 |

| SG&A | -3,365 | -3,770 | -4,063 | -4,984 | -6,449 |

| Employee share expense | -2,320 | -2,218 | -2,149 | -2,741 | -3,638 |

| Operating profit | 14,119 | 8,636 | 8,154 | 20,652 | 43,525 |

| EBITDA | 18,987 | 13,797 | 13,676 | 26,511 | 49,599 |

| Depreciation | -4,829 | -5,120 | -5,478 | -5,812 | -6,026 |

| Amortisation | -39 | -41 | -44 | -47 | -48 |

| EBIT | 14,119 | 8,636 | 8,154 | 20,652 | 43,525 |

| Net interest expense | 2,489 | 1,124 | 3,388 | 3,690 | 5,275 |

| Associates & JCEs | 186 | 85 | 15 | 0 | 0 |

| Other income | -4,364 | -329 | 4,365 | 0 | 0 |

| Earnings before tax | 12,429 | 9,516 | 15,922 | 24,342 | 48,800 |

| Income tax | -2,590 | -2,205 | -3,437 | -5,355 | -10,736 |

| Net profit after tax | 9,840 | 7,311 | 12,485 | 18,987 | 38,064 |

| Minority interests | 7 | 0 | 0 | 0 | 0 |

| Other items | 0 | 0 | 0 | 0 | 0 |

| Preferred dividends | 0 | 0 | 0 | 0 | 0 |

| Normalised NPAT | 9,847 | 7,311 | 12,485 | 18,986 | 38,064 |

| Extraordinary items | 0 | 0 | 0 | 0 | 0 |

| Reported NPAT | 9,847 | 7,311 | 12,485 | 18,986 | 38,064 |

| Dividends | -5,259 | -3,290 | -5,618 | -8,544 | -11,107 |

| Transfer to reserves | 4,588 | 4,021 | 6,867 | 10,443 | 26,956 |

| Valuations and ratios | |||||

| Reported P/E (x) | 61.0 | 87.9 | 51.7 | 34.0 | 17.0 |

| Normalised P/E (x) | 61.0 | 87.9 | 51.7 | 34.0 | 17.0 |

| FD normalised P/E (x) | 61.6 | 87.9 | 51.7 | 34.0 | 17.0 |

| Dividend yield (%) | 0.8 | 0.5 | 0.9 | 1.3 | 1.7 |

| Price/cashflow (x) | 23.4 | - | 13.9 | 30.6 | 16.7 |

| Price/book (x) | 7.1 | 6.9 | 6.4 | 5.7 | 4.5 |

| EV/EBITDA (x) | 33.6 | 47.0 | 46.3 | 23.6 | 12.2 |

| EV/EBIT (x) | 45.0 | 74.8 | 77.6 | 30.3 | 13.9 |

| Gross margin (%) | 31.6 | 24.1 | 22.8 | 34.2 | 47.1 |

| EBITDA margin (%) | 30.3 | 22.8 | 21.7 | 31.9 | 43.5 |

| EBIT margin (%) | 22.5 | 14.3 | 13.0 | 24.9 | 38.2 |

| Net margin (%) | 15.7 | 12.1 | 19.8 | 22.9 | 33.4 |

| Effective tax rate (%) | 20.8 | 23.2 | 21.6 | 22.0 | 22.0 |

| Dividend payout (%) | 53.4 | 45.0 | 45.0 | 45.0 | 29.2 |

| ROE (%) | 12.5 | 7.9 | 12.9 | 17.7 | 29.6 |

| ROA (pretax %) | 8.2 | 4.5 | 4.2 | 10.8 | 21.8 |

| Growth (%) | |||||

| Revenue | -11.4 | -3.2 | 3.8 | 32.0 | 37.2 |

| EBITDA | -24.0 | -27.3 | -0.9 | 93.9 | 87.1 |

| Normalised EPS | -51.8 | -30.6 | 70.0 | 52.1 | 100.5 |

| Normalised FDEPS | -51.8 | -29.8 | 70.0 | 52.1 | 100.5 |

Source: Company data, Nomura estimates

Cashflow statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F | FY28F |

|---|---|---|---|---|---|---|

| EBITDA | 18,987 | 13,797 | 13,676 | 26,511 | 49,599 | 49,599 |

| Change in working capital | 11,289 | -28,021 | 28,325 | -3,759 | -5,450 | -5,450 |

| Other operating cashflow | -4,298 | -1,297 | 4,332 | -1,666 | -5,461 | -5,461 |

| Cashflow from operations expenditure | 25,978 -48,319 | -15,520 | 46,334 | 21,086 -20,956 | 38,688 -17,398 | 38,688 -17,398 |

| Capital | -33,130 | -25,033 | 130 | 21,290 | 21,290 | |

| Free cashflow | -22,342 | -48,650 | 21,301 | |||

| Reduction in investments | -6,052 | 498 | -127 | 0 | 0 | 0 |

| Net acquisitions | 0 | 0 | 0 | 0 | 0 | 0 |

| Dec in other LT assets | 4,302 | 39,845 | 14,538 | 13,418 | 8,679 | 8,679 |

| Inc in other LT liabilities | 0 | 0 | 0 | 0 | ||

| Adjustments | 0 | 0 | 0 | 0 | 0 | 0 |

| CF after investing acts | -24,092 | -8,307 | 35,711 | 13,548 | 29,969 | 29,969 |

| Cash dividends | -8,748 | -5,259 | -3,290 | -5,618 | -8,544 | -8,544 |

| Equity issue | 0 | 0 | 0 | 0 | 0 | 0 |

| 9,776 | -11,511 | -7,141 | 0 | 0 | 0 | |

| Debt issue Convertible | 0 | 0 | 0 | |||

| debt issue Others | 35,829 | 5,632 | -14,495 | 0 | 0 | 0 |

| CF from financial | acts 36,857 | -11,139 | -24,927 | 0 -5,618 | 0 -8,544 | 0 -8,544 |

| Net cashflow | 12,765 | -19,445 | 10,784 | 7,930 | 21,425 | 21,425 |

| Beginning cash | 26,165 | 38,929 | 19,484 | 30,268 | 38,198 | 38,198 |

| Ending cash | 38,929 | 19,484 | 30,268 | 38,198 | 59,623 | 59,623 |

| Ending net debt | ||||||

| (TWDmn) | -1,282 | -19,203 | ||||

| Balance sheet As at 31 Dec | 6,652 | -11,273 FY24 FY25 FY26F | FY27F | -40,628 FY28F | -40,628 FY28F | |

| Cash & equivalents Marketable securities | 38,929 29 | 1 10,113 | 19,484 30,268 0 10,066 | 38,198 0 13,558 | 59,623 0 18,751 | 59,623 0 18,751 |

| Accounts receivable Inventories | 10,265 | 10,148 | 11,090 | 12,114 | 12,114 | |

| Other current | 11,238 | 10,399 | 31,636 | 31,636 | 31,636 | |

| assets Total current assets | 20,030 80,492 | 46,632 86,629 | 31,636 94,481 | 122,123 | 122,123 | |

| LT investments | 7,445 | 6,947 | 82,118 7,074 | 7,074 | 7,074 | 7,074 |

| Fixed assets | 119,074 0 | 107,241 | 111,560 | 113,239 | 115,885 | 115,885 |

| Goodwill | 0 | 0 | 0 | 0 | 0 | |

| Other intangible assets | 0 | 0 | 0 | 0 | 0 | |

| Other LT assets | 0 17,570 | 18,179 | 18,179 | 18,179 | 18,179 | |

| Total assets | 224,581 | 17,525 218,343 | 218,932 | 232,975 | 263,261 | 263,261 |

| Short-term debt | 27,117 | 18,571 | 14,252 | 14,252 | 14,252 | 14,252 |

| Accounts | 5,371 | 4,464 | 5,138 | 5,905 | 5,905 | |

| payable Other current | 4,161 | 44,105 | 44,105 | 44,105 | 44,105 | |

| liabilities Total current liabilities | 32,577 | 31,377 54,109 | 62,821 | 63,495 | 64,262 | 64,262 |

| Long-term debt | 65,065 | 7,565 | 4,743 | 4,743 | 4,743 | |

| Convertible debt | 10,531 0 | 0 | 0 | 4,743 0 | 0 | 0 |

| Other LT liabilities | 57,958 | 63,374 125,048 | 50,690 118,254 | 50,690 118,929 | 50,690 119,695 | 50,690 119,695 |

| Total liabilities | 133,553 | -4 | -4 | |||

| Minority interest | -3 | -3 | -4 | -4 0 | 0 | 0 |

| Preferred stock | 0 | 0 | 0 | |||

| Common stock | 4,781 | 4,781 | 4,781 | 4,781 | 4,781 78,991 | 4,781 78,991 |

| Retained earnings | 37,451 3,290 | 41,592 5,618 | 52,035 8,544 | 11,107 | 11,107 | |

| Proposed dividends | 31,640 5,259 | |||||

| Other equity and | 49,350 | 47,776 | 48,690 | 48,690 114,049 | 48,690 143,569 | 48,690 143,569 |

| reserves Total shareholders' equity | 91,030 | 93,298 | 100,681 | |||

| Total equity & liabilities | 224,580 | 218,342 | 232,975 | 263,261 | 263,261 | |

| Liquidity (x) | ||||||

| 218,932 | ||||||

| - net cash | 0.48 7.1 | 1.24 1.60 1.31 - - | 1.49 - net cash net cash | 1.90 - | 1.90 - | |

| Current ratio Interest cover Leverage | net cash | net cash net cash | net cash net cash | net cash net cash | ||

| Net debt/EBITDA (x) Net debt/equity (%) Per share | 22.14 22.14 | 15.36 | 26.11 | 39.71 | 79.61 | 79.61 |

| Reported EPS (TWD) Norm EPS (TWD) FD norm EPS (TWD) | 21.90 190.39 | 15.36 195.14 | 15.36 26.11 26.11 | 39.71 238.54 | 79.61 79.61 300.28 | 79.61 79.61 300.28 |

| BVPS (TWD) DPS (TWD) | 11.00 | 6.88 | ||||

| 39.71 | ||||||

| 210.58 | ||||||

| Activity | 11.75 | 17.87 | 23.23 | 23.23 | ||

| 61.4 | 58.5 77.2 | 51.9 70.9 | 51.9 70.4 | 51.9 70.4 | ||

| (days) Days receivable | 59.4 | 85.9 | 32.4 | 33.5 | 33.5 | |

| Days inventory Days payable | 87.8 44.3 | 37.8 | ||||

| Cash cycle | 109.4 | 32.0 | ||||

| 102.9 | 103.3 | |||||

| 88.8 | 88.8 | |||||

| 90.7 |

Source: Company data, Nomura estimates

Company profile

GlobalWafers is the world's third-largest and largest non-Japanese wafer manufacturer that specializing in 3' to 12' silicon wafer manufacturing, possessing a complete production line from ingot growth, slicing, etching, diffusion, polishing and epitaxy.

Valuation Methodology

Our TP of TWD1800 is based on 6x 2028F BVPS TWD300. The 6x P/B is based on the high-end of 2-6x P/B range during the full Semi wafer cycle in 2017-2020. The benchmark index is TAIEX.

Risks that may impede the achievement of the target price

Downside risks include: · Faster-than-expected entry of China into the 12' semi wafer market. · Slower-than-expected of market consolidation. · Worse-than-expected end-demand for the semi industry. · Less favorable demand/supply dynamics in the semi wafer industry. · Less favorable FX volatility and rising material/utility costs.

ESG

In response to global climate change and latest development trends in corporate social responsibilities (CSR), GlobalWafers has taken the initiative to compile a CSR report. Based on long-term in-depth interactions with local communities and engagement with stakeholders, GlobalWafers discloses in the report relevant information on material issues regarding the four aspects of corporate governance, economy, environment, and society, as well as execution & improvement results, in addition to presenting the the future vision and goals in terms of sustainable development.

Net Sales

(TWD mn)

Previous

2Q25

3Q25

4Q25

2026F

16,008

1Q26

13,985

2Q26F 3Q26F

4Q26F

2027F

15,396

Revised Change (%; pp) Previous

14,493

14,502

Earnings forecast revisions

2026F

2025

60,598

16,137

3,208

1,669

83,063

17,414

13.0

50.5

2,875

6,445

28,342

2028F

2027F

62,931

83,063

88,666

Revised Change (%; pp)

Revised Change (%; pp) Previous

28.5

28,377

8, 154

113,936

14,366

20,652

15,922

53,612

28,377

2,135

4,512

3,884

We revise up our 2026-28F earnings forecasts by 7-99%. We expect a moderate revenue recovery in 2026F, but believe revenues will accelerate from 2H26F onward, as well as a more favorable supply-demand environment in 2027-28F. YTD 2026, GWC has also recognized meaningful non-operating gains from its investment in Siltronic (WAF GR, Not rated) due to the sharp rise in Siltronic's share price. We have not yet factored any Siltronic share price impact into our forecasts from 2H26F onward. 5.30 12.1% 15.36

In the near term, we believe GWC's profitability is still under pressure due to rising depreciation costs from new capacity expansion, but as market demand continues to grow, we believe price hike potential is also likely to increase. 27.9% 34.7%

Fig. 1: GWC: earnings estimate revisions

Net Sales

Gross profit

Op income

Pretax income

Net income

-19.3%

-14.0%

174.7%

165.2%

-49.6%

49.6%

19.6%

19.6%

| 3.4% | -8.7% -11.3% -10.3% | -8.7% -11.3% -10.3% | -8.7% -11.3% -10.3% | 11.3% 20.1% -3.2% | 11.3% 20.1% -3.2% | 11.3% 20.1% -3.2% | 32.0% 37.2% | 32.0% 37.2% | 32.0% 37.2% |

|---|---|---|---|---|---|---|---|---|---|

| -20.4% -16.7% | -44.2% | -24.2% | -29.1% -22.2% | 40.2% | 21.1% -26.2% | -1.8% | 97.5% | 88.9% | |

| -34.7% | -27.6% | 61.6% -33.6% | 43.0% | -31.6% | 73.6% 20.8% | -38.8% | -5.6% | 153.3% | 110.8% |

| -53.2% | -35.2% | -38.3% 265.2% | 10.0% | 181.6% | 48.4% 33.6% | -23.4% | 67.3% | 52.9% | 100.5% |

| -58.8% | 41.6% | -33.3% 360.5% | 30.2% | 198.9% | 28.6% 37.4% | -25.7% | 70.7% | 52.1% | 100.5% |

Source: Nomura estimates

Fig. 2: GWC: P&L

Source: Company data, Nomura estimates

Valuation methodology and risks

Our new TP of TWD1,800 is based on 6x 2028F BVPS of TWD300. The 6x target multiple is at the high-end of the historical P/B range of 2-6x during the full semi wafer cycle in 2017-20.

24,342

12,485

43,525

18,986

38,064

48,800

22.8%

79.6

34.2%

13.0%

25.3%

24.9%

23.1

47.1

29.3%

38.2

19.8%

21.6

26.11

39.71

33.4

22.9%

53,612

89.2

43,525

48,800

112.5

98.6

38,064

98.6

98.6

47.1%

38.2%

42.8%

15.1

15.1

79.61

33.4%

11.8

14,624

3,732

8,636

EPS

EPS

45

40

35

30

25

20

15

10

5

10/28/2014

Downside risks include:

9

8

7

6

- Faster-than-expected entry of China into the 12' semi wafer market.

- Slower-than-expected of market consolidation.

4

3

- Worse-than-expected end-demand for the semi industry.

2

- Less favorable demand/supply dynamics in the semi wafer industry.

- Less favorable FX volatility and rising material/utility costs.

Fig. 3: GWC: P/E

GWC P/E

Source: Company data, Nomura estimates ywim

10/28/2017

10/28/2018

10/28/2019

10/28/2020

10/28/2021

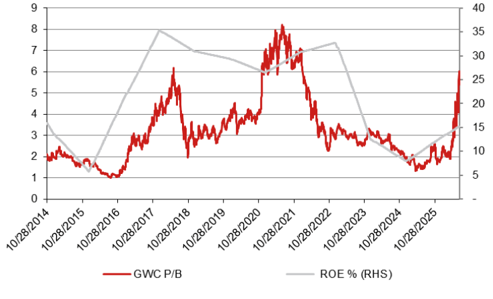

Fig. 4: GWC: P/B

10/28/2022

10/28/2023

10/28/2024

10/28/2025

ROE % (RHS)

Source: Company data, Nomura estimates

35

30

25

20

15

10

5

Rating and target price chart (three year history)

GlobalWafers

Appendix A-1

30

21

21

05

05

24

This report has been produced by Nomura International (Hong Kong) Ltd. (NIHK), Hong Kong. See Disclaimers for Nomura Group entity details.