PDF 原檔:報告_Nomura_大立光3008_20260709_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

_002.png |

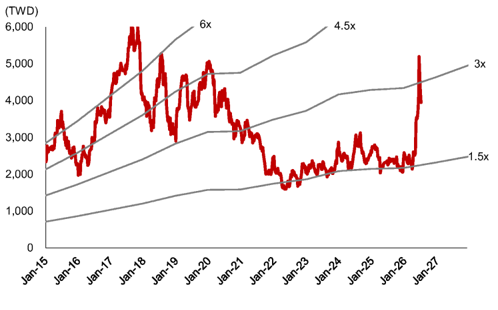

48124 | 真資料圖 | Largan P/E band 圖(Jan-15~Jan-27),股價疊加 1.5x/3x/4.5x/6x 四條本益比線 |

_003.png |

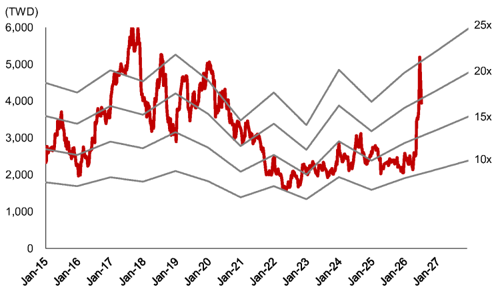

57467 | 真資料圖 | Largan P/B band 圖(Jan-15~Jan-27),股價疊加 10x/15x/20x/25x 四條本淨比線 |

_004.png |

132725 | 真資料圖 | Largan 評等與目標價三年歷史圖+表格:列出 2023-10~2026-06 共 9 筆 TP 調整紀錄,最新一筆 2026-06-08 TP NT$4,310 |

_001.png(39190B,<40KB)未逐張驗證,依規則預設略過。

原始內容

Relative performance chart

EQUITY: HANDSETS

Price

(TWD)

5000-

4500-

4000-

35001

30001

25001

2000

-110

- 100

÷ 90.

-80

Largan Precision

3008.TW 3008 TT

EQUITY: HANDSETS

Churra. I CEC Namura

Faster progress in CPO FA

More concrete progress in CPO components to mark a step closer to mass production; maintain Buy

Action: Maintain Buy; TP raised to TWD6,000, implying ~52% upside

We believe Largan's conviction in fiber array (FA) mass production has become stronger than it was during the COMPUTEX (report ). We fine-tune our 2026/27F earnings by -2.4%/-2.4% as we bake in FX fluctuations, and recent price hikes by Apple (AAPL US, Not rated) for its end products temporarily hurting demand; however, we raise our 2028F earnings by 2.3% to reflect an accelerated pace of iPhone camera/lens upgrades from 2H27F to 2028F. We maintain our Buy rating and raise TP to TWD6,000, based on 25x 2028F EPS of TWD240.0 (previously: TWD4,310, based on 20x 2027F EPS of TWD215.5). We shift our valuation base to 2028F, as we believe visibility on more camera/lens upgrades in iPhones has improved, and thus raise our target P/E from 20x to 25x to reflect Largan's better-than-expected progress on CPO FA mass production. The target P/E of 25x is at the high end of the stock's historical trading band (10-25x) since 2015. Largan trades at 18x 2027F P/E.

One anchor client for CPO FA, likely mass production by mid-2027F at the earliest

Largan has secured one client for one-row FA product, aiming to kick off a pilot run by Sep 2026E. The mass production could start in mid-2027 at the earliest, and Largan plans to leverage its full automation capability to help with volume scale-up and more efficient troubleshooting as well as high-precision alignment for FA. Engagements with other clients at this moment are primarily PoC for next-gen products. Largan has noted that its focus is on grating coupling (GC) FA, and that it is unaffected by Corning's (GLW US, Not rated) GlassBridge for edge coupling (EC); Largan believes GC is the mainstream design route.

Largan also has prism/microlens array (PMLA) for CPO based on molding glass, but it appears to have a lower priority than FA. The company notes that molding glass offers less insertion loss than metalens alternatives but acknowledges another competitive prism solution on quartz glass using semiconductor-grade fabrication to demonstrate a better cost structure and absence of thermal effect.

More intense iPhone camera/lens upgrades in 2027-28F

Beyond variable aperture (VA) adoption in flagship iPhone main camera in 2026F, we expect an enhanced VA camera in 2027F in which Largan could address blades on top of lens, and the main camera may further improve the resolution in 2028F. We also expect a more complicated periscope camera designs in 2027F to enable inner zooming with higher resolutions, and Largan should benefit from its technology leadership.

| Year-end 31 Dec | FY25 | FY26F | FY27F New | Old | FY28F New | ||

|---|---|---|---|---|---|---|---|

| Currency (TWD) | Actual | Old | New | Old | |||

| Revenue (mn) | 61,148 | 66,520 | 65,936 | 74,234 | 72,266 | 79,402 | 80,815 |

| Reported net profit (mn) | 21,275 | 25,583 | 24,968 | 28,764 | 28,070 | 30,690 | 31,381 |

| Normalised net profit (mn) | 21,275 | 25,583 | 24,968 | 28,764 | 28,070 | 30,690 | 31,381 |

| FD normalised EPS | 159.40 | 191.68 | 190.75 | 215.51 | 214.68 | 229.94 | 240.01 |

| FD norm. EPS growth (%) | -17.9 | 20.2 | 19.7 | 12.4 | 12.5 | 6.7 | 11.8 |

| FD normalised P/E (x) | 24.8 | - | 20.7 | - | 18.4 | - | 16.5 |

| EV/EBITDA (x) | 12.8 | - | 11.5 | - | 9.9 | - | 8.5 |

| Price/book (x) | 2.8 | - | 2.8 | - | 2.6 | - | 2.4 |

| Dividend yield (%) | 2.2 | - | 2.4 | - | 2.8 | - | 3.2 |

| ROE (%) | 11.4 | 13.4 | 13.1 | 14.5 | 14.2 | 14.5 | 14.8 |

| Net debt/equity (%) | net cash | net cash | net cash | net cash | net cash | net cash | net cash |

Source: Company data, Nomura estimates

Global Markets Research 9 July 2026

| Rating Remains | Buy |

|---|---|

| Target price Increased from TWD 4,310.00 | TWD 6,000.00 |

| Closing price 9 July 2026 | TWD 3,950.00 |

| Implied upside | +51.9% |

| Market Cap (USD mn) | 16,077.6 |

| ADT (USD mn) | 285.1 |

Relative performance chart

Source: LSEG, Nomura

Research Analysts

Taiwan Technology/Hardware

Anne Lee, CFA - NITB anne.lee@nomura.com +886(2) 21769966

Eric Chen, CFA - NITB

eric.chen@nomura.com +886(2) 21769965

Carol Hu - NITB

carol.r.hu@nomura.com +886(2) 21769963

Production Complete: 2026-07-09 11:26 UTC

Key data on Largan Precision

Performance

| (%) | 1M | 3M | 12M | ||

|---|---|---|---|---|---|

| Absolute (TWD) | 1.7 | 73.2 | 80.8 | M cap (USDmn) | 16,077.6 |

| Absolute (USD) | -0.3 | 71.3 | 63.7 | Free float (%) | 69.6 |

| Rel to Taiwan TAIEX Index | -0.6 | 42.1 | -22.2 | 3-mth ADT (USDmn) | 285.1 |

Income statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

|---|---|---|---|---|---|

| Revenue | 59,458 | 61,148 | 65,936 | 72,266 | 80,815 |

| Cost of goods sold | -28,248 | -30,311 | -32,746 | -34,859 | -38,775 |

| Gross profit | 31,209 | 30,837 | 33,190 | 37,407 | 42,040 |

| SG&A | -7,177 | -7,279 | -7,783 | -8,393 | -8,932 |

| Employee share expense | 0 | 0 | 0 | 0 | 0 |

| Operating profit | 24,033 | 23,558 | 25,407 | 29,013 | 33,108 |

| EBITDA | 30,262 | 31,290 | 34,349 | 39,022 | 44,184 |

| Depreciation | -6,230 | -7,732 | -8,942 | -10,009 | -11,076 |

| Amortisation | 0 | 0 | 0 | 0 | 0 |

| EBIT | 24,033 | 23,558 | 25,407 | 29,013 | 33,108 |

| Net interest expense | 4,404 | 4,259 | 4,370 | 4,800 | 4,800 |

| Associates & JCEs | 117 | 212 | 89 | 80 | 80 |

| Other income | 3,621 | -2,129 | 807 | 800 | 800 |

| Earnings before tax | 32,174 | 25,900 | 30,674 | 34,693 | 38,788 |

| Income tax | -5,963 | -4,340 | -5,600 | -6,624 | -7,407 |

| Net profit after tax | 26,211 | 21,560 | 25,074 | 28,070 | 31,381 |

| Minority interests | -296 | -285 | -105 | 0 | 0 |

| Other items | 0 | 0 | 0 | 0 | 0 |

| Preferred dividends | 0 | 0 | 0 | 0 | 0 |

| Normalised NPAT | 25,915 | 21,275 | 24,968 | 28,070 | 31,381 |

| Extraordinary items | 0 | 0 | 0 | 0 | 0 |

| Reported NPAT | 25,915 | 21,275 | 24,968 | 28,070 | 31,381 |

| Dividends | -10,811 | -11,412 | -12,446 | -14,894 | -16,762 |

| Transfer to reserves | 15,104 | 9,864 | 12,522 | 13,176 | 14,619 |

| Valuations and ratios | |||||

| Reported P/E (x) | 20.3 | 24.8 | 20.7 | 18.4 | 16.5 |

| Normalised P/E (x) | 20.3 | 24.8 | 20.7 | 18.4 | 16.5 |

| FD normalised P/E (x) | 20.3 | 24.8 | 20.7 | 18.4 | 16.5 |

| Dividend yield (%) | 2.1 | 2.2 | 2.4 | 2.8 | 3.2 |

| Price/cashflow (x) | 16.7 | 20.2 | 17.2 | 16.0 | 14.6 |

| Price/book (x) | 2.9 | 2.8 | 2.8 | 2.6 | 2.4 |

| EV/EBITDA (x) | 13.3 | 12.8 | 11.5 | 9.9 | 8.5 |

| EV/EBIT (x) | 16.8 | 16.9 | 15.6 | 13.3 | 11.4 |

| Gross margin (%) | 52.5 | 50.4 | 50.3 | 51.8 | 52.0 |

| EBITDA margin (%) | 50.9 | 51.2 | 52.1 | 54.0 | 54.7 |

| EBIT margin (%) | 40.4 | 38.5 | 38.5 | 40.1 | 41.0 |

| Net margin (%) | 43.6 | 34.8 | 37.9 | 38.8 | 38.8 |

| Effective tax rate (%) | 18.5 | 16.8 | 18.3 | 19.1 | 19.1 |

| Dividend payout (%) | 41.7 | 53.6 | 49.8 | 53.1 | 53.4 |

| ROE (%) | 14.8 | 11.4 | 13.1 | 14.2 | 14.8 |

| ROA (pretax %) | 25.4 | 22.9 | 23.2 | 24.9 | 27.3 |

| Growth (%) | |||||

| Revenue | 21.7 | 2.8 | 7.8 | 9.6 | 11.8 |

| EBITDA | 30.3 | 3.4 | 9.8 | 13.6 | 13.2 |

| Normalised EPS | 44.8 | -17.9 | 19.7 | 12.5 | 11.8 |

| Normalised FDEPS | 44.8 | -17.9 | 19.7 | 12.5 | 11.8 |

Source: Company data, Nomura estimates

Cashflow statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F | FY28F |

|---|---|---|---|---|---|---|

| EBITDA | 30,262 | 31,290 | 34,349 | 39,022 | 44,184 | 44,184 |

| Change in working capital | -948 | -1,472 | 6,659 | -2,205 | -1,949 | -1,949 |

| Other operating cashflow | 2,264 | -3,738 | -10,883 | -4,472 32,345 | -6,856 35,378 | -6,856 35,378 |

| Cashflow from operations expenditure | 31,579 | 26,080 | 30,126 | -8,000 | -8,000 | |

| Capital | -11,126 | -12,338 | -8,341 | -8,000 | ||

| Free cashflow | 20,453 | 13,743 | 21,785 | 24,345 | 27,378 | 27,378 |

| Reduction in investments | -7,374 | -1,704 | -1,022 | 0 | 0 | 0 |

| Net acquisitions | 0 | 0 | 0 | 0 | 0 | 0 |

| Dec in other LT assets liabilities | 0 | 0 | 0 | 0 | 0 | 0 |

| Inc in other LT Adjustments | 0 | 0 | 0 | 0 | 0 | 0 |

| 2,434 | 4,805 | 951 | 0 | 0 | 0 | |

| CF after investing acts | 15,512 | 16,845 | 21,714 | 24,345 | 27,378 | 27,378 |

| Cash dividends | -10,811 | -11,412 | -12,446 | -14,894 | -16,762 | -16,762 |

| Equity issue | 0 | 0 | 0 | 0 | 0 | 0 |

| Debt issue | 212 | -212 | 0 | 0 | 0 | 0 |

| Convertible debt issue | 0 | 0 | 0 | 0 | 0 | 0 |

| Others | 1,255 | -2,937 | -3,824 | 0 | 0 | 0 |

| CF from financial | acts -9,344 | -14,561 | -16,270 | -14,894 | -16,762 | -16,762 |

| Net cashflow | 6,168 | 2,283 | 5,444 | 9,451 | 10,616 | 10,616 |

| Beginning cash | 107,490 | 113,658 | 115,942 | 121,386 | 130,837 | 130,837 |

| Ending cash | 113,658 | 115,942 | 121,386 | 130,837 | 141,453 | 141,453 |

| Ending net debt | -115,942 | -130,837 | -141,453 | -141,453 | ||

| As at 31 Dec | -113,455 | |||||

| -121,386 | ||||||

| Balance sheet (TWDmn) | FY24 | FY25 | FY26F | FY27F | FY28F 141,453 | FY28F 141,453 |

| Marketable securities Accounts receivable | 9,961 11,307 | 15,353 11,454 | 16,941 14,115 | 16,941 15,859 | 16,941 17,364 | 16,941 17,364 |

| Inventories | 5,733 5,105 | 6,713 4,823 | 10,406 5,048 | 11,431 5,048 | 12,419 5,048 | 12,419 5,048 |

| Other current assets | 145,764 | 167,896 | 180,115 | 193,225 | 193,225 | |

| Total current assets LT investments | 12,460 | 154,285 8,517 | 9,984 | 10,064 | 10,144 | 10,144 |

| Fixed assets | 46,936 0 | 51,472 | 50,974 | 48,965 0 | 45,889 | 45,889 |

| Goodwill | 0 | 0 | 0 | 0 | ||

| Other intangible assets | 0 | 0 | 0 | 0 | 0 | |

| Other LT assets | 0 11,367 | 6,512 | 7,434 | 10,885 | 15,936 | 15,936 |

| Total assets | 216,527 | 220,787 | 236,288 | 250,029 | 265,194 | 265,194 |

| Short-term debt | 203 | 0 | 0 | 0 | 0 | 0 |

| Accounts payable | 25,100 | 33,258 | 33,258 | 33,258 | 33,258 | |

| Other current | 25,243 4,506 | 9,727 | 10,291 | 10,834 | 10,834 | |

| liabilities Total current liabilities | 5,275 | 29,749 | 42,986 | 43,549 | 44,093 | 44,093 |

| Long-term debt | 30,578 | 0 | 0 | 0 | 0 | 0 |

| 0 | 0 | 0 | 0 | 0 | ||

| Convertible debt Other LT liabilities | 0 561 | 0 171 | 228 | 230 43,779 | 232 | 232 |

| Total liabilities | 31,139 | 29,919 | 43,214 | 44,325 | 44,325 | |

| Minority interest | 1,869 | 2,001 | 2,110 | 2,110 | 2,110 | 2,110 |

| Preferred stock | 0 | 0 | 0 | 0 | 0 | 0 |

| Common stock | 1,335 | 1,335 | 1,335 | 1,335 | 1,335 | 1,335 |

| Retained earnings | 148,623 | 153,570 | 155,702 | 168,878 | 183,497 | 183,497 |

| Proposed dividends | 0 | 0 | 0 33,927 | 0 | 0 33,927 | 0 33,927 |

| Other equity and reserves | 33,561 | 33,963 | 33,927 204,140 | 218,759 | 218,759 | |

| Total shareholders' equity | 183,519 | 188,867 | 190,964 | |||

| Total equity & liabilities | 216,527 | 250,029 | ||||

| Liquidity (x) | 3.91 | 4.77 | 4.14 | 4.38 | ||

| 220,787 | ||||||

| 5.19 | 236,288 | 265,194 | 265,194 | |||

| Current ratio Interest cover | net cash net cash | - net cash cash | - - net cash net | net cash net | - net cash net cash | - |

| Leverage Net debt/EBITDA Net debt/equity | (x) | net | cash | cash | ||

| (%) Per share Reported EPS (TWD) Norm EPS (TWD) | 194.17 194.17 194.17 | 159.40 159.40 159.40 | 190.75 190.75 | 214.68 214.68 214.68 | 240.01 240.01 240.01 | 240.01 240.01 240.01 |

| FD norm EPS (TWD) BVPS (TWD) DPS (TWD) | 1,375.00 | 1,415.07 | 190.75 1,430.78 | 1,529.50 | 1,639.03 | 1,639.03 |

| 85.50 | ||||||

| 81.00 | 125.59 | 125.59 | ||||

| Activity (days) | 93.25 | 111.59 | ||||

| 68.7 | 70.8 | 75.7 | 75.2 | 75.2 | ||

| 67.9 74.9 | 95.4 | 114.3 | 112.6 | 112.6 | ||

| Days receivable Days inventory | 66.7 | 303.1 | 313.9 | 313.9 | ||

| Days payable | 313.2 | 326.0 | 348.2 | |||

| Cash cycle | -177.8 | -160.2 | -159.9 | |||

| -158.2 | ||||||

| -126.1 | -126.1 |

Source: Company data, Nomura estimates

Company profile

Largan is a technology leader in handset camera lenses, and is currently Top 2 plastic lens maker in the world.

Valuation Methodology

Our TP of TWD6,000 is based on 25x 2028F EPS of TWD240. Our target P/E of 25x is at the high end of the historical trading range of 10-25x since 2015. The benchmark index for the stock is TAIEX.

Risks that may impede the achievement of the target price

Downside risks: 1) weaker-than-expected sales of iPhones and Android phones; 2) level of inventory correction by Chinese customers; 3) higherthan-expected ASP/margin erosion; 4) slower-than-expected spec upgrades; 5) increased competition, causing market share loss; and 6) worsethan-expected production yields.

ESG

Largan focuses on resource recycling and voluntarily reported green house gas emission through attending ISO14064 in 2020. Largan has achieved 90%+ water recycling and targets to save 1% electricity every year.

uZjWnViZtZbWaVoXlZaQ9RaQtRrRmOsMiNpPqPkPrQnN7NoPsPNZoOmNvPmPtP

Fig. 1: Largan - 2Q26 results

| TWDmn | 2Q26 results | Nomura forecast | Diff% | 2Q26 Consensus | Diff% | 1Q26 | q-q | 2Q25 | y-y |

|---|---|---|---|---|---|---|---|---|---|

| Total revenue | 13,665 | 13,803 | (1.0) | 13,403 | 2.0 | 15,544 | (12.1) | 11,673 | 17.1 |

| Gross profit | 6,752 | 6,746 | 0.1 | 6,678 | 1.1 | 7,680 | (12.1) | 6,260 | 7.9 |

| Operating profit | 5,148 | 5,040 | 2.1 | 5,081 | 1.3 | 5,812 | (11.4) | 4,879 | 5.5 |

| Pretax profit | 6,099 | 6,460 | (5.6) | 6,143 | (0.7) | 7,288 | (16.3) | 1,794 | 240.0 |

| Net profit | 4,670 | 4,962 | (5.9) | 4,792 | (2.6) | 6,123 | (23.7) | 1,032 | 352.5 |

| EPS (TWD) | 35.7 | 37.2 | (3.9) | 36.1 | (1.0) | 46.6 | (23.4) | 7.7 | 361.9 |

| Margins (%) | (ppt) | (ppt) | |||||||

| Gross margin | 49.4 | 48.9 | 0.5 | 49.8 | (0.4) | 49.4 | 0.0 | 53.6 | (4.2) |

| Operating margin | 37.7 | 36.5 | 1.2 | 37.9 | (0.2) | 37.4 | 0.3 | 41.8 | (4.1) |

| Pretax margin | 44.6 | 46.8 | (2.2) | 45.8 | (1.2) | 46.9 | (2.3) | 15.4 | 29.3 |

| Net margin | 34.2 | 36.0 | (1.8) | 35.8 | (1.6) | 39.4 | (5.2) | 8.8 | 25.3 |

Source: Company data, Bloomberg Finance L.P., Nomura estimates

Fig. 2: Largan - earnings forecast revisions

| New forecasts | New forecasts | New forecasts | Previous forecasts | Previous forecasts | Previous forecasts | Change (%) | Change (%) | Change (%) | |

|---|---|---|---|---|---|---|---|---|---|

| TWDmn | 2026F | 2027F | 2028F | 2026F | 2027F | 2028F | 2026F | 2027F | 2028F |

| Revenue | 65,936 | 72,266 | 80,815 | 66,520 | 74,234 | 79,402 | (0.9) | (2.7) | 1.8 |

| Gross profit | 33,190 | 37,407 | 42,040 | 33,613 | 38,365 | 41,155 | (1.3) | (2.5) | 2.2 |

| Operating profit | 25,407 | 29,013 | 33,108 | 25,692 | 29,889 | 32,299 | (1.1) | (2.9) | 2.5 |

| Pretax profit | 30,674 | 34,693 | 38,788 | 31,428 | 35,569 | 37,979 | (2.4) | (2.5) | 2.1 |

| Net profit | 24,968 | 28,070 | 31,381 | 25,583 | 28,764 | 30,690 | (2.4) | (2.4) | 2.3 |

| EPS (TWD) | 190.8 | 214.7 | 240.0 | 191.7 | 215.5 | 229.9 | (0.5) | (0.4) | 4.4 |

| Margins (%) | |||||||||

| Gross margin | 50.3 | 51.8 | 52.0 | 50.5 | 51.7 | 51.8 | (0.2) | 0.1 | 0.2 |

| Operating margin | 38.5 | 40.1 | 41.0 | 38.6 | 40.3 | 40.7 | (0.1) | (0.1) | 0.3 |

| Pretax margin | 46.5 | 48.0 | 48.0 | 47.2 | 47.9 | 47.8 | (0.7) | 0.1 | 0.2 |

| Net margin | 37.9 | 38.8 | 38.8 | 38.5 | 38.7 | 38.7 | (0.6) | 0.1 | 0.2 |

Source: Nomura estimates

Fig. 3: Largan - quarterly financial forecasts

| (TWDmn) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 | 1Q26 | 2Q26 | 3Q26F | 4Q26F | 2026F | 1Q27F | 2Q27F | 3Q27F | 4Q27F | 2027F | 2028F |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Net revenue | 14,579 | 11,673 | 17,677 | 17,219 | 61,148 | 15,544 | 13,665 | 17,184 | 19,544 | 65,936 | 15,524 | 14,532 | 20,252 | 21,959 | 72,266 | 80,815 |

| COGS | 6,615 | 5,413 | 9,325 | 8,958 | 30,311 | 7,865 | 6,913 | 8,603 | 9,366 | 32,746 | 7,766 | 7,157 | 9,648 | 10,288 | 34,859 | 38,775 |

| Gross profit | 7,965 | 6,260 | 8,352 | 8,260 | 30,837 | 7,680 | 6,752 | 8,580 | 10,178 | 33,190 | 7,757 | 7,375 | 10,603 | 11,671 | 37,407 | 42,040 |

| Op expenses | 1,878 | 1,381 | 2,088 | 1,932 | 7,279 | 1,867 | 1,604 | 2,070 | 2,242 | 7,783 | 1,917 | 1,790 | 2,280 | 2,407 | 8,393 | 8,932 |

| Op profit | 6,086 | 4,879 | 6,265 | 6,329 | 23,558 | 5,812 | 5,148 | 6,511 | 7,936 | 25,407 | 5,841 | 5,585 | 8,323 | 9,264 | 29,013 | 33,108 |

| Non-op profit | 1,630 | (3,085) | 1,890 | 1,907 | 2,342 | 1,476 | 951 | 1,420 | 1,420 | 5,267 | 1,420 | 1,420 | 1,420 | 1,420 | 5,680 | 5,680 |

| Pretax profit | 7,716 | 1,794 | 8,155 | 8,236 | 25,900 | 7,288 | 6,099 | 7,931 | 9,356 | 30,674 | 7,261 | 7,005 | 9,743 | 10,684 | 34,693 | 38,788 |

| Net profit | 6,443 | 1,032 | 7,080 | 6,720 | 21,275 | 6,123 | 4,670 | 6,503 | 7,672 | 24,968 | 5,954 | 5,365 | 7,990 | 8,761 | 28,070 | 31,381 |

| EPS (TWD) | 48.3 | 7.7 | 53.0 | 50.3 | 159.4 | 46.6 | 35.7 | 49.7 | 58.7 | 190.8 | 45.5 | 41.0 | 61.1 | 67.0 | 214.7 | 240.0 |

| Operating ratios (%) | ||||||||||||||||

| Gross margin | 54.6% | 53.6% | 47.2% | 48.0% | 50.4% | 49.4% | 49.4% | 49.9% | 52.1% | 50.3% | 50.0% | 50.7% | 52.4% | 53.2% | 51.8% | 52.0% |

| Operating margin | 41.7% | 41.8% | 35.4% | 36.8% | 38.5% | 37.4% | 37.7% | 37.9% | 40.6% | 38.5% | 37.6% | 38.4% | 41.1% | 42.2% | 40.1% | 41.0% |

| Pretax profit margin | 52.9% | 15.4% | 46.1% | 47.8% | 42.4% | 46.9% | 44.6% | 46.2% | 47.9% | 46.5% | 46.8% | 48.2% | 48.1% | 48.7% | 48.0% | 48.0% |

| Net profit margin | 44.2% | 8.8% | 40.1% | 39.0% | 34.8% | 39.4% | 34.2% | 37.8% | 39.3% | 37.9% | 38.4% | 36.9% | 39.5% | 39.9% | 38.8% | 38.8% |

| Year-to-year (%) | ||||||||||||||||

| Net revenue | 29% | 6% | -7% | -5% | 3% | 7% | 17% | -3% | 14% | 8% | 0% | 6% | 18% | 12% | 10% | 12% |

| Gross profit | 43% | 18% | -12% | -24% | -1% | -4% | 8% | 3% | 23% | 8% | 1% | 9% | 24% | 15% | 13% | 12% |

| Operating profit | 54% | 25% | -20% | -24% | -2% | -5% | 6% | 4% | 25% | 8% | 0% | 8% | 28% | 17% | 14% | 14% |

| Pretax profit | 4% | -69% | 4% | -26% | -20% | -6% | 240% | -3% | 14% | 18% | 0% | 15% | 23% | 14% | 13% | 12% |

| Net profit | 5% | -77% | 7% | -23% | -18% | -5% | 352% | -8% | 14% | 17% | -3% | 15% | 23% | 14% | 12% | 12% |

| Qtr-to-Qtr (%) | ||||||||||||||||

| Net revenue | -20% | -20% | 51% | -3% | -10% | -12% | 26% | 14% | -21% | -6% | 39% | 8% | ||||

| Gross profit | -26% | -21% | 33% | -1% | -7% | -12% | 27% | 19% | -24% | -5% | 44% | 10% | ||||

| Operating profit | -27% | -20% | 28% | 1% | -8% | -11% | 26% | 22% | -26% | -4% | 49% | 11% | ||||

| Pretax profit | -30% | -77% | 355% | 1% | -12% | -16% | 30% | 18% | -22% | -4% | 39% | 10% | ||||

| Net profit | -26% | -84% | 586% | -5% | -9% | -24% | 39% | 18% | -22% | -10% | 49% | 10% |

Source: Company data, Nomura estimates

H

o

b

p

L

f

M

w

/

9

B

W

P

I

x

K

t

q

3

k

n

5

F

y

d

R

e

A

8

z

l

O

+

D

c

u

C

N

a

(TWD)

6,000

5,000

4,000

3,000

2,000

1,000

0

Jan-15

Fig. 4: Largan - P/E band

Jan-16

(TWD)

6,000

5,000

4,000

Shiven

Source: TE. | Nomura estimates

6x

Fig. 5: Largan - P/B band

3x

Source: TEJ, Nomura estimates

Source: TEJ, Nomura estimates

25x

20x

15x

4.5x

Rating and target price chart (three year history)

5000.00

4500.00

4000.00

3000.00 •

2500.00

2000.00

1500.00

1000.00

500.00•

0.00

Largan Precision

Appendix A-1

Di

08

08

09

10

11

1

This report has been produced by Nomura International (Hong Kong) Ltd., Taipei Branch (NITB), Taiwan. See Disclaimers for Nomura Group entity details.