PDF 原檔:260630_3008_大立光_gs_largan_original.pdf

圖片清單(已驗證 2026-07-01)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

_004.png |

49KB | 真資料圖 | 月營收/出貨 YoY 成長率走勢圖(2013–2026) |

_005.png |

41KB | 真資料圖 | forward P/E band(avg 17.0x/+1SD 22.1x/-1SD 11.8x) |

_007.png |

81KB | 真資料圖 | GS 評等/目標價 3 年沿革圖 |

皆估值/走勢圖,lib 不嵌。<40KB 未列(_001/_002/_003/_006,鏡頭營收占比小圖等)預設不嵌。

OCR 限制

本 PDF 之財務模型附表經 pdf_parse/trim 後嚴重錯位(單字元散列,無法逐格判讀)。可讀內容為首頁 GS Forecast 摘要 + 投資論點段落;模型細格請以 GS 摘要數字為準,勿引用下方錯位表格數字。

原始內容

Goldman

56%

Research

48%

46%

2025

Periscope lens

• Others

Largan (3008.TW) 44%

Handset lens speci fi cation upgrade; CPO lens in expansion; TP up to NT$6,231, Buy

3008.TW

12m Pri c e Target:

NT$6,231.00

Pri c e:

NT$4,290.00

Upside:

45.2%

We are positive on Largan's expansion to CPO lens, and see its focus on high-end handset lens as supporting it with the growing vision AI trend in smartphones, and meaning it should be less impacted by the high memory costs. The expansion toward CPO lens o ff ers Largan diversi fi cation away from the competitive smartphone market, which we believe should support a re-rating for the company. We raise our target price to NT$6,231 (29.5x 2027E PE) from NT$3,423, with net income rising by 6% / 11% / 11% in 2026-28E. Maintain Buy.

Source: Company data, Goldman Sachs Global Investment Research

AI to drive handset lens upgrade: Camera is an important portal to input data for AI smartphones; the better quality of data input can enhance the AI processing and output, and strong hardware speci fi cation can physically capture more details, avoiding software over-editing, leading to more natural / more authentic photos / videos. In addition, AI can automatically optimise the aperture under di ff erent scenarios (e.g. from outdoors to indoors), reducing noise, or compensate for details of photos / video, enhancing user experience. In upcoming 2H26 fl agship models, we see continuous camera lens upgrade, supporting Largan's growth:

BUY

Verena Jeng +852-2978-1681 | verena.jeng@gs.com

Goldman Sachs (Asia) L.L.C.

Allen Chang +852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Ting Song +852-2978-6466 | ting.song@gs.com

Goldman Sachs (Asia) L.L.C.

Key Data _____________________________________

Market cap: NT$577.1bn / $18.1bn

Enterprise value: NT$449.9bn / $14.1bn

3m ADTV: NT$8.6bn / $271.3mn

Taiwan

Greater China Technology

M&A Rank: 3

Leases incl. in net debt & EV?: No

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue(NT$mn) New | 61,147.9 | 65,588.5 | 75,755.3 | 84,529.2 |

| Revenue (NT$ mn) Old | 6 1 , 1 47.9 | 63,330.6 | 70,297.8 | 75,296. 1 |

| EBITD A (NT$ mn) | 3 1 ,290.3 | 34,547.5 | 40,8 1 7. 1 | 45,898.9 |

| EPS(NT$) New | 159.41 | 188.11 | 213.81 | 237.08 |

| EPS (NT$) Old | 1 59.4 1 | 1 77.46 | 1 92.82 | 2 1 2.69 |

| P/E (X) | 1 4.8 | 22.8 | 20. 1 | 1 8. 1 |

| P/B (X) | 1 .7 | 2.9 | 2.7 | 2.5 |

| Dividend yield (%) | 3.3 | 2. 1 | 2.4 | 2.7 |

| CROCI (%) | 1 2.5 | 1 6. 1 | 1 5.9 | 1 5.7 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | 46.63 | 38.50 | 50.23 | 52.75 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

e92c7a75ab8b4efbba794e6b187208c8

BUY

Largan (3008.TW)

Rating since Nov 12, 2024

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | 14.8 | 22.8 | 20.1 | 18.1 |

| P/B (X) | 1. 7 | 2.9 | 2. 7 | 2.5 |

| FCF yield (%) | 4.3 | 4.1 | 4.4 | 5.4 |

| EV/EBITDAR (X) | 6.4 | 12.8 | 10.6 | 9.1 |

| EV/EBITDA (excl. leases) (X) | 6.4 | 12.8 | 10.6 | 9.1 |

| CROCI (%) | 12.5 | 16.1 | 15.9 | 15. 7 |

| ROE (%) | 11.4 | 12.8 | 13. 7 | 14.1 |

| Net debt/equity (%) | (64.1) | (66.6) | (6 7 .9) | ( 7 0.6) |

| Net debt/equity (excl. leases) (%) | (64.1) | (66.6) | (6 7 .9) | ( 7 0.6) |

| Interest cover (X) | 15,611.8 | 43, 7 40.4 | -- | -- |

| Days inventory outst, sales | 3 7 .1 | 38.9 | 36.9 | 35.5 |

| Receivable days | 62.1 | 60.0 | 59.0 | 58.0 |

| Days p ayable outstandin g | 21.6 | 22.0 | 24.0 | 24.0 |

| DuPont ROE (%) | 11.1 | 12.3 | 13.1 | 13.6 |

| Turnover (X) | 0.3 | 0.3 | 0.3 | 0.3 |

| L evera g e (X) | 1.2 | 1.2 | 1.2 | 1.2 |

| G ross cas h invested (ex cas h ) (NT $ ) | 1 7 6,8 7 9.0 | 19 7 ,81 7 .9 | 220,514.4 | 244,820.1 |

| Avera g e ca p ital e mp loyed (NT $ ) | 7 3,429.5 | 7 4,596.1 | 7 5,156.4 | 7 5,469.6 |

| BVP S (NT $ ) | 1,395.59 | 1,49 7 . 7 2 | 1,59 7 .98 | 1, 7 22.56 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | 2 . 8 | 7 . 3 | 15 . 5 | 11 . 6 |

| EBITDA growth | 3 .4 | 10 .4 | 18 . 1 | 12 . 5 |

| EPS growth | (19 . 7) | 18 . 0 | 13 . 7 | 10 . 9 |

| DPS growth | (19 . 0) | 18 . 2 | 13 . 6 | 11 . 3 |

| EBIT margin | 38 . 5 | 39 . 6 | 4 2 . 6 | 44. 1 |

| EBITDA margin | 51 . 2 | 52 . 7 | 53 . 9 | 5 4. 3 |

| Net income margin | 3 4. 8 | 38 . 1 | 37 . 7 | 37 .4 |

3m

99.1%

36.9%

1

2m

80.3%

6m

71.9%

8.0%

(13.0)%

Source: FactSet. Price as of 30 Jun 2026 close.

Absolute

Rel. to the Taiwan SE Weighted Index

Income Statement (NT$ mn) ________________________________

12/25

6

1,147.9

(30,310.8)

(1,985.5)

(5,293.3)

--

3

2

90.3

1

,

(7,732.0)

2

3,

.3

558

4,258.6

87.0

25

,900.

2

(4,340.0)

(284.9)

--

21

,

21

275

.4

--

275

.4

,

15

9.4

157

1

.

21

15

1

9.4

157

21

.

77.87

48.9

12/26E

65,588.5

(31,873.0)

(2,008.0)

(5,725.6)

--

34,

.

4

5

7

5

(8,565.7)

25

.

81

8

,9

3,883.5

28.4

30,3

0.

7

6

(5,118.7)

(246.2)

--

25

,00

25

,00

.

7

5

--

5

188

7

.

.

11

185

88

.

188

.

11

185

.

88

92.07

48.9

12/27E

75,755.3

(34,465.3)

(2,356.0)

(6,666.5)

--

40,

1

817

.

(8,549.5)

3

6

,

2

267

.

4,643.1

--

3

,9

1

6

7

0.

(8,120.4)

(254.1)

--

28

,

5

3

28

,

5

3

6

.3

--

6

21

.3

3.

81

211

.

22

21

3.

81

211

.

22

104.63

48.9

12/28E

84,529.2

(37,071.2)

(2,628.9)

(7,523.1)

--

4

5

,

.9

9

8

8

(8,592.9)

3

7

,30

6

.0

4,664.3

--

4

,9

7

1

0.3

(10,072.9)

(255.5)

--

1

3

,

3

6

4

1

,

6

4

2

1

.9

--

1

3

.9

7

2

.0

3

8

5

2

8

.0

3

8

7

.0

2

3

8

5

.0

116.45

49.1

Tota

v

r

e

nu

e

l

e

Co

s

t of good

SG&A

R&D

Other operating inc./(exp.)

E

BITDA

Depreciation & amortization

E

BIT

Net intere

s

t inc./(exp.)

Income/(lo ss

) from a ss

Pre-tax pro fi

t

Provi

s

ion for taxe

s

Minority intere

s

t

Preferred dividend

s

N

et inc

.

(

pre-ex

c

Po ept

s

t-tax exceptional

N

ociate

s

n

o

i

s

et

E

P

E

E

ept inc

.

(

po

s

t-ex

c

S

P

P

(b

a

S

S

sic

(dilu

i

o

c

a

ls)

n

ept

, pre-ex te

(b

a

, pre-ex

d

sic

, po

E

(dilu

P

S

te

a

ls)

)

(N

c

ept

s

t-ex

c

d

, po

$)

T

)

(N

ept

s

)

t-ex

DPS (NT$)

Div. payout ratio (%)

Balance Sheet (NT$ mn) ____________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| C a sh& c a sh equiv a lents | 115,941.7 | 128,975.2 | 141,341.2 | 158,208.8 |

| Accounts receiv a ble | 10,461.7 | 11,101.6 | 13,389.2 | 13,474.9 |

| Inventory | 6,713.2 | 7,258.5 | 8,038.4 | 8,415.2 |

| Other current a ssets | 21,168.8 | 21,168.8 | 21,168.8 | 21,168.8 |

| Total current assets | 15 4 ,285 . 5 | 168,5 04. 1 | 18 3 , 93 7 . 6 | 2 0 1,267 . 7 |

| Net PP&E | 51,472.4 | 51,984.2 | 52,757.3 | 52,848.2 |

| Net int a ngibles | 474.6 | 351.6 | 344.5 | 213.7 |

| Tot a l investments | 26.5 | 26.5 | 26.5 | 26.5 |

| Other long-term a ssets | 14,528.1 | 14,528.1 | 14,528.1 | 14,528.1 |

| Total assets | 22 0 ,787 .0 | 2 3 5, 394.4 | 251,5 94.0 | 268,88 4. 2 |

| Accounts p a y a ble | 1,727.9 | 2,114.3 | 2,418.1 | 2,457.0 |

| Short-term debt | 0.0 | 0.0 | 0.0 | 0.0 |

| Short-term le a se li a bilities | -- | -- | -- | -- |

| Other current li a bilities | 28,020.6 | 29,868.4 | 31,617.2 | 33,155.6 |

| Total current liabilities | 2 9 ,7 4 8 . 5 | 3 1, 9 82 . 7 | 34 , 03 5 .3 | 3 5,612 . 6 |

| Long-term debt | -- | -- | -- | -- |

| Long-term le a se li a bilities | -- | -- | -- | -- |

| Other long-term li a bilities | 170.6 | 170.6 | 170.6 | 170.6 |

| Total long-term liabilities | 17 0. 6 | 17 0. 6 | 17 0. 6 | 17 0. 6 |

| Total liabilities | 2 9 , 9 1 9. 1 | 3 2,15 3.3 | 34 ,2 0 5 .9 | 3 5,78 3. 2 |

| Preferred sh a res | -- | -- | -- | -- |

| Tot a l commonequity | 188,867.2 | 201,486.5 | 215,887.6 | 231,855.9 |

| Minority interest | 2, 000. 8 | 1,75 4. 6 | 1,5 00. 6 | 1,2 4 5 . 1 |

| Total liabilities &equity | 22 0 ,787 .0 | 2 3 5, 394.4 | 251,5 94.0 | 268,88 4. 2 |

| Net debt, a djusted | (122,308.6) | (135,342.0) | (147,708.1) | (164,575.7) |

Cash Flow (NT$ mn) ________________________________________

12/25

25,900.2

7,732.0

(284.9)

(1,208.2)

(6,058.9)

26

2

,0

8

0.

(12,340.0)

(2,040.4)

(2.6)

5,147.2

(9,

)

.

3

2

5

7

--

(13,013.1)

(203.4)

(1,344.6)

1

)

2

561

.

4,

2

,

28

3.4

13,740.3

8

(

12/26E

25,005.7

8,565.7

(246.2)

(798.8)

--

3

.

5

526

2

,

(8,854.4)

--

(100.0)

--

,9

5

4.4)

--

(10,538.6)

--

0.0

5

6

1

.

8

)

3

0,

1

3,033.

5

12

12/27E

28,536.3

8,549.5

(254.1)

(2,763.6)

--

34,0

.

68

1

(9,090.6)

--

(225.0)

--

(9,3

15

.

6

)

--

(12,386.4)

--

0.0

,3

86

.4)

12

,3

66

.0

1

4,

1

(

8

12/28E

31,641.9

8,592.9

(255.5)

(423.6)

--

39,

.

555

8

(8,452.9)

--

(100.0)

--

,

552

.9)

--

(14,135.2)

--

0.0

3

5

.

2

)

16

,

867

.

6

23,672.1

24,977.4

31,102.8

Source: Company data, Goldman Sachs Research estimates.

T

(N

c

$)

T

ept

$)

)

(N

T

$)

s

Net income

D&A add-back

Minority interest add-back

Net (inc)/dec

w

orking capital

Other operating cash flo

w

Cash flow fro operations

m

Capital expenditures

Acquisitions

Divestitures

Others

Cash flow fro

m

investing

Repayment of lease liabilities

Dividends paid (common & pref)

Inc/(dec) in debt

Other financing cash flo

w

s

Cash flow fro

m

Total cash flow

w

Free cash flo financing

s

old

(

(

(

(

e92c7a75ab8b4efbba794e6b187208c8

- Variable Aperture: lens aperture changes based on the focal length (e.g. Huawei n Pura 90 Pro Max launched in Apr 2026 featured with f/1.4-f/4.0 variable aperture wide camera), allowing easier user control of DoF (depth of fi eld), taking pictures in low lights, or having a more natural broken gradient background when in portrait mode.

- Under-Display Camera (UDC) brings true full-screen visual experience, maximizing n screen-to-body ratio and better environmental sealing (e.g. easier to achieve high water and dust resistance ratings). Huawei Mate 90 Pro in 4Q26 is likely to upgrade to UDC (link). The previous model launched in Nov 2025 priced at Rmb5,999 (US$884) with single front camera at 13MPx.

- Dual 200MPx with front camera upgrades: OPPO Find X10 Pro series likely to n launch in Sep or Oct with dual 200MPx and front camera upgrade to 100MPx (link). The previous model OPPO Find X9 Pro priced at Rmb5,299 (US$780) and launched in Oct 2025 with triple rear cameras (50MPx wide, 200MPx periscope tele, 50MPx ultrawide) and single front camera (50MPx). Honor Magic 9 Pro Max likely to launch in Oct with dual 200MPx (link). The previous model Honor Magic 8 Pro is launched in Oct 2025 and priced at Rmb5,699 (US$839) with triple rear cameras (50MPx wide, 200MPx periscope tele, 50MPx ultrawide) and single front camera (50MPx). Xiaomi 18 all series likely to launch in Sep with dual 200MPx (link). The previous model Xiaomi 17 was launched in Sep 2025 priced at Rmb4,499 (US$662) with triple rear cameras (50MPx wide, 200MPx periscope tele, 50MPx ultrawide) and single front camera (50MPx).

- 10x optical zoom: Vivo launched X300 Ultra in Mar 2026 priced at Rmb6,999 n (US$1,030) with triple rear cameras (200MPx wide, 200MPx periscope tele, 50MPx ultrawide) and single front camera (50MPx). The upcoming Vivo X500 Ultra in 4Q26 is likely to upgrade the rear periscope tele from 3.7x optical zoom to 10x optical zoom (link). Huawei Mate 90 Pro Max in 4Q26 is likely to upgrade the rear periscope tele from 4x / 6.2x optical zoom to 10x optical zoom (link). The previous model launched in Nov 2025 priced at Rmb7,999 (US$1,178) with quad rear cameras (50MPx wide, 50MPx periscope tele, 50MPx periscope tele, 40MPx ultrawide) and single front camera (13MPx).

Premium models su ff er less under the high memory costs: Global smartphone shipment declined by 4% YoY in 1Q26, while premium brands outperform: Samsung / Apple increased by 3.6% / 3.3% YoY (link), echoing our view that global leading brand makers enjoy better bargaining power over the supply chain, given larger procurement scale, and over customers, given strong brand awareness and as consumers of premium models are less price sensitive. As we highlighted in June in our Global Smartphone TAM report, we expect global smartphone shipment to decline 10% YoY in 2026E and stay low at 2027E (+3% YoY), while we continue to expect iPhones to outperform (-2% / +5% YoY in 2026 / 27E) with growing foldable iPhones (14m / 34m in 2026 / 27E). Largan mainly serves global leading smartphone brands with strong exposure to high-end handset lens, and we expect the premium model outperformance under the current challenging environment to continue to support Largan's growth ahead.

CPO lens, entering fast growth AI servers market: We are positive on Largan's expansion to lens for FAU in CPO switches for AI infrastructure, leading Largan to e92c7a75ab8b4efbba794e6b187208c8

Earnings revision

participate in the fast-growing AI server industry. As we highlighted in our Optical Networking thematic report, we expect CPO switch to start in 2H26, expanding from scale out to scale up with bandwidth migration (from 1.6T to 3.2T / 6.4T), supporting Largan's growth in coming years. Despite expecting a small revenue contribution in the near term, we believe it will enhance Largan's long term growth visibility, and rea ffi rms Largan's leading market position in the lens industry, which deserves a re-rating in our view. Note that the Taiwan AI server supply chain enjoyed a strong re-rating when it entered the AI server supply chain.

Exhibit 2: Taiwan AI server supply chain enjoyed a re-rating when AI servers ramped up

| Company | Ticker | 2020-2025 PE | 2020-2025 PE | 2020-2025 PE |

|---|---|---|---|---|

| Trough | Peak | Diff | ||

| Largan | 3008.TW | 10.6 | 28.0 | 163% |

| Taiwan AI server supply chain | Taiwan AI server supply chain | Taiwan AI server supply chain | Taiwan AI server supply chain | Taiwan AI server supply chain |

| Hon Hai | 2317.TW | 7.7 | 17.5 | 129% |

| Wistron | 3231.TW | 6.0 | 21.8 | 262% |

| King Slide | 2059.TW | 9.0 | 30.2 | 236% |

| AVC | 3017.TW | 4.7 | 32.8 | 604% |

| Landmark | 3081.TWO | 28.9 | 144.1 | 398% |

| Auras | 3324.TWO | 8.8 | 54.6 | 523% |

| Chenbro | 8210.TW | 6.7 | 25.6 | 282% |

| Fositek | 6805.TW | 11.3 | 49.9 | 343% |

| Mitac | 3706.TW | 2.5 | 28.7 | 1044% |

| VPEC | 2455.TW | 18.1 | 74.1 | 310% |

| Inventec | 2356.TW | 9.9 | 31.0 | 213% |

| Avg. | 10.3 | 46.4 | 395% |

Source: Company data

We raise net income by 6% / 11% / 11% in 2026-28E mainly on higher revenues, re fl ecting premium smartphone models outperforming the market, with the high memory costs supporting Largan's handset lens shipment growth and pixel mix upgrade, and Largan's expansion toward CPO lens.

Exhibit 3: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NTm | Old | New | Chg | Old | New | Chg | Old | New | Chg |

| Revenue | 63,331 | 65,588 | 4% | 70,298 | 75,755 | 8% | 75,296 | 84,529 | 12% |

| GP | 32,486 | 33,715 | 4% | 38,022 | 41,290 | 9% | 41,795 | 47,458 | 14% |

| OP | 24,937 | 25,982 | 4% | 29,966 | 32,268 | 8% | 33,392 | 37,306 | 12% |

| Net income | 23,685 | 25,006 | 6% | 25,734 | 28,536 | 11% | 28,386 | 31,642 | 11% |

| EPS (Diluted) | 175.99 | 185.88 | 6% | 191.21 | 211.22 | 10% | 210.92 | 235.08 | 11% |

| Margins | |||||||||

| GM | 51.3% | 51.4% | 54.1% | 54.5% | 55.5% | 56.1% | |||

| OPM | 39.4% | 39.6% | 42.6% | 42.6% | 44.3% | 44.1% | |||

| NM | 37.4% | 38.1% | 36.6% | 37.7% | 37.7% | 37.4% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

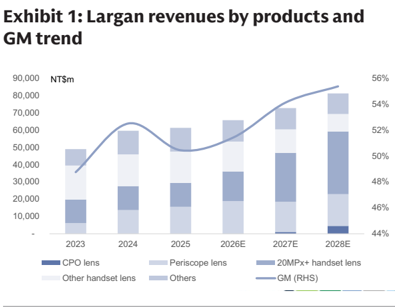

Exhibit 4: Revenues and GM revision by products

| AAC 80kk | O-Film 31.6kk | Remark | Chart | 2027E | 2028E | ||

|---|---|---|---|---|---|---|---|

| NEW | 65,588 | 75,755 | 84,529 | NEW | 51.4% | 54.5% | 56.1% |

| CPO lens | 63 | 1,067 | 4,518 | CPO lens | 50.3% | 50.4% | 50.5% |

| Periscope lens | 18,762 | 18,570 | 19,783 | Periscope lens | 38.9% | 38.5% | 38.5% |

| 20MPx+ handset lens | 17,130 | 30,178 | 38,447 | 20MPx+ handset lens | 72.8% | 73.0% | 74.0% |

| Other handset lens | 17,282 | 13,632 | 9,898 | Other handset lens | 62.6% | 62.4% | 62.1% |

| Others | 12,351 | 12,309 | 11,884 | Others | 24.9% | 24.9% | 25.0% |

| OLD | 63,331 | 70,298 | 75,296 | OLD | 51.3% | 54.1% | 55.5% |

| CPO lens | - | - | - | CPO | |||

| Periscope | lens | ||||||

| lens | 17,583 | 17,042 | 18,087 | Periscope lens | 38.7% | 38.5% | 38.5% |

| 20MPx+ handset lens | 16,326 | 27,672 | 35,433 | 20MPx+ handset lens | 72.7% | 72.6% | 72.6% |

| Other handset lens | 17,107 | 13,331 | 9,869 | Other handset lens | 62.6% | 62.3% | 62.1% |

| Others | 12,314 | 12,252 | 11,907 | Others | 25.1% | 25.0% | 25.0% |

| CHG | 4% | 8% | 12% | CHG (NEW - OLD) | 0.1% | 0.4% | 0.6% |

| CPO lens | na | na | na | CPO lens | |||

| Periscope lens | 7% | 9% | 9% | Periscope lens | 0.2% | 0.0% | 0.0% |

| 20MPx+ handset lens | 5% | 9% | 9% | 20MPx+ handset lens | 0.1% | 0.4% | 1.4% |

| Other handset lens | 1% | 2% | 0% | Other handset lens | 0.0% | 0.0% | 0.0% |

| Others | 0% | 0% | 0% | Others | -0.1% | 0.0% | 0.0% |

Source: Goldman Sachs Global Investment Research

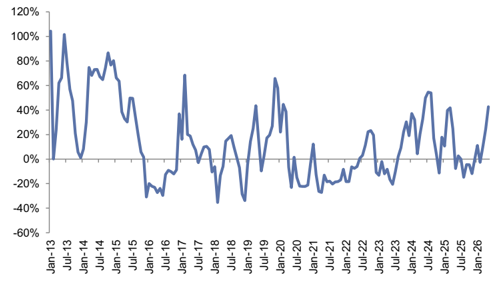

Largan's April and May revenues were 12% / 42% ahead of our estimates, re fl ecting the stronger-than-expected handset lens growth. We expect a sequential decline in June considering its major smartphone brand customer is under model transition, and a sequential increase in July as demand for lens for new models ramps up.

Exhibit 5: Largan revenues YoY

Source: Company data

Exhibit 6: Largan monthly revenues preview

| Apr 2026 | May 2026 | Jun 2026E | Jul 2026E | Aug 2026E | Sep 2026E | 1Q26 | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 5,362 | 4,593 | 3,795 | 5,692 | 6,262 | 6,912 | 15,544 | 13,750 | 18,866 |

| YoY | 24% | 43% | -8% | 5% | 5% | 11% | 7% | 18% | 7% |

| MoM/QoQ | -1% | -14% | -17% | 50% | 10% | 10% | -10% | -12% | 37% |

| GS estimates (NT$m) | 4,769 | 3,243 | 14,180 | ||||||

| Act. Vs. GS | 12% | 42% | 10% |

Source: Company data, Goldman Sachs Global Investment Research

Compared to Bloomberg consensus, we are largely in line in 2026E, and 15% ahead in 2027E operating income, given our higher revenue and GM estimates, re fl ecting our positive view on Largan's focus on high-end handset lens, premium models being likely to su ff er less under the high memory cost environment, and Largan's expansion towards CPO lens.

e92c7a75ab8b4efbba794e6b187208c8

Valuation

Exhibit 7: GS vs. Bloomberg consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | |

|---|---|---|---|---|---|---|

| NT m | GS | BB | Diff% | GS | BB | Diff% |

| Revenue | 65,588 | 66,124 | -1% | 75,755 | 70,488 | 7% |

| GP | 33,715 | 33,342 | 1% | 41,290 | 36,407 | 13% |

| OP | 25,982 | 25,656 | 1% | 32,268 | 28,156 | 15% |

| Net income | 25,006 | 24,742 | 1% | 28,536 | 26,522 | 8% |

| Margins | ||||||

| GM | 51.4% | 50.4% | 54.5% | 51.7% | ||

| OPM | 39.6% | 38.8% | 42.6% | 39.9% | ||

| NM | 38.1% | 37.4% | 37.7% | 37.6% |

Source: Goldman Sachs Global Investment Research, Bloomberg

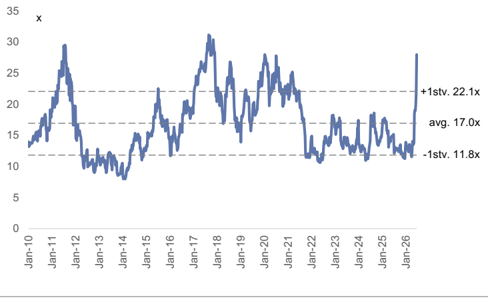

We continue to derive our target price from 2027E PE, and update our target PE multiple from 17.9x to 29.5x. Our target PE multiple (29.5x) is derived from (1) peers' avg. ratio of trading PE to forward year fundamentals (NI YoY and OPM), which is at 0.5x, and (2) Largan's forward year fundamentals: 2027-28E NI YoY at 13% on avg. and OPM at 43% on avg. Our previous target PE multiple (17.9x) was derived from Largan's historical trading avg. during periods when its OPM is recovering, which is di ffi cult to re fl ect Largan's expansion to fast-growing AI server supply chain, in our view. The ratio of our new target PE multiple to forward year fundamentals (NI YoY and OPM) is at 0.5x, higher than our previous ratio (0.4x) of a target PE multiple to forward year fundamentals (NI YoY and OPM), re fl ecting our positive view on Largan's expansion from handset lens to CPO lens. The new target PE multiple of 29.5x is within Largan's historical trading range of 8.0x to 31.2x, re fl ecting our positive view on Largan's expansion from handset lens to CPO lens. Our new target price is at NT$6,231 (vs. NT$3,423 previously). Maintain Buy.

Exhibit 8: Largan peer comparison

| Company | Ticker | Rating | PE | NI YoY | NI YoY | OPM | OPM | Ratio |

|---|---|---|---|---|---|---|---|---|

| 2027E | 2027E | 2028E | 2027E | 2028E | ||||

| Largan | 3008.TW | Buy | 20.3 | 14% | 11% | 42.6% | 44.1% | 0.4 |

| Largan (TP implied) | 3008.TW | Buy | 29.5 | 14% | 11% | 42.6% | 44.1% | 0.5 |

| Peers | ||||||||

| AAC | 2018.HK | Buy | 13.4 | 12% | 12% | 9.7% | 10.0% | 0.6 |

| Q-Tech | 1478.HK | NC | 7.1 | 21% | 16% | 4.3% | 4.3% | 0.3 |

| Himax | HIMX | NC | 16.7 | 83% | 101% | 13.2% | 20.7% | 0.2 |

| SEMCO | 009150.KS | Buy | 62.9 | 75% | 18% | 18.9% | 19.1% | 1.0 |

| Genius | 3406.TW | NC | 18.1 | 8% | 13% | 20.1% | 19.6% | 0.6 |

| Average | 23.6 | 40% | 32% | 13.2% | 14.7% | 0.5 |

NC=not covered

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 9: Largan 12M forward PE ratio

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg

Financial tables

Exhibit 11: Largan P&L

| NT$m | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenues | 14,579 | 11,673 | 17,677 | 17,219 | 15,544 | 13,750 | 18,866 | 17,428 | 48,842 | 59,458 | 61,148 | 65,588 | 75,755 | 84,529 |

| GP | 7,965 | 6,260 | 8,352 | 8,260 | 7,680 | 6,820 | 9,336 | 9,880 | 23,808 | 31,209 | 30,837 | 33,715 | 41,290 | 47,458 |

| OP income | 6,086 | 4,879 | 6,265 | 6,329 | 5,812 | 5,168 | 7,091 | 7,911 | 17,821 | 24,033 | 23,558 | 25,982 | 32,268 | 37,306 |

| Net income | 6,443 | 1,032 | 7,080 | 6,720 | 6,123 | 5,139 | 6,704 | 7,040 | 17,902 | 25,915 | 21,275 | 25,006 | 28,536 | 31,642 |

| EPS, diluted (NT$) | 47.73 | 7.70 | 52.61 | 49.17 | 46.11 | 38.04 | 49.62 | 52.11 | 132.62 | 191.44 | 157.21 | 185.88 | 211.22 | 235.08 |

| YoY | ||||||||||||||

| Revenues | 29% | 6% | -7% | -5% | 7% | 18% | 7% | 1% | 2% | 22% | 3% | 7% | 16% | 12% |

| GP | 43% | 18% | -13% | -23% | -4% | 9% | 12% | 20% | -9% | 31% | -1% | 9% | 22% | 15% |

| OP income | 54% | 25% | -20% | -24% | -5% | 6% | 13% | 25% | -13% | 35% | -2% | 10% | 24% | 16% |

| Net income | 5% | -77% | 7% | -23% | -5% | 398% | -5% | 5% | -21% | 45% | -18% | 18% | 14% | 11% |

| EPS, diluted (NT$) | 5% | -77% | 7% | -22% | -3% | 394% | -6% | 6% | -21% | 44% | -18% | 18% | 14% | 11% |

| QoQ | ||||||||||||||

| Revenues | -20% | -20% | 51% | -3% | -10% | -12% | 37% | -8% | ||||||

| GP | -26% | -21% | 33% | -1% | -7% | -11% | 37% | 6% | ||||||

| OP income | -27% | -20% | 28% | 1% | -8% | -11% | 37% | 12% | ||||||

| Net income | -26% | -84% | 586% | -5% | -9% | -16% | 30% | 5% | ||||||

| EPS, diluted (NT$) | -24% | -84% | 583% | -7% | -6% | -18% | 30% | 5% | ||||||

| Margins | ||||||||||||||

| GM | 54.6% | 53.6% | 47.2% | 48.0% | 49.4% | 49.6% | 49.5% | 56.7% | 48.7% | 52.5% | 50.4% | 51.4% | 54.5% | 56.1% |

| OPM | 41.7% | 41.8% | 35.4% | 36.8% | 37.4% | 37.6% | 37.6% | 45.4% | 36.5% | 40.4% | 38.5% | 39.6% | 42.6% | 44.1% |

| NM | 44.2% | 8.8% | 40.1% | 39.0% | 39.4% | 37.4% | 35.5% | 40.4% | 36.7% | 43.6% | 34.8% | 38.1% | 37.7% | 37.4% |

| Ratios | ||||||||||||||

| Opex ratio | 13% | 12% | 12% | 11% | 12% | 12% | 12% | 11% | 12% | 12% | 12% | 12% | 12% | 12% |

| Tax rate | 15% | 42% | 12% | 17% | 15% | 15% | 16% | 20% | 19% | 19% | 17% | 17% | 22% | 24% |

Source: Company data, Goldman Sachs Global Investment Research

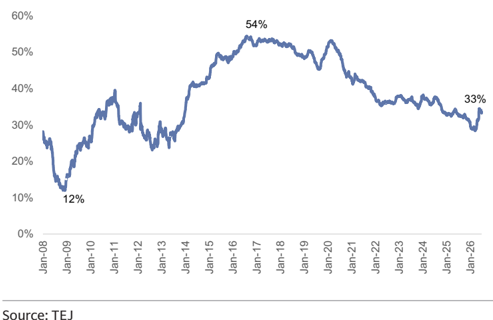

Exhibit 10: Largan QFII holdings

Source: TEJ

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 12: Largan balance sheet

| NT$ mn | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|

| Balance Sheet | ||||||

| Cash and equivalents | 107,490 | 113,658 | 115,942 | 128,975 | 141,341 | 158,209 |

| Accounts receivable | 10,091 | 10,360 | 10,462 | 11,102 | 13,389 | 13,475 |

| Inventory | 4,591 | 5,733 | 6,713 | 7,259 | 8,038 | 8,415 |

| Other current assets | 12,149 | 16,012 | 21,169 | 21,169 | 21,169 | 21,169 |

| Current assets | 134,321 | 145,764 | 154,285 | 168,504 | 183,938 | 201,268 |

| Net PP&E/Fixed assets | 41,135 | 46,936 | 51,472 | 51,984 | 52,757 | 52,848 |

| Net intangibles | 239 | 505 | 475 | 352 | 345 | 214 |

| Other long-term assets | 19,443 | 23,322 | 14,555 | 14,555 | 14,555 | 14,555 |

| Non-current assets | 60,817 | 70,763 | 66,502 | 66,890 | 67,656 | 67,616 |

| Total assets | 195,138 | 216,527 | 220,787 | 235,394 | 251,594 | 268,884 |

| Accounts payable | 1,731 | 1,855 | 1,728 | 2,114 | 2,418 | 2,457 |

| Short-term debt | - | 203 | - | - | - | - |

| Other current liabilities | 27,787 | 28,520 | 28,021 | 29,868 | 31,617 | 33,156 |

| Current liabilities | 29,517 | 30,578 | 29,749 | 31,983 | 34,035 | 35,613 |

| Long-term debt | - | - | - | - | - | - |

| Other long-term liabilities | 110 | 561 | 171 | 171 | 171 | 171 |

| Non-current liabilities | 110 | 561 | 171 | 171 | 171 | 171 |

| Total liabilities | 29,627 | 31,139 | 29,919 | 32,153 | 34,206 | 35,783 |

| Common stock | 1,335 | 1,335 | 1,335 | 1,335 | 1,335 | 1,335 |

| Retained earnings | 160,871 | 175,969 | 185,818 | 198,437 | 212,838 | 228,807 |

| Other common equity | 3,305 | 6,215 | 1,714 | 1,714 | 1,714 | 1,714 |

| Total common equity | 165,510 | 183,519 | 188,867 | 201,487 | 215,888 | 231,856 |

| Minority interest | - | 1,869 | 2,001 | 1,755 | 1,501 | 1,245 |

| Total equity | 165,510 | 185,388 | 190,868 | 203,241 | 217,388 | 233,101 |

| BVPS | 1,226.07 | 1,369.51 | 1,410.38 | 1,510.76 | 1,609.09 | 1,731.81 |

| Cash conversion cycle | ||||||

| Account receivable days | 68 | 63 | 62 | 60 | 59 | 58 |

| Inventory days | 71 | 67 | 75 | 80 | 81 | 81 |

| Net payable days | 25 | 23 | 22 | 22 | 24 | 24 |

| Cash conversion cycle | 114 | 106 | 116 | 118 | 116 | 115 |

| Ratios | ||||||

| ROE (common equity) | 11% | 15% | 11% | 13% | 14% | 14% |

| ROA | 9% | 13% | 10% | 11% | 12% | 12% |

| Net debt to total equity | -67% | -64% | -64% | -67% | -68% | -71% |

| Net cash per share (NTD) | (827.12) | (870.08) | (903.77) | (1,006.04) | (1,093.32) | (1,222.70) |

| Total liabilities to total assets | 15% | 14% | 14% | 14% | 14% | 13% |

| Dupont analysis | ||||||

| Asset turnover | 0.3 | 0.3 | 0.3 | 0.3 | 0.3 | 0.3 |

| Leverage (assets to equity) | 1.2 | 1.2 | 1.2 | 1.2 | 1.2 | 1.2 |

| Net margin | 36.7% | 43.6% | 34.8% | 38.1% | 37.7% | 37.4% |

| ROE (total equity) | 11% | 15% | 11% | 13% | 14% | 14% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 13: Largan cash fl ow

| NT$ mn | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|

| Cash flow statement | ||||||

| Net income | 22,102 | 32,174 | 25,900 | 25,006 | 28,536 | 31,642 |

| Minority interest add-back | - | (296) | (285) | (246) | (254) | (255) |

| Depreciation and amortization add-back | 5,422 | 6,230 | 7,732 | 8,566 | 8,549 | 8,593 |

| (Increase)/decrease in working capital | (1,400) | (1,287) | (1,208) | (799) | (2,764) | (424) |

| Other operating cash flow items | (7,925) | (5,243) | (6,059) | - | - | - |

| Cash flow from operating | 18,199 | 31,579 | 26,080 | 32,527 | 34,068 | 39,556 |

| Capital expenditure | (8,237) | (11,133) | (12,340) | (8,854) | (9,091) | (8,453) |

| Other investment cash flow items | (2,915) | (4,933) | 3,104 | (100) | (225) | (100) |

| Cash flow from investing | (11,151) | (16,066) | (9,236) | (8,954) | (9,316) | (8,553) |

| Dividends paid | (11,412) | (9,009) | (13,013) | (10,539) | (12,386) | (14,135) |

| Change in common stock | - | - | - | - | - | - |

| Increase/(decrease) in short-term debt | (19) | 203 | (203) | - | - | - |

| Increase/(decrease) in long-term debt | - | - | - | - | - | - |

| Other financing cash flow items | 1,680 | (1,958) | (241) | - | - | - |

| Cash flow from financing | (9,750) | (10,764) | (13,458) | (10,539) | (12,386) | (14,135) |

| Net change in cash | (2,682) | 6,168 | 2,283 | 13,033 | 12,366 | 16,868 |

| FCF | 9,962 | 20,446 | 13,740 | 23,672 | 24,977 | 31,103 |

| Ratio | ||||||

| Capex to revenue | 17% | 19% | 20% | 14% | 12% | 10% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Price Target Risks and Methodology - Largan

Valuation : We are Buy rated on Largan and have a 12-month target price of NT$6,231, which is based on 2027E P/E. Our target P/E multiple of 29.5x is derived from (1) peers' avg. ratio of trading PE to forward year fundamentals (NI YoY and OPM), which is at 0.5x, and (2) Largan's forward year fundamentals: 2027-28E NI YoY at 13% on avg. and OPM at 43% on avg. The target PE multiple of 29.5x is within Largan's historical trading range of 8.0x to 31.2x, re fl ecting our positive view on Largan's expansion from handset lens to CPO lens.

Key risks : (1) slower-than-expected smartphone market growth, (2) fi ercer competition in handset lenses, (3) slower-than-expected smartphone camera lens speci fi cation upgrades or Largan's handset lens pixel mix upgrade, (4) slower-than-expected CPO lens ramp up, and (5) fi ercer competition in CPO lens.

e92c7a75ab8b4efbba794e6b187208c8