報告_大和_南駿6584_20260511

PDF 原檔:報告_大和_南駿6584_20260511_original.pdf

原始內容

Taiwan

Nan Juen International (6584 TT)

Target price:

TWD1,022.00 (from TWD1,000.00)

Share price (11 May):

TWD687.00

|

Up/downside:

+48.8%

1Q26 results review: demand outlook remains intact

- CSP rail kit slowdown driven by component shortages, not demand

- Nan Juen well-positioned to gain share in AI servers

- Reaffirming our Buy (1) rating with higher 12-month TP of TWD1,022

What’s new: We provide an update on Nan Juen after its 1Q26 results.

What’s the impact: 1Q26 results beat on FX gains. Nan Juen’s 1Q26 earnings came in at TWD235m (EPS: TWD3.38), which was 9% and 13% higher than our and the street’s expectations, respectively, due to higherthan-expected FX gains. While revenue was TWD867m (up 22% QoQ and 74% YoY), gross margin increased by 2.4pp QoQ to 41.6% due to the favourable product mix (server sales mix surpassed 70%). Accordingly, operating margin improved by 4.1pp to 29.5% given the operating leverage. Lastly, net profit was boosted by higher-than expected non-operating gains of TWD39m (mainly from FX gains).

Business outlook. Management is observing a slower-than-expected monthly shipment trend for its CSP regular server rail kit in April, a softness it anticipates will persist through 2Q26. However, as we understand it, this remains within the normal range of fluctuation, considering the shipment levels in 2025, and does not appear to signal any meaningful structural deterioration in demand. While we have made only modest downward adjustments to our model to reflect this near-term softness, we do not view this as a cause for significant concern at this stage. Despite the near-term weakness, we remain confident in the demand outlook for regular server rail kits, as the current slowdown appears to be primarily driven by component shortages (ie, CPUs, memory, and other key parts) rather than any fundamental weakening in end demand. As such, we believe that deferred demand is likely to be pushed out to 2H26 and into 2027, which should provide a meaningful tailwind for shipment recovery in the latter part of the forecast period. For AI servers, the status of GPU and ASIC server shipments has not changed materially from our previous update, and we continue to monitor the space closely for any developments. We maintain a positive view on its share gain story within AI servers by its strong product positioning and customer relationships. At the same time, we continue to see its regular server business as a key and stable demand, reinforcing our overall outlook on the company.

What we recommend: We lower our 2026E EPS by 4.9% but raise our 2027-28E EPS by 0.1-3.8% to factor in 1Q26 results. We therefore raise our 12M TP to TWD1,022, based on an unchanged PER of 36x (vs. its past-3-year range of 11-90x), applied to our 4-quarter forward EPS forecast. We reaffirm Buy (1) on Nan Juen. Key downside risk: worse-thanexpected AI server demand.

How we differ: Our 2027-28E EPS are 0.1-30% above the Bloomberg consensus, likely as we are more positive on Nan Juen’s revenue.

11 May 2026

Daiwa

5

3

→

2

1

Buy

Allan Wang

(886) 2 8758 6249

allan.wang@daiwacm-cathay.com.tw

Sheng Cheng

(886) 2 8758 6253 sheng.cheng@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | (4.0) | 4.4 | 0.8 |

| Net profit change | (4.9) | 3.8 | 0.1 |

| Core EPS (FD) change | (4.9) | 3.8 | 0.1 |

Source: Daiwa forecasts

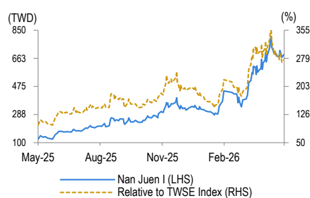

Share price performance

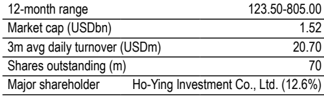

| 12-month range | 123.50-805.00 |

|---|---|

| Market cap (USDbn) | 1.52 |

| 3m avg daily turnover (USDm) | 20.70 |

| Shares outstanding (m) | 70 |

| Major shareholder Ho-Ying | lnvestment Co., Ltd. (12.6%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 4,327 | 7,417 | 8,190 |

| Operating profit (m) | 1,442 | 3,111 | 3,869 |

| Net profit (m) | 1,187 | 2,492 | 3,098 |

| Core EPS (fully-diluted) | 17.045 | 35.779 | 44.477 |

| EPS change (%) | 220.9 | 109.9 | 24.3 |

| Daiwa vs Cons. EPS (%) | (1.3) | 29.8 | 0.1 |

| PER (x) | 40.3 | 19.2 | 15.4 |

| Dividend yield (%) | 0.4 | 1.3 | 2.5 |

| DPS | 2.7 | 9.0 | 17.0 |

| PBR (x) | 11.5 | 8.0 | 6.0 |

| EV/EBITDA (x) | 27.6 | 13.4 | 10.4 |

| ROE (%) | 32.6 | 49.1 | 44.5 |

Source: FactSet, Daiwa forecasts

Nan Juen International (6584 TT): 11 May 2026

Nan Juen: Daiwa revenue and earnings forecasts revisions vs. the consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | Previous | New | Consensus | Previous | New | Consensus | Previous | New | Consensus |

| Revenue | 4,506 | 4,327 | 4,247 | 7,105 | 7,417 | 5,718 | 8,128 | 8,190 | 8,128 |

| Diff (%) | -4.0% | 1.9% | 4.4% | 29.7% | 0.8% | 0.8% | |||

| Gross Margin (%) | 46.6% | 45.4% | 44.6% | 54.0% | 53.8% | 53.4% | 59.2% | 58.9% | 59.2% |

| Operating profit | 1,556 | 1,442 | 1,487 | 2,995 | 3,111 | 2,391 | 3,864 | 3,869 | 3,864 |

| Op Margin (%) | 34.5% | 33.3% | 35.0% | 42.2% | 41.9% | 41.8% | 47.5% | 47.2% | 47.5% |

| Net profit | 1,248 | 1,187 | 1,203 | 2,400 | 2,492 | 1,920 | 3,094 | 3,098 | 3,094 |

| EPS (TWD) | 17.91 | 17.04 | 17.26 | 34.45 | 35.78 | 27.56 | 44.42 | 44.48 | 44.41 |

| Diff (%) | -4.9% | -1.3% | 3.8% | 29.8% | 0.1% | 0.1% |

Source: Bloomberg, Daiwa forecasts

Nan Juen: quarterly and annual P&L statement

| 2026E | 2026E | 2026E | 2026E | 2027E | 2025 | 2026E | 2027E | 2028E | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | ||||

| Net revenue | 867 | 918 | 1,163 | 1,379 | 1,711 | 1,943 | 1,906 | 1,858 | 2,433 | 4,327 | 7,417 | 8,190 |

| COGS | -507 | -519 | -629 | -708 | -813 | -873 | -876 | -863 | -1,582 | -2,362 | -3,426 | -3,363 |

| Gross profit | 360 | 399 | 534 | 672 | 898 | 1,070 | 1,029 | 995 | 851 | 1,965 | 3,991 | 4,827 |

| Operating expenses | -105 | -110 | -140 | -168 | -205 | -229 | -223 | -223 | -367 | -523 | -880 | -958 |

| Operating profit | 255 | 289 | 394 | 503 | 692 | 840 | 806 | 772 | 484 | 1,442 | 3,111 | 3,869 |

| Non-operating profit | 39 | 0 | 1 | 2 | 1 | 1 | 1 | 1 | 48 | 42 | 4 | 4 |

| Pre-tax profit | 294 | 289 | 395 | 505 | 693 | 841 | 807 | 773 | 532 | 1,484 | 3,115 | 3,872 |

| Income taxes | -59 | -58 | -79 | -101 | -139 | -168 | -161 | -155 | -162 | -297 | -623 | -774 |

| Net profit | 235 | 232 | 316 | 404 | 555 | 673 | 646 | 619 | 370 | 1,187 | 2,492 | 3,098 |

| Net EPS (TWD) | 3.38 | 3.32 | 4.54 | 5.80 | 7.96 | 9.66 | 9.27 | 8.88 | 5.31 | 17.04 | 35.78 | 44.48 |

| Operating Ratios | ||||||||||||

| Gross margin | 41.6% | 43.5% | 45.9% | 48.7% | 52.5% | 55.1% | 54.0% | 53.5% | 35.0% | 45.4% | 53.8% | 58.9% |

| Operating margin | 29.5% | 31.5% | 33.9% | 36.5% | 40.5% | 43.3% | 42.3% | 41.5% | 19.9% | 33.3% | 41.9% | 47.2% |

| Pre-tax margin | 34.0% | 31.5% | 34.0% | 36.6% | 40.5% | 43.3% | 42.4% | 41.6% | 21.9% | 34.3% | 42.0% | 47.3% |

| Net margin | 27.1% | 25.2% | 27.2% | 29.3% | 32.4% | 34.6% | 33.9% | 33.3% | 15.2% | 27.4% | 33.6% | 37.8% |

| YoY (%) | ||||||||||||

| Net revenue | 74% | 53% | 87% | 94% | 97% | 112% | 64% | 35% | 26% | 78% | 71% | 10% |

| Gross profit | 139% | 104% | 135% | 142% | 149% | 168% | 93% | 48% | 69% | 131% | 103% | 21% |

| Operating profit | 255% | 197% | 192% | 180% | 171% | 191% | 104% | 53% | 138% | 198% | 116% | 24% |

| Pre-tax profit | 259% | 526% | 142% | 110% | 135% | 191% | 104% | 53% | 121% | 179% | 110% | 24% |

| Net profit | 260% | 2663% | 143% | 143% | 136% | 191% | 104% | 53% | 92% | 221% | 110% | 24% |

| QoQ (%) | ||||||||||||

| Net revenue | 22% | 6% | 27% | 19% | 24% | 14% | -2% | -2% | ||||

| Gross profit | 30% | 11% | 34% | 26% | 34% | 19% | -4% | -3% | ||||

| Operating profit | 42% | 13% | 36% | 28% | 38% | 21% | -4% | -4% | ||||

| Pre-tax profit | 23% | -2% | 37% | 28% | 37% | 21% | -4% | -4% | ||||

| Net profit | 42% | -2% | 37% | 28% | 37% | 21% | -4% | -4% |

Source: Company, Daiwa forecasts

Nan Juen: 1Q26 comparison table

| (TWDm) | Actual | QoQ% | YoY% | Daiwa | Diff% | Consensus | Diff% |

|---|---|---|---|---|---|---|---|

| Revenue | 867 | 22% | 74% | 870 | 0% | 850 | 2% |

| Gross profit | 360 | 30% | 139% | 376 | -4% | 366 | -1% |

| Gross margin (%) | 41.6% | 43.3% | 43.0% | ||||

| Operating profit | 255 | 42% | 255% | 270 | -6% | 250 | 2% |

| Operating margin (%) | 29.5% | 31.1% | 29.4% | ||||

| Pre-tax profit | 294 | 23% | 259% | 270 | 9% | 270 | 9% |

| Net profit | 235 | 42% | 260% | 216 | 9% | 208 | 13% |

| EPS (TWD) | 3.38 | 42% | 260% | 3.11 | 9% | 2.99 | 13% |

Source: Company data, Daiwa forecasts, Bloomberg

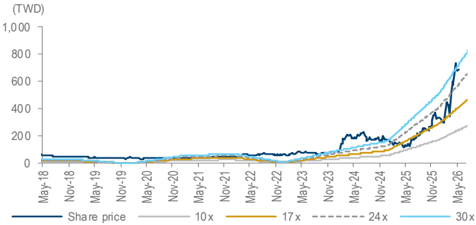

Nan Juen: 1-year forward PER bands

Source: TEJ, Daiwa forecasts

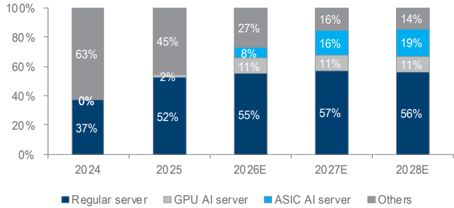

Nan Juen: revenue breakdown

Source: Company, Daiwa forecasts

Daiwa

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Server rail kit revenue | 0 | 479.7 | 357.6 | 712.1 | 1,327.1 | 3,159.2 | 6,249.7 | 7,022.2 |

| Regular server rail kit revenue | 0 | 479.7 | 357.6 | 712.1 | 1,270.6 | 2,369.3 | 4,244.6 | 4,609.2 |

| AI server rail kit revenue | 0 | 0 | 0 | 0 | 56.6 | 789.8 | 2,005.1 | 2,413.0 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Regular server railkit sales | 0 | 480 | 358 | 712 | 1,271 | 2,369 | 4,245 | 4,609 |

| AI server railkit sales | 0 | 0 | 0 | 0 | 57 | 790 | 2,005 | 2,413 |

| Other Revenue | 2,041 | 1,519 | 967 | 1,212 | 1,106 | 1,168 | 1,168 | 1,168 |

| Total Revenue | 2,041 | 1,999 | 1,324 | 1,924 | 2,433 | 4,327 | 7,417 | 8,190 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (1,669) | (1,636) | (1,085) | (1,422) | (1,582) | (2,362) | (3,426) | (3,363) |

| SG&A | (208) | (230) | (191) | (237) | (301) | (437) | (732) | (795) |

| Other op.expenses | (31) | (48) | (38) | (62) | (66) | (85) | (148) | (164) |

| Operating profit | 133 | 85 | 9 | 203 | 484 | 1,442 | 3,111 | 3,869 |

| Net-interest inc./(exp.) | (22) | (22) | (17) | (17) | (12) | (10) | (9) | (9) |

| Assoc/forex/extraord./others | (6) | 110 | 12 | 54 | 60 | 52 | 13 | 12 |

| Pre-tax profit | 105 | 172 | 5 | 240 | 532 | 1,485 | 3,115 | 3,873 |

| Tax | (18) | (42) | 4 | (48) | (162) | (297) | (623) | (774) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 87 | 131 | 8 | 192 | 370 | 1,187 | 2,492 | 3,098 |

| Net profit (adjusted) | 87 | 131 | 8 | 192 | 370 | 1,187 | 2,492 | 3,098 |

| EPS (reported)(TWD) | 1.653 | 2.234 | 0.127 | 2.914 | 5.311 | 17.045 | 35.779 | 44.477 |

| EPS (adjusted)(TWD) | 1.653 | 2.234 | 0.127 | 2.914 | 5.311 | 17.045 | 35.779 | 44.477 |

| EPS (adjusted fully-diluted)(TWD) | 1.653 | 2.234 | 0.127 | 2.914 | 5.311 | 17.045 | 35.779 | 44.477 |

| DPS (TWD) | 0.000 | 1.000 | 1.200 | 1.005 | 1.500 | 2.650 | 9.000 | 17.000 |

| EBIT | 133 | 85 | 9 | 203 | 484 | 1,442 | 3,111 | 3,869 |

| EBITDA | 267 | 218 | 125 | 322 | 628 | 1,695 | 3,390 | 4,186 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 105 | 172 | 5 | 240 | 532 | 1,485 | 3,115 | 3,873 |

| Depreciation and amortisation | 134 | 133 | 116 | 119 | 143 | 253 | 279 | 317 |

| Tax paid | (18) | (42) | 4 | (48) | (162) | (297) | (623) | (774) |

| Change in working capital | (238) | 64 | (10) | (133) | (251) | 257 | (346) | (71) |

| Other operational CF items | 57 | 43 | (34) | 117 | 78 | 0 | 0 | 0 |

| Cash flow from operations | 40 | 370 | 80 | 295 | 341 | 1,697 | 2,425 | 3,345 |

| Capex | (68) | (70) | (29) | (113) | (122) | (325) | (482) | (246) |

| Net (acquisitions)/disposals | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other investing CF items | (7) | (4) | (3) | (21) | (9) | 0 | 0 | 0 |

| Cash flow from investing | (76) | (74) | (32) | (134) | (131) | (325) | (482) | (246) |

| Change in debt | 226 | (383) | (328) | 111 | 84 | 0 | 0 | 0 |

| Net share issues/(repurchases) | 45 | 171 | 413 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | 0 | (52) | (70) | (66) | (99) | (185) | (627) | (1,184) |

| Other financing CF items | (23) | (24) | (21) | (285) | (47) | 0 | 0 | 0 |

| Cash flow from financing | 248 | (289) | (7) | (240) | (62) | (185) | (627) | (1,184) |

| Forex effect/others | (0) | 1 | 0 | (3) | (2) | 0 | 0 | 0 |

| Change in cash | 212 | 9 | 42 | (82) | 145 | 1,188 | 1,316 | 1,915 |

| Free cash flow | (29) | 300 | 52 | 181 | 219 | 1,372 | 1,943 | 3,099 |

Source: FactSet, Daiwa forecasts

Nan Juen International (6584 TT): 11 May 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 363 | 384 | 414 | 327 | 496 | 1,684 | 3,000 | 4,914 |

| Inventory | 330 | 288 | 262 | 298 | 487 | 518 | 751 | 737 |

| Accounts receivable | 432 | 280 | 297 | 436 | 536 | 415 | 711 | 785 |

| Other current assets | 40 | 13 | 12 | 23 | 57 | 57 | 57 | 57 |

| Total current assets | 1,164 | 965 | 984 | 1,084 | 1,577 | 2,674 | 4,519 | 6,494 |

| Fixed assets | 2,530 | 2,492 | 2,430 | 2,454 | 2,464 | 2,536 | 2,739 | 2,668 |

| Goodwill & intangibles | 7 | 7 | 7 | 9 | 11 | 11 | 11 | 11 |

| Other non-current assets | 58 | 50 | 78 | 394 | 334 | 334 | 334 | 334 |

| Total assets | 3,759 | 3,513 | 3,499 | 3,941 | 4,386 | 5,555 | 7,604 | 9,507 |

| Short-term debt | 428 | 253 | 419 | 117 | 0 | 0 | 0 | 0 |

| Accounts payable | 305 | 185 | 161 | 204 | 242 | 408 | 591 | 580 |

| Other current liabilities | 319 | 335 | 259 | 301 | 411 | 411 | 411 | 411 |

| Total current liabilities | 1,052 | 773 | 839 | 622 | 653 | 819 | 1,003 | 992 |

| Long-term debt | 1,388 | 1,166 | 696 | 1,027 | 552 | 552 | 552 | 552 |

| Other non-current liabilities | 11 | 4 | 39 | 61 | 37 | 37 | 37 | 37 |

| Total liabilities | 2,451 | 1,942 | 1,573 | 1,710 | 1,243 | 1,408 | 1,592 | 1,581 |

| Share capital | 525 | 585 | 656 | 660 | 697 | 697 | 697 | 697 |

| Reserves/R.E./others | 784 | 986 | 1,269 | 1,571 | 2,447 | 3,450 | 5,315 | 7,229 |

| Shareholders’ equity | 1,309 | 1,571 | 1,925 | 2,231 | 3,144 | 4,146 | 6,012 | 7,926 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 3,759 | 3,513 | 3,499 | 3,941 | 4,386 | 5,555 | 7,604 | 9,507 |

| EV | 49,312 | 48,895 | 48,560 | 48,676 | 47,916 | 46,728 | 45,412 | 43,498 |

| Net debt/(cash) | 1,453 | 1,035 | 700 | 817 | 56 | (1,131) | (2,447) | (4,362) |

| BVPS (TWD) | 24.931 | 26.864 | 29.333 | 33.826 | 45.126 | 59.518 | 86.294 | 113.769 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 40.2 | (2.1) | (33.7) | 45.3 | 26.4 | 77.8 | 71.4 | 10.4 |

| EBITDA (YoY) | 137.5 | (18.6) | (42.5) | 157.3 | 94.8 | 170.0 | 100.0 | 23.5 |

| Operating profit (YoY) | 3,825.2 | (36.2) | (88.8) | 2,042.9 | 138.1 | 197.7 | 115.7 | 24.4 |

| Net profit (YoY) | n.a. | 50.6 | (93.6) | 2,208.0 | 92.5 | 220.9 | 109.9 | 24.3 |

| Core EPS (fully-diluted) (YoY) | n.a. | 35.1 | (94.3) | 2,197.0 | 82.2 | 220.9 | 109.9 | 24.3 |

| Gross-profit margin | 18.2 | 18.1 | 18.0 | 26.1 | 35 | 45.4 | 53.8 | 58.9 |

| EBITDA margin | 13.1 | 10.9 | 9.5 | 16.8 | 25.8 | 39.2 | 45.7 | 51.1 |

| Operating-profit margin | 6.5 | 4.2 | 0.7 | 10.6 | 19.9 | 33.3 | 41.9 | 47.2 |

| Net profit margin | 4.3 | 6.5 | 0.6 | 10.0 | 15.2 | 27.4 | 33.6 | 37.8 |

| ROAE | 7.0 | 9.1 | 0.5 | 9.2 | 13.8 | 32.6 | 49.1 | 44.5 |

| ROAA | 2.5 | 3.6 | 0.2 | 5.2 | 8.9 | 23.9 | 37.9 | 36.2 |

| ROCE | 4.5 | 2.8 | 0.3 | 6.3 | 13.7 | 34.4 | 55.2 | 51.4 |

| ROIC | 4.1 | 2.4 | 0.4 | 5.7 | 10.8 | 37.1 | 75.7 | 86.9 |

| Net debt to equity | 111.0 | 65.9 | 36.4 | 36.6 | 1.8 | n.a. | n.a. | n.a. |

| Effective tax rate | 17.0 | 24.2 | 0.0 | 20.0 | 30.4 | 20.0 | 20.0 | 20.0 |

| Accounts receivable (days) | 61.4 | 65.1 | 79.5 | 69.5 | 72.9 | 40.1 | 27.7 | 33.3 |

| Current ratio (x) | 1.1 | 1.2 | 1.2 | 1.7 | 2.4 | 3.3 | 4.5 | 6.5 |

| Net interest cover (x) | 6.0 | 3.8 | 0.6 | 12.1 | 38.9 | 150.2 | 353.9 | 449.3 |

| Net dividend payout | n.a. | 60.5 | 53.7 | 792.1 | 51.5 | 49.9 | 52.8 | 47.5 |

| Free cash flow yield | n.a. | 0.6 | 0.1 | 0.4 | 0.5 | 2.9 | 4.1 | 6.5 |

Source: FactSet, Daiwa forecasts

Company profile

Founded in 1984, Nan Juen International Co., LTD. is a Taiwan-based slide and rail kit manufacturer headquartered in Taoyuan City. The company began its operations as a producer of furniture and kitchen rail kits, leveraging its mechanical engineering expertise to gradually expand its product portfolio. Building on decades of slide mechanism design experience, Nan Juen extended its capabilities into the server rail kit market, which has since become the primary growth driver of the business.

Nan Juen’s current product portfolio spans two core categories: server rail kits and others (including kitchen rail kits, office furniture rail kits, etc.). Within the server rail kit segment, the company produces both regular server rail kits and AI server rail kits, serving major CSPs globally. The company has been listed on the Taiwan Stock Exchange under the ticker 6584 TT.

Nan Juen International (6584 TT): 11 May 2026

Daiwa

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| G | Executive/board quality | 2 | Nan Juen’s board consists of 9 directors, including 4 independent directors. The total number of directors is slightly lower than that of other listed companies in our coverage. Nan Juen held 6 board meetings in 2024; the actual attendee rate was 98%. Most of the board members are Nan Juen’s founder’s family members, which we believe presents downside risks to independent governance. However, the independent directors have diversified backgrounds with expertise in accounting and management, a positive for the board’s quality. |

| Capital management | 2 | Nan Juen declared a DPS of TWD1.5 in 2024, representing a payout ratio of 51%. The payout ratio was in line with the level of 50-60% during 2021-24. As a rail kit manufacturer, Nan Juen is set to deliver solid revenue growth and FCF over our forecast horizon amidst strong ASP increase in the server rail kit market. | |

| Related party & transaction | 1 | The company did not report any related-party transactions in 2025. We see limited risks from related-party transactions. | |

| S | Product quality & safety | 2 | Nan Juen has implemented a Project Management Information System (PMIS) to streamline R&D workflows and enhance cross-departmental collaboration. The company is further planning to introduce a Product Lifecycle Management (PLM) system, integrating the full product lifecycle from concept through to manufacturing and after-sales service. Beyond operational efficiency, the PLM adoption reflects Nan Juen’s commitment to responsible product stewardship, enabling better oversight of material consumption and environmental impact across its operations. The company continues to advance its green product programme. Based on 2024 shipments, its carbon emissions were 4,490 tonnes of CO2e (vs. 3,794 tonnes in 2023), but with a lower CO2e per TWD1m revenue of 2.33 tonnes (vs. 2.87 tonnes in 2024), underscoring progress in lowering the environmental footprint of its products. |

| S | Product design & lifecycle management | 2 | Nan Juen is actively reducing its greenhouse gas emissions under a core commitment to net- zero carbon operations, aligned with Taiwan’s 2050 net-zero emission policy. The company has adopted ISO 14064-1 GHG inventory standards and maintains ISO 14001:2015 environmental management system certification, providing a structured framework for monitoring and improving energy use and emissions across its operations. Practical measures include regular audits of high-energy-consuming equipment, employee sustainability training, and collaboration with supply chain partners on green procurement. Progress is tracked through internal audits and external verification, with findings reviewed periodically to refine the company’s decarbonisation strategy. |

| Supply chain management |

Note: Management score represents a company’s ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 17 Apr 2026

Source: Daiwa, Company

Nan Juen International (6584 TT): 11 May 2026

Daiwa