報告_Daiwa_儒鴻1476_20260519

PDF 原檔:報告_Daiwa_儒鴻1476_20260519_original.pdf

原始內容

Taiwan

Eclat Textile (1476 TT)

Target price:

TWD560.00 (from TWD540.00)

Share price (19 May):

TWD320.00

|

Up/downside:

+75.0%

1Q26 results review: solid 2026 outlook

- 1Q26 results: a strong beat on gross and operating margins

- Order outlook remains on track for 2026

- Reaffirming our Buy (1) rating; raising 12-month TP to TWD560

What’s new: Eclat held an investor conference on 19 May to discuss its 1Q26 results (see our Memo , 7 May) and its outlook for 2026. We reaffirm our Buy (1) rating, as we believe Eclat is in a solid position to gain market share through vendor consolidation and to benefit from a trend towards functionality upgrades designed to navigate macroeconomic uncertainties, such as inflation and oil price hikes.

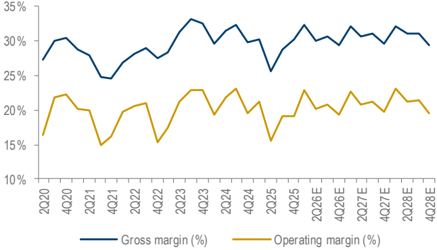

What’s the impact: Key highlights of 1Q26 results: a strong beat. Its 1Q26 gross margin came in at 32.2% (vs. 30.2% in both 4Q25 and 1Q25), beating our estimate (28.5%) and the consensus (29.7%), thanks to new product lines and gross margin improvements in both its garment and fabric segments. The company maintains its gross margin target of 28-32%, and will update in mid-2026. Its revenue momentum for 4M26 was mainly driven by the garment segment.

Unchanged 2026 order outlook and gross margin guidance. Its order visibility remains at 6 months, and the company aims to deliver monthly revenue of TWD3bn+ for the remaining months of 2026. Despite the inflationary environment in the US, the company believes order placement momentum remains intact. YTD, revenue contribution from new clients was 10.3%, and revenue contribution from new products was 15-20%. The order outlook from its key clients is largely on track, with some rush orders in between, despite macro uncertainty. Its new plant in Indonesia will be established in 2H26 and ramp up capacity in 2H27, with garment capacity added first and fabric capacity considered thereafter. Its mid- to long-term revenue drivers are new product development (including functionality upgrades and high value-added products) on top of its innovation capability. During the meeting, management highlighted that it will gradually raise its cash dividend payout ratio onward, vs. 75% in 2025. We slightly raise our 2026E EPS by 4%, mainly on our more aggressive gross margin assumptions, but trim our 2027E EPS by 2% on more conservative revenue forecasts. We also introduce our 2028 forecasts.

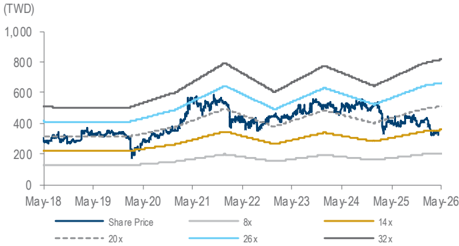

What we recommend: We reaffirm our Buy (1) rating and raise our 12month TP to TWD560 (from TWD540), still based on a target PER of 22x (close to the mid-point of its past-5-year range of 13-27x [average PER of 21x]), and on 1-year forward EPS. Key downside risks: slower-thanexpected gross margin expansion; lower-than-expected demand; and high inflation and tariff uncertainty.

How we differ: Our 2026E EPS is 2% above consensus, likely as we are slightly more aggressive on Eclat’s gross margin assumptions.

19 May 2026

Daiwa

5

3

→

2

1

Buy

Helen Chien

Helen Chien

(886) 2 8758 6254

helen.chien@daiwacm-cathay.com.tw

Neil Teng (886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | (3.2) | (3.2) | n.a. |

| Net profit change | 4.0 | (1.4) | n.a. |

| Core EPS (FD) change | 3.8 | (1.5) | n.a. |

Source: Daiwa forecasts

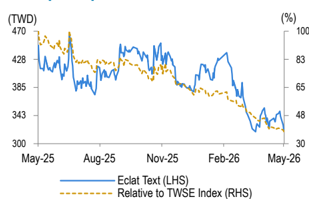

Share price performance

| 12-month range | 318.00-466.00 |

|---|---|

| Market cap (USDbn) | 2.78 |

| 3m avg daily turnover (USDm) | 17.11 |

| Shares outstanding (m) | 274 |

| Major shareholder | Zhen-Hai Hong (Chairman) (3.3%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 40,561 | 43,894 | 47,534 |

| Operating profit (m) | 8,396 | 9,218 | 10,077 |

| Net profit (m) | 6,797 | 7,396 | 8,077 |

| Core EPS (fully-diluted) | 24.729 | 26.908 | 29.385 |

| EPS change (%) | 23.1 | 8.8 | 9.2 |

| Daiwa vs Cons. EPS (%) | 1.7 | (0.0) | (0.6) |

| PER (x) | 12.9 | 11.9 | 10.9 |

| Dividend yield (%) | 5.8 | 6.3 | 6.9 |

| DPS | 18.6 | 20.2 | 22.1 |

| PBR (x) | 2.7 | 2.5 | 2.4 |

| EV/EBITDA (x) | 9.2 | 8.3 | 7.5 |

| ROE (%) | 21.9 | 22.1 | 22.5 |

Source: FactSet, Daiwa forecasts

Eclat: revenue and earnings forecasts revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | New | Previous | Change | New | Previous | Change | New | Previous | Change |

| Fabric revenue | 13,286 | 13,286 | 0.0% | 13,823 | 13,823 | 0.0% | 14,381 | n.a. | n.a. |

| Garment revenue | 27,275 | 28,599 | -4.6% | 30,071 | 31,531 | -4.6% | 33,153 | n.a. | n.a. |

| Sales | 40,561 | 41,885 | -3.2% | 43,894 | 45,353 | -3.2% | 47,534 | n.a. | n.a. |

| Gross profit | 12,371 | 12,147 | 1.8% | 13,475 | 13,606 | -1.0% | 14,641 | n.a. | n.a. |

| Gross profit margin | 30.5% | 29.0% | 1.5pp | 30.7% | 30.0% | 0.7pp | 30.8% | n.a. | n.a. |

| Operating profit | 8,396 | 8,084 | 3.9% | 9,218 | 9,297 | -0.9% | 10,077 | n.a. | n.a. |

| Operating profit margin | 20.7% | 19.3% | 1.4pp | 21.0% | 20.5% | 0.5pp | 21.2% | n.a. | n.a. |

| Net profit | 6,797 | 6,537 | 4.0% | 7,396 | 7,502 | -1.4% | 8,077 | n.a. | n.a. |

| Net profit margin | 16.8% | 15.6% | 1.2pp | 16.9% | 16.5% | 0.3pp | 17.0% | n.a. | n.a. |

| EPS (TWD) | 24.73 | 23.81 | 3.8% | 26.91 | 27.33 | -1.5% | 29.38 | n.a. | n.a. |

Source: Daiwa forecasts

Eclat: 1Q26 results vs. Daiwa and Bloomberg forecasts

| (TWDm) | Eclat’s 1Q26 results | Daiwa’s previous forecast | Difference | Bloomberg consensus | Difference |

|---|---|---|---|---|---|

| Revenue | 9,621 | 9,122 | 5.5% | 9,460 | 1.7% |

| Gross profit | 3,095 | 2,600 | 19.0% | 2,814 | 10.0% |

| Operating profit | 2,195 | 1,665 | 31.9% | 1,911 | 14.9% |

| Profit before tax | 2,291 | 1,699 | 34.8% | 1,948 | 17.6% |

| Net profit | 1,835 | 1,367 | 34.2% | 1,550 | 18.3% |

| Basic EPS (TWD) | 6.69 | 4.98 | 34.2% | 5.62 | 19.0% |

| Margin | |||||

| Gross margin | 32.2% | 28.5% | 3.7pp | 29.7% | 2.4pp |

| Operating margin | 22.8% | 18.2% | 4.6pp | 20.2% | 2.6pp |

| Pre-tax margin | 23.8% | 18.6% | 5.2pp | 20.6% | 3.2pp |

| Net margin | 19.1% | 15.0% | 4.1pp | 16.4% | 2.7pp |

Source: Company, Bloomberg, Daiwa forecasts

Eclat: quarterly P&L

| 2026E | 2026E | 2026E | 2026E | 2027E | 2026E | 2027E | 2028E | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | |||

| Revenue | 9,621 | 10,264 | 10,500 | 10,176 | 10,300 | 10,900 | 11,100 | 11,594 | 40,561 | 43,894 | 47,534 |

| Gross profit | 3,095 | 3,079 | 3,203 | 2,995 | 3,296 | 3,325 | 3,441 | 3,414 | 12,371 | 13,475 | 14,641 |

| Operating profit | 2,195 | 2,069 | 2,173 | 1,960 | 2,326 | 2,260 | 2,351 | 2,281 | 8,396 | 9,218 | 10,077 |

| Pre-tax profit | 2,291 | 2,100 | 2,203 | 1,991 | 2,357 | 2,290 | 2,382 | 2,312 | 8,585 | 9,342 | 10,201 |

| Net profit | 1,835 | 1,522 | 1,743 | 1,697 | 1,888 | 1,660 | 1,884 | 1,964 | 6,797 | 7,396 | 8,077 |

| Basic EPS (TWD) | 6.69 | 5.55 | 6.35 | 6.19 | 6.88 | 6.05 | 6.87 | 7.16 | 24.77 | 26.96 | 29.44 |

| Margin | |||||||||||

| Gross margin | 32.2% | 30.0% | 30.5% | 29.4% | 32.0% | 30.5% | 31.0% | 29.4% | 30.5% | 30.7% | 30.8% |

| Operating margin | 22.8% | 20.2% | 20.7% | 19.3% | 22.6% | 20.7% | 21.2% | 19.7% | 20.7% | 21.0% | 21.2% |

| Pre-tax margin | 23.8% | 20.5% | 21.0% | 19.6% | 22.9% | 21.0% | 21.5% | 19.9% | 21.2% | 21.3% | 21.5% |

| Net margin | 19.1% | 14.8% | 16.6% | 16.7% | 18.3% | 15.2% | 17.0% | 16.9% | 16.8% | 16.9% | 17.0% |

| YoY | |||||||||||

| Revenue | 2.6% | 5.6% | 9.0% | 9.8% | 7.1% | 6.2% | 5.7% | 13.9% | 6.8% | 8.2% | 8.3% |

| Gross profit | 9.3% | 23.5% | 16.0% | 7.1% | 6.5% | 8.0% | 7.4% | 14.0% | 13.7% | 8.9% | 8.6% |

| Operating profit | 11.1% | 37.9% | 18.0% | 10.4% | 6.0% | 9.2% | 8.2% | 16.4% | 18.4% | 9.8% | 9.3% |

| Pre-tax profit | 9.8% | 153.2% | 5.5% | 1.5% | 2.9% | 9.1% | 8.1% | 16.2% | 23.2% | 8.8% | 9.2% |

| Net profit | 9.2% | 153.2% | 5.5% | 7.3% | 2.9% | 9.1% | 8.1% | 15.7% | 23.2% | 8.8% | 9.2% |

| QoQ | |||||||||||

| Revenue | 3.9% | 6.7% | 2.3% | -3.1% | 1.2% | 5.8% | 1.8% | 4.4% | |||

| Gross profit | 10.7% | -0.5% | 4.0% | -6.5% | 10.1% | 0.9% | 3.5% | -0.8% | |||

| Operating profit | 23.6% | -5.7% | 5.0% | -9.8% | 18.7% | -2.9% | 4.0% | -3.0% | |||

| Pre-tax profit | 16.9% | -8.3% | 4.9% | -9.7% | 18.4% | -2.8% | 4.0% | -2.9% | |||

| Net profit | 16.0% | -17.0% | 14.5% | -2.6% | 11.2% | -12.1% | 13.5% | 4.2% |

Source: Company, Daiwa forecasts

Eclat: margin trend

Source: Company, Daiwa forecasts

Eclat: 1-year forward PER

Source: Bloomberg, Daiwa forecasts

Eclat Textile (1476 TT): 19 May 2026

Daiwa

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Garment revenue growth (YoY %) | 16.9 | 5.2 | (22.6) | 23.9 | 6.2 | 8.2 | 10.3 | 10.3 |

| Fabric revenue growth (YoY %) | 52.9 | 21.8 | (22.4) | 12.5 | (2.3) | 4 | 4 | 4 |

| Gross margin (%) | 26.4 | 27.8 | 31.4 | 30.9 | 28.6 | 30.5 | 30.7 | 30.8 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Garment revenue | 23,552 | 24,774 | 19,174 | 23,755 | 25,220 | 27,275 | 30,071 | 33,153 |

| Fabric revenue | 12,284 | 14,962 | 11,617 | 13,073 | 12,770 | 13,286 | 13,823 | 14,381 |

| Other Revenue | 81 | 0 | 0 | 0 | 0 | 0 | (0) | 0 |

| Total Revenue | 35,917 | 39,736 | 30,790 | 36,828 | 37,990 | 40,561 | 43,894 | 47,534 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (26,426) | (28,671) | (21,111) | (25,460) | (27,108) | (28,190) | (30,418) | (32,894) |

| SG&A | (2,930) | (3,168) | (2,977) | (3,442) | (3,614) | (3,772) | (4,038) | (4,326) |

| Other op.expenses | (163) | (160) | (153) | (171) | (176) | (203) | (219) | (238) |

| Operating profit | 6,398 | 7,737 | 6,549 | 7,755 | 7,092 | 8,396 | 9,218 | 10,077 |

| Net-interest inc./(exp.) | (2) | (23) | (2) | 38 | 99 | 84 | 84 | 84 |

| Assoc/forex/extraord./others | (11) | 826 | 128 | 557 | (225) | 105 | 40 | 40 |

| Pre-tax profit | 6,386 | 8,540 | 6,676 | 8,351 | 6,966 | 8,585 | 9,342 | 10,201 |

| Tax | (1,237) | (1,750) | (1,499) | (1,710) | (1,451) | (1,788) | (1,945) | (2,124) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 5,149 | 6,790 | 5,176 | 6,641 | 5,515 | 6,797 | 7,396 | 8,077 |

| Net profit (adjusted) | 5,149 | 6,790 | 5,176 | 6,641 | 5,515 | 6,797 | 7,396 | 8,077 |

| EPS (reported)(TWD) | 18.765 | 24.749 | 18.867 | 24.204 | 20.101 | 24.774 | 26.957 | 29.438 |

| EPS (adjusted)(TWD) | 18.765 | 24.749 | 18.867 | 24.204 | 20.101 | 24.774 | 26.957 | 29.438 |

| EPS (adjusted fully-diluted)(TWD) | 18.764 | 24.747 | 18.866 | 24.203 | 20.087 | 24.729 | 26.908 | 29.385 |

| DPS (TWD) | 12.000 | 17.000 | 13.500 | 17.000 | 15.000 | 18.580 | 20.218 | 22.078 |

| EBIT | 6,398 | 7,737 | 6,549 | 7,755 | 7,092 | 8,396 | 9,218 | 10,077 |

| EBITDA | 7,031 | 8,531 | 7,430 | 8,642 | 7,968 | 9,255 | 10,158 | 11,090 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 6,386 | 8,540 | 6,676 | 8,351 | 6,966 | 8,585 | 9,342 | 10,201 |

| Depreciation and amortisation | 632 | 794 | 881 | 886 | 876 | 859 | 940 | 1,012 |

| Tax paid | (1,237) | (1,750) | (1,499) | (1,710) | (1,451) | (1,788) | (1,945) | (2,124) |

| Change in working capital | (3,020) | 3,828 | (708) | (2,365) | 1,283 | (1,260) | (226) | (957) |

| Other operational CF items | 16 | 905 | (686) | (442) | (104) | 0 | 0 | 0 |

| Cash flow from operations | 2,778 | 12,318 | 4,664 | 4,720 | 7,570 | 6,396 | 8,110 | 8,132 |

| Capex | (2,490) | (1,796) | (303) | (484) | (370) | (2,480) | (2,000) | (2,000) |

| Net (acquisitions)/disposals | 5 | 0 | 46 | 93 | 0 | 0 | 0 | 0 |

| Other investing CF items | (13) | (3,011) | (1,579) | (401) | (1,497) | 0 | 0 | 0 |

| Cash flow from investing | (2,498) | (4,807) | (1,836) | (792) | (1,866) | (2,480) | (2,000) | (2,000) |

| Change in debt | 4 | 431 | (1,154) | 1,181 | (1,171) | 0 | 0 | 0 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (3,018) | (3,292) | (4,664) | (3,704) | (4,664) | (4,116) | (5,098) | (5,547) |

| Other financing CF items | 525 | (393) | (233) | (586) | (18) | 0 | 0 | 0 |

| Cash flow from financing | (2,489) | (3,254) | (6,052) | (3,109) | (5,854) | (4,116) | (5,098) | (5,547) |

| Forex effect/others | (54) | 5 | 15 | (15) | (59) | 0 | 0 | 0 |

| Change in cash | (2,264) | 4,262 | (3,209) | 804 | (209) | (200) | 1,012 | 585 |

| Free cash flow | 287 | 10,522 | 4,361 | 4,236 | 7,200 | 3,916 | 6,110 | 6,132 |

Source: FactSet, Daiwa forecasts

Eclat Textile (1476 TT): 19 May 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 1,760 | 6,022 | 2,814 | 3,618 | 3,409 | 3,210 | 4,222 | 4,807 |

| Inventory | 8,276 | 4,625 | 4,402 | 5,522 | 5,931 | 6,141 | 6,641 | 7,174 |

| Accounts receivable | 5,209 | 4,087 | 4,967 | 6,638 | 4,817 | 6,227 | 6,152 | 6,980 |

| Other current assets | 578 | 3,621 | 5,215 | 5,730 | 7,210 | 7,210 | 7,210 | 7,210 |

| Total current assets | 15,823 | 18,355 | 17,398 | 21,508 | 21,367 | 22,787 | 24,225 | 26,170 |

| Fixed assets | 12,065 | 13,627 | 12,288 | 12,994 | 12,328 | 13,944 | 15,004 | 15,992 |

| Goodwill & intangibles | 19 | 19 | 25 | 27 | 20 | 20 | 20 | 20 |

| Other non-current assets | 1,372 | 1,362 | 2,122 | 1,337 | 1,326 | 1,326 | 1,326 | 1,326 |

| Total assets | 29,279 | 33,364 | 31,833 | 35,865 | 35,042 | 38,078 | 40,575 | 43,508 |

| Short-term debt | 1,347 | 1,778 | 624 | 1,804 | 547 | 547 | 547 | 547 |

| Accounts payable | 4,144 | 3,526 | 3,137 | 3,793 | 3,625 | 3,985 | 4,184 | 4,587 |

| Other current liabilities | 1,536 | 2,274 | 2,320 | 1,169 | 1,090 | 1,090 | 1,090 | 1,090 |

| Total current liabilities | 7,027 | 7,577 | 6,081 | 6,767 | 5,263 | 5,623 | 5,822 | 6,225 |

| Long-term debt | 1,037 | 563 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current liabilities | 66 | 81 | 81 | 177 | 137 | 137 | 137 | 137 |

| Total liabilities | 8,129 | 8,222 | 6,162 | 6,943 | 5,400 | 5,760 | 5,958 | 6,362 |

| Share capital | 2,744 | 2,744 | 2,744 | 2,744 | 2,744 | 2,744 | 2,744 | 2,744 |

| Reserves/R.E./others | 18,406 | 22,398 | 22,927 | 26,178 | 26,893 | 29,575 | 31,873 | 34,403 |

| Shareholders’ equity | 21,149 | 25,142 | 25,671 | 28,922 | 29,637 | 32,319 | 34,617 | 37,147 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 29,279 | 33,364 | 31,833 | 35,865 | 35,037 | 38,078 | 40,575 | 43,508 |

| EV | 88,421 | 84,116 | 85,608 | 85,984 | 84,935 | 85,135 | 84,123 | 83,538 |

| Net debt/(cash) | 624 | (3,681) | (2,190) | (1,814) | (2,862) | (2,662) | (3,675) | (4,259) |

| BVPS (TWD) | 77.084 | 91.636 | 93.563 | 105.412 | 108.020 | 117.793 | 126.170 | 135.390 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 27.5 | 10.6 | (22.5) | 19.6 | 3.2 | 6.8 | 8.2 | 8.3 |

| EBITDA (YoY) | 13.4 | 21.3 | (12.9) | 16.3 | (7.8) | 16.2 | 9.8 | 9.2 |

| Operating profit (YoY) | 16.4 | 20.9 | (15.4) | 18.4 | (8.6) | 18.4 | 9.8 | 9.3 |

| Net profit (YoY) | 21.0 | 31.9 | (23.8) | 28.3 | (17.0) | 23.2 | 8.8 | 9.2 |

| Core EPS (fully-diluted) (YoY) | 21.0 | 31.9 | (23.8) | 28.3 | (17.0) | 23.1 | 8.8 | 9.2 |

| Gross-profit margin | 26.4 | 27.8 | 31.4 | 30.9 | 28.6 | 30.5 | 30.7 | 30.8 |

| EBITDA margin | 19.6 | 21.5 | 24.1 | 23.5 | 21.0 | 22.8 | 23.1 | 23.3 |

| Operating-profit margin | 17.8 | 19.5 | 21.3 | 21.1 | 18.7 | 20.7 | 21.0 | 21.2 |

| Net profit margin | 14.3 | 17.1 | 16.8 | 18.0 | 14.5 | 16.8 | 16.9 | 17.0 |

| ROAE | 25.5 | 29.3 | 20.4 | 24.3 | 18.8 | 21.9 | 22.1 | 22.5 |

| ROAA | 18.5 | 21.7 | 15.9 | 19.6 | 15.6 | 18.6 | 18.8 | 19.2 |

| ROCE | 28.7 | 30.3 | 24.4 | 27.2 | 23.3 | 26.6 | 27.1 | 27.7 |

| ROIC | 26.6 | 28.5 | 22.6 | 24.4 | 20.8 | 23.6 | 24.1 | 25.0 |

| Net debt to equity | 2.9 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Effective tax rate | 19.4 | 20.5 | 22.5 | 20.5 | 20.8 | 20.8 | 20.8 | 20.8 |

| Accounts receivable (days) | 53.7 | 42.7 | 53.7 | 57.5 | 55.0 | 49.7 | 51.5 | 50.4 |

| Current ratio (x) | 2.3 | 2.4 | 2.9 | 3.2 | 4.1 | 4.1 | 4.2 | 4.2 |

| Net interest cover (x) | 4,206.8 | 337.2 | 3,882.0 | n.a. | n.a. | n.a. | n.a. | n.a. |

| Net dividend payout | 63.9 | 68.7 | 71.6 | 70.2 | 74.6 | 75.0 | 75.0 | 75.0 |

| Free cash flow yield | 0.3 | 12.0 | 5.0 | 4.8 | 8.2 | 4.5 | 7.0 | 7.0 |

Source: FactSet, Daiwa forecasts

Company profile

Eclat Textile (Eclat) is a technology-based Taiwanese textiles company that supplies functional and flexible knitwear fabrics, as well as sports apparel products, to a diversified client base. Its major clients include Nike, Gap (Athleta), Under Armour and Lululemon.

Eclat Textile (1476 TT): 19 May 2026

Daiwa

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| G | Executive/board quality | 1 | The CEO and Chairman of Eclat are not the same individual. The Chairman leads the board and the 2 independent CEOs manage its fabric and garment divisions, respectively. The board includes 4 independent directors and 1 female member. Moreover, 3 of the board members (including the Chairman) are founding members, with more than 40 years of experience in Eclat’s business, indicating strong leadership and management capability. |

| G | Capital management | 1 | Eclat has maintained its payout ratio at 64-75% over 2019-25. As it is expanding its capacity in Indonesia, we believe the current payout level is reasonable. |

| G | Related party & transaction | 1 | Eclat’s garment division sources partially from its fabric division, with an internal transfer ratio of 40%. We believe this is a strong sign to its clients about the company’s competitive advantages in production cost and quality. |

| S | Supply chain management | 1 | Eclat adheres to the ZDHC regulation (MRSL) and has adopted the Higg Index to evaluate its sustainability. It is also a partner of the Bluesign system. Eclat has also set up its ERP system, which could save 50k+ hours per year. To lower supplier-related risks, it adopts a decentralised procurement strategy that conducts collaborative R&D with suppliers. Its capacity allocation has expanded to different regions in the past few years, including Taiwan, Vietnam, Cambodia and Indonesia. We believe the risk-mitigation measures from the decentralised procurement strategy can offset the costs incurred from managing suppliers from various locations. |

| E | Materials sourcing & efficiency | 1 | As one of the few textile companies that have R&D capability to develop innovative products, Eclat has invested substantially in its environment-friendly products on the back of the ESG trend in the fashion industry. Also, Eclat has been increasing its recycled yarn percentage every year (2022: 17.23%) and is dedicated to improving its local-to-local sourcing ratio (2022: 85.43% in Taiwan; 45.81% in Vietnam), which saves transportation costs and energy, and lowers carbon emissions. |

Note: Management score represents a company’s ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 19 May 2026

Source: Daiwa, Company

Eclat Textile (1476 TT): 19 May 2026

Daiwa